The State of Digitization in B2B Finance

In collaboration with Wakefield Research, Versapay surveyed 1,000 C-level executives at companies with a minimum annual revenue of $100m USD on their AR digital transformation efforts.

The State of Digitization in B2B Finance

WAKEFIELD + VERSAPAY

June 3rd, 2022

In collaboration with Wakefield Research, Versapay surveyed 1,000 C-level executives at companies with a minimum annual revenue of $100m USD on their accounts receivable (AR) digital transformation efforts.

Download the free report and see why Collaborative AR automation software must be included as part of your digital transformation roadmap.

Here's what you can expect:

- Learn why automation alone won't bridge the AR disconnect

- Explore how the current climate is accelerating the need for AR transformation (and why companies still might not be prioritizing it)

- Discover the work businesses still need to do to digitize AR

- See what Collaborative AR is and how it's bridging the human divide

- Uncover the solution to the AR disconnect (hint: it's Versapay's Collaborative AR Network)

- Plus, key insights on how ignoring the customer in AR digitization hurts businesses' bottom lines

Take a peek inside the report

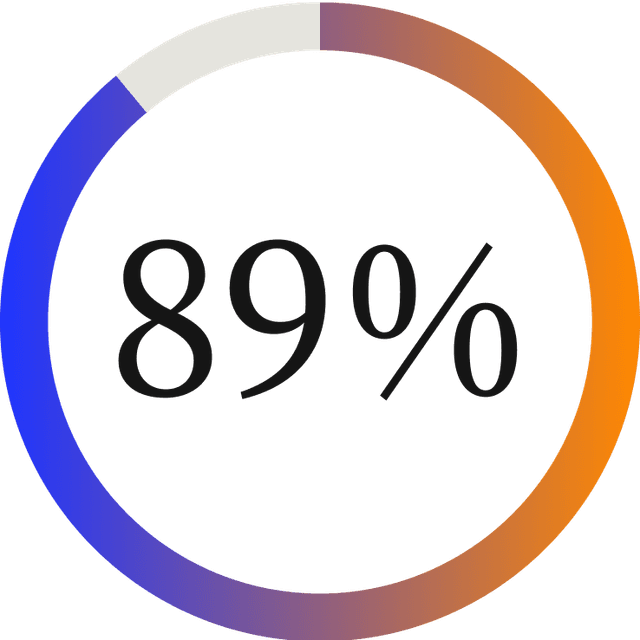

... of executives agree that the customer's experience is a key measurement of the C-suite's effectiveness

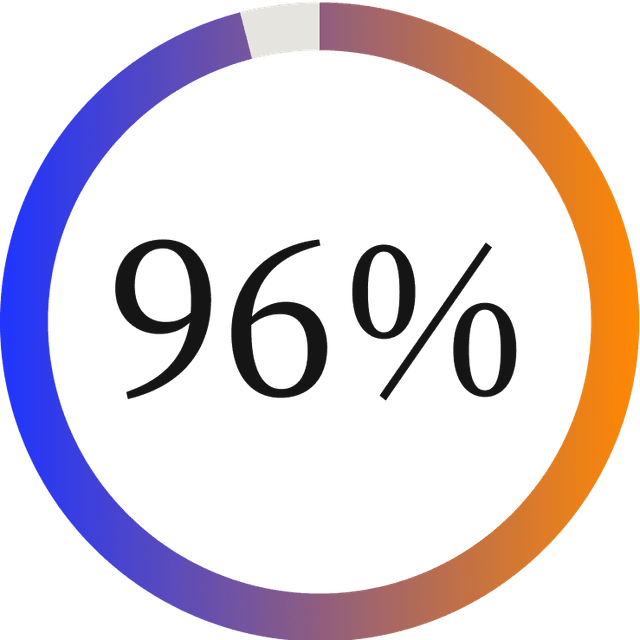

... of executives acknowledge that there's still work to be done to digitize accounts receivable

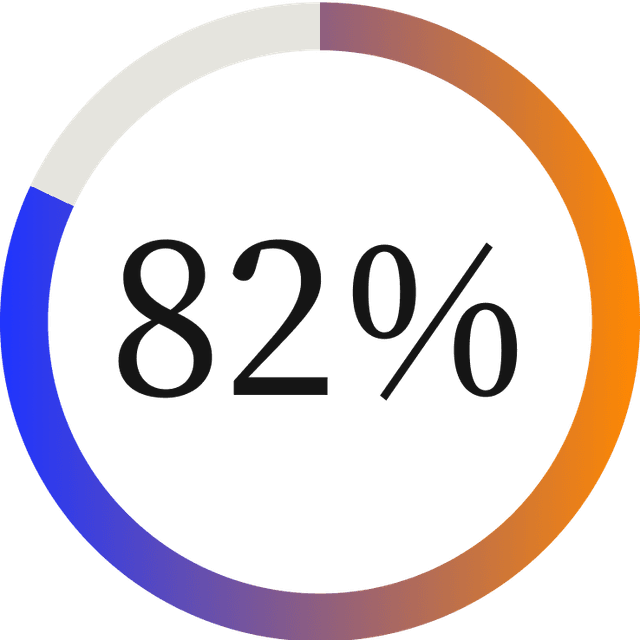

... of executives state that their company has lost work due to miscommunication in the payment process

The State of Digitization in B2B Finance is just a few clicks away!

Abstract

Customer experience (CX) is among the top priorities for executives business-wide—in fact, nearly 9 in 10 survey respondents (89%) agreed that “the C-suite is only as good as its customer experience.” Yet, most glaringly, the research found that executives aren’t doing enough to solve their self-proclaimed most pressing problem when undertaking the digital transformation of their accounts receivable departments.

We found that businesses primarily focus on automating internal processes while ignoring what’s most important to them—delivering exceptional customer experiences. When the human element in accounts receivable is broken, it’s known as the AR Disconnect. And automation alone won’t bridge the resulting communication gap that stems from an inability to collaborate directly with customers.

Despite the majority of executives agreeing that their AR department has work to do to be more customer focused (96%), most (65%) have not prioritized implementing collaborative AR tools (such as an online portal) in their digital transformation efforts, further perpetuating the AR Disconnect.