Cash vs. Accrual Accounting: The Basics, Benefits, and Business Implications

- 7 min read

The difference between cash vs. accrual accounting is the time at which income and expenses are recorded.

In this blog, we’ll explain the benefits and financial reporting implications of each, and which method is best for which companies.

When it comes to recording revenue, you have a choice between two main accounting methods: cash and accrual.

The differences between these methods are worth understanding because each has different tax, reporting, and financial planning implications for your business.

In this article, we’ll cover:

- What cash and accrual basis accounting are

- The differences between cash and accrual accounting

- Examples of accrual vs. cash transactions

- How to choose between cash vs. accrual accounting

- How AR automation software helps with managing accrual accounting

What is the difference between cash and accrual accounting?

The difference between accrual and cash basis accounting lies in the timing of when income and expenses are recorded on the business’ books.

In accounts receivable (AR), whether you use accrual or cash basis accounting will determine when you recognize revenue after making a sale on credit.

Cash basis accounting recognizes revenue when a payment is physically received in the business’ bank account.

In contrast, accrual accounting recognizes revenue when it's earned (i.e. the sale has been made), but the physical payment hasn't been received.

Here's a closer look at each accounting method, how they differ, and where those tax and financial planning implications come into play.

Accrual accounting

In the accrual principle, businesses must record a transaction in the same time period it originated, even if the actual cash isn’t received until much later. Companies report income when a sale is made rather than when the cash is received. Similarly, expenses are recorded when incurred (i.e. when an invoice has been received), not when paid.

This ensures revenue is properly matched against expenses, providing a more accurate picture of a company’s financial situation. Providing a correct representation of the company’s financial health is especially important for larger companies that report to external stakeholders like their board of directors.

That’s why both the International Financial Reporting Standards (IFRS) and the Generally Accepted Accounting Principles (GAAP) support accrual accounting.

The GAAP is the set of accounting principles set forth by the Financial Accounting Standards Board (FASB). The US securities law requires that all publicly traded companies (or any company that publicly releases financial statements) follow the GAAP.

Additionally, US businesses that average over $25M of gross receipts for the prior three years must use the accrual method, under Internal Revenue Service (IRS) requirements.

Cash basis accounting

In the cash basis method, companies report revenue once cash arrives in their bank account. By the same token, they’ll report expenses when actually paid. Cash basis accounting is often used by entrepreneurs, startups, and other small businesses.

Having control over the timing of revenue and expenses also provides a small business with more tax planning opportunities. For example, if a business had a great year, it might choose to prepay some expenses before the end of the financial year to shift a tax deduction to the current year.

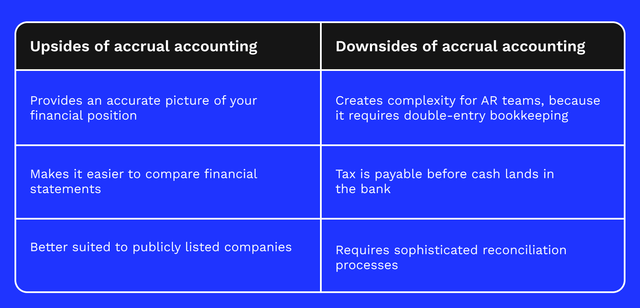

The pros and cons of the accrual method

The accrual method of accounting is better suited to the complex transactions of large businesses. For companies that make a high volume of sales on credit, accrual accounting makes it easier to track which payments are still owed to the company.

Accrual accounting also allows finance teams to account for future revenue, which supports financial forecasting and planning activities.

Accrual basis accounting does, however, have its set of challenges. For one, it requires more bookkeeping effort, as finance teams have to stay on top of receivables and expenses until payment has been made. It also creates the need for more frequent and complex account reconciliation.

Recording revenue before you’ve received payment also makes for a tricky situation when a customer doesn’t pay their invoice. To account for this, companies will create an allowance for doubtful accounts. This gives them a safety margin for bad debt that they can record in the same period as the original revenue.

While accrual accounting shows a more accurate picture of a company’s finances, it does have the potential to obscure short-term cash flow issues. This is because revenue reporting will include cash that is not yet usable to the business.

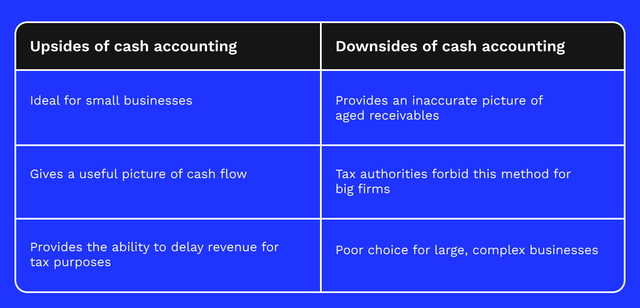

The pros and cons of the cash method

In cash basis accounting, it’s easier for accounting staff to record transactions as they’re only doing so when cash physically changes hands. This method also makes it easy for businesses to know exactly how much cash they have on hand. There’s also a tax benefit to the cash basis method, as companies don’t have to pay taxes for cash they haven’t received yet.

For these reasons, small businesses and solo entrepreneurs tend to favor cash accounting.

Cash accounting, however, doesn’t allow you to account for future revenue. This makes it difficult to stay on top of sales made on credit—especially if you make a lot of them. This also makes it impossible to gauge what the company’s financial position will be beyond the present moment. This makes the cash method unuseful for forecasting and planning.

Because outside parties can’t get a forward-looking view of a company’s financial statements, the cash method is not permitted under the GAAP, exempting larger companies from using it.

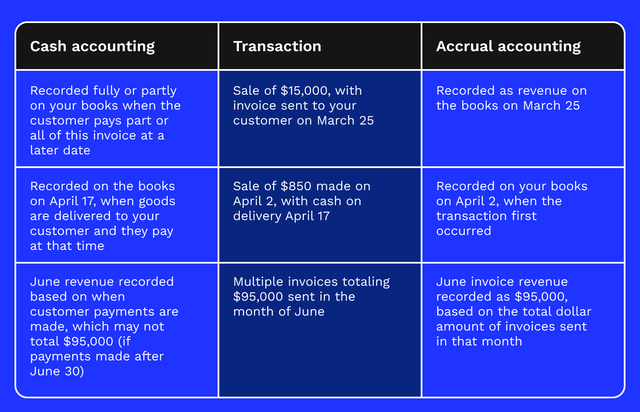

Examples of accrual vs. cash transactions

Whether AR teams use accrual or cash basis accounting will impact how they record revenue.

Here’s a breakdown of how you would record revenue for the same transactions under the cash vs. accrual accounting methods:

What does it mean to record transactions?

The examples above mention how transactions are recorded. Here’s a quick overview of what that actually means:

- When a business provides goods or services on credit, it records the transaction in accounts receivable.

- This record is stored on a financial statement called a ledger. This ledger tracks all the money that is owed to the business by its customers.

- Recording transactions helps businesses understand what they are owed, who they owe, and what tax obligations or deductions they need to prepare for.

Choosing between cash vs. accrual accounting methods

It’s a given that large companies (especially public ones) will be using the accrual method due to the GAAP and IFRS. Cash accounting doesn’t give the clear picture of financial performance that's needed for key stakeholders like tax authorities, regulators, and investors.

For smaller companies, the choice of accounting methods is less clear. Small business owners and startups should stick with cash accounting where they can, purely for the simplicity and efficiency it provides their small teams and resource availability. If your intent is to eventually scale the business, however, then it’s best to be using the accrual method.

Supporting accrual accounting with AR automation

Making the choice to run your business with the accrual method of accounting is much easier when you know there’s technology out there to help you.

With accounts receivable automation software, finance teams can streamline every aspect of the receivables lifecycle: invoicing, collections, dispute management, payment processing, and cash application.

Invoice matching and revenue recognition—the key processes you need for sound accrual accounting—can be automated too, making it easier to reconcile cash inflows and close books faster.

—

Learn how you can automate manual AR work, reduce errors, and improve your customers’ payment experience with Versapay’s collaborative AR automation solution.

Always stay up-to-date

Subscribe

Join the 50,000 accounts receivable professionals already getting our insights, best practices, and stories every month.