A Finance Leader's Guide to AI-Powered Cash Application

With advanced cash application automation technology, you can harness powerful, high-tech tools to make your cash application process smarter, faster, and stronger.

Drive Efficiencies with AI-Powered Cash Application Automation Software

October 17th, 2023

This guide for finance leaders explores how advanced cash application automation can:

→ Transform your accounts receivable

→ Drive efficiency and reduce manual labor

→ Make matching payments with open receivables simple and easy

Plus, get tips on selecting the right partner for your advanced cash application automation solution.

What's inside this guide?

With advanced cash application automation technology, you can harness powerful, high-tech tools to make your cash application process smarter, faster, and stronger. Here's what you'll find within:

- What cash application is and how it works

- The risks of manual cash application and applying payments incorrectly

- How to accelerate cash flow with advanced cash application automation

- Real-world cash application automation success stories

- And much, much more

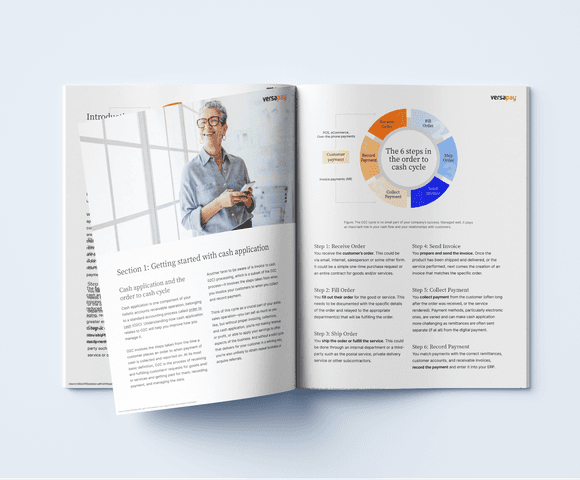

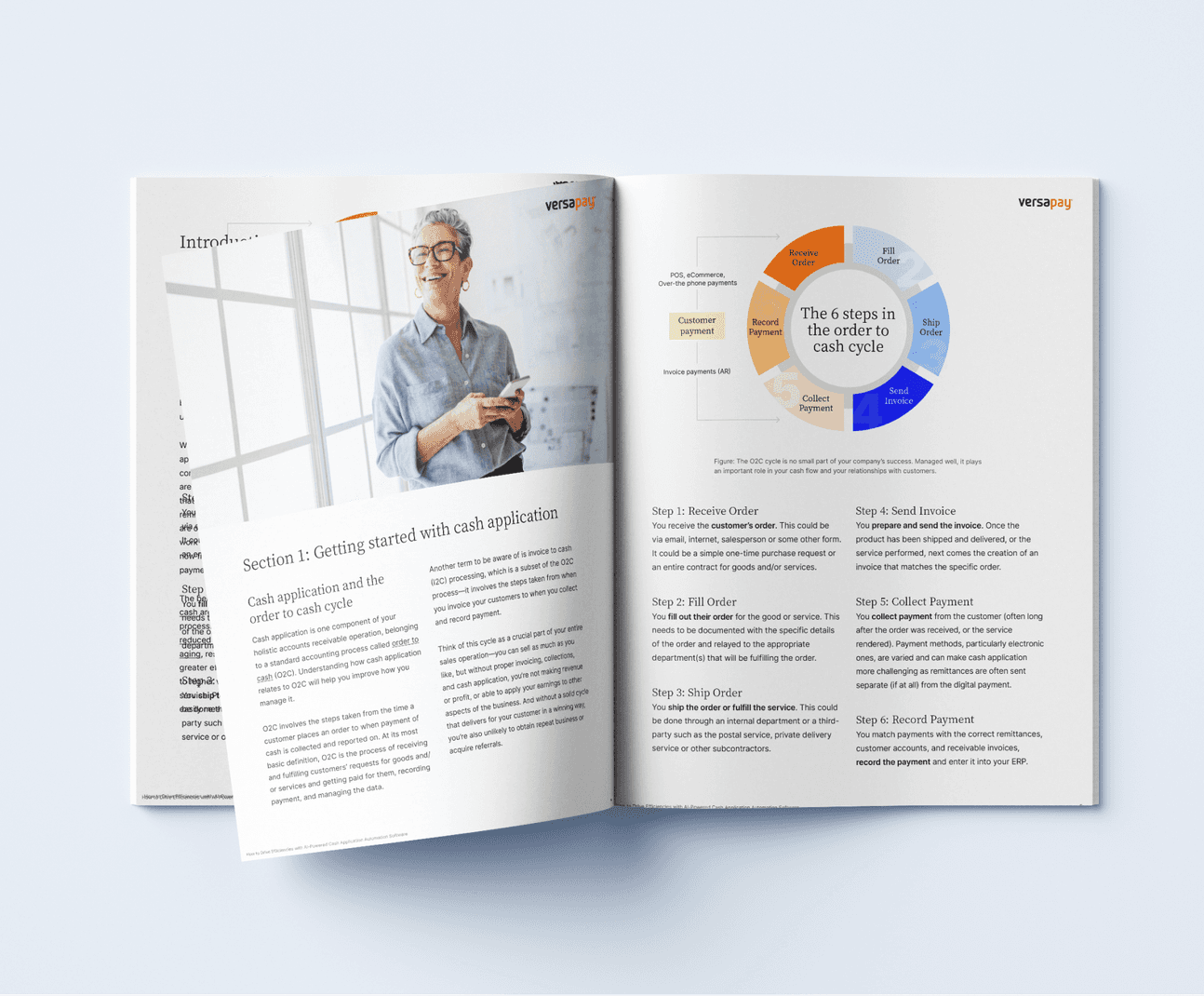

Section 1: Getting started with cash application

Cash application and the order to cash cycle

Cash application is one component of your holistic accounts receivable operation, belonging to a standard accounting process called order to cash (O2C). Understanding how cash application relates to O2C will help you improve how you manage it.

O2C involves the steps taken from the time a customer places an order to when payment of cash is collected and reported on. At its most basic definition, O2C is the process of receiving and fulfilling customers’ requests for goods and/ or services and getting paid for them, recording payment, and managing the data.

Another term to be aware of is invoice to cash (I2C) processing, which is a subset of the O2C process—it involves the steps taken from when you invoice your customers to when you collect and record payment.

Think of this cycle as a crucial part of your entire sales operation—you can sell as much as you like, but without proper invoicing, collections, and cash application, you’re not making revenue or profit, or able to apply your earnings to other aspects of the business. And without a solid cycle that delivers for your customer in a winning way, you’re also unlikely to obtain repeat business or acquire referrals.

Step 1: Receive Order

You receive the customer’s order. This could be via email, internet, salesperson or some other form. It could be a simple one-time purchase request or an entire contract for goods and/or services.

Step 2: Fill Order

You fill out their order for the good or service. This needs to be documented with the specific details of the order and relayed to the appropriate department(s) that will be fulfilling the order.

Step 3: Ship Order

You ship the order or fulfill the service. This could be done through an internal department or a third- party such as the postal service, private delivery service or other subcontractors.

Step 4: Send Invoice

You prepare and send the invoice. Once the product has been shipped and delivered, or the service performed, next comes the creation of an invoice that matches the specific order.

Step 5: Collect Payment

You collect payment from the customer (often long after the order was received, or the service rendered). Payment methods, particularly electronic ones, are varied and can make cash application more challenging as remittances are often sent separate (if at all) from the digital payment.

Step 6: Record Payment

You match payments with the correct remittances, customer accounts, and receivable invoices, record the payment and enter it into your ERP.

The benefits of streamlining the order to cash process

Businesses large and small face challenges when making sure payments are correctly posted—think of the times you needed to apply a discount, a customer paid multiple invoices at once, or a balance was paid through multiple accounts. Manually managing that can require a lot of work and there is potential for error, cost overruns, delays in getting paid, and customer dissatisfaction.

And while manual processes—often involving reams of paper and many labor hours—have been the standard in B2B accounting for decades, forward-thinking companies are now turning to technology and automated software solutions more than ever to drive greater efficiencies across the entire O2C cycle, cash application included.

Here are the four benefits of streamlining and automating O2C:

- Customers are served more quickly and efficiently

- Fewer errors are made, and less delays are incurred

- Cash flow is vastly accelerated

- Data captured is more thoroughly analyzed, and opportunities for improvement are identified

What cash application is and how it works

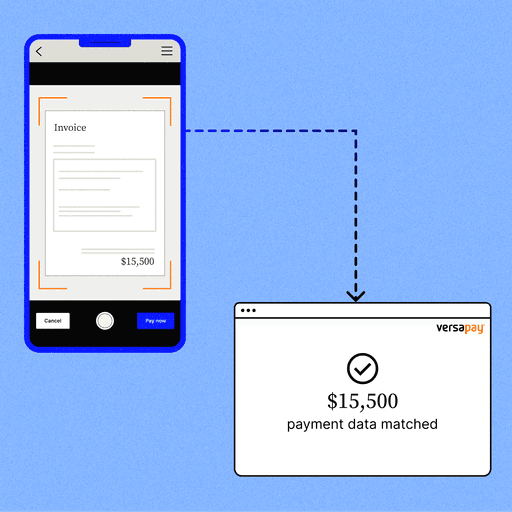

Cash application is a process that’s key to the entire O2C cycle. It involves matching incoming payments to remittance information and their corresponding invoices. It also comprises reviewing payments made by check, credit card, electronic fund transfer (EFT), automatic clearing house (ACH), and many other payment methods, matching them to open invoices and marking them as paid.

The two crucial business functions efficient cash application impacts

- Financials—It increases straight through processing rates, lowers accounts receivable processing costs, reduces DSO, and results in more timely financial closing.

- Non-Financials—Increasing efficiencies reduces time spent manually applying cash, enables the reallocation of resources to higher value work, and improves customer service.

What your cash application system should provide

- Accuracy—Your accounts receivable should not have errors. Errors can lead to delays and poor customer experiences.

- Speed—In applying cash more quickly, you’re able to reduce your DSO, significantly lower AR processing costs, and ensure your business has access to its cash more quickly.

- Standardization—Standardized cash application processes eliminate inefficiencies and reduce compliance issues.

The three crucial pieces of data for cash application

- Invoices—These are the original bills that prompt payments to be made.

- Payments—These are the funds transferred from your customer to you.

- Remittances—These describe why a payment is being made (either through an invoice number or—in some cases—payment information detailing why a customer made a partial payment, whether discounts have been applied, or what the payment terms are).

So, you have a variety of payment sources and then a variety of remittance sources—and all that information needs to be matched up and reconciled.

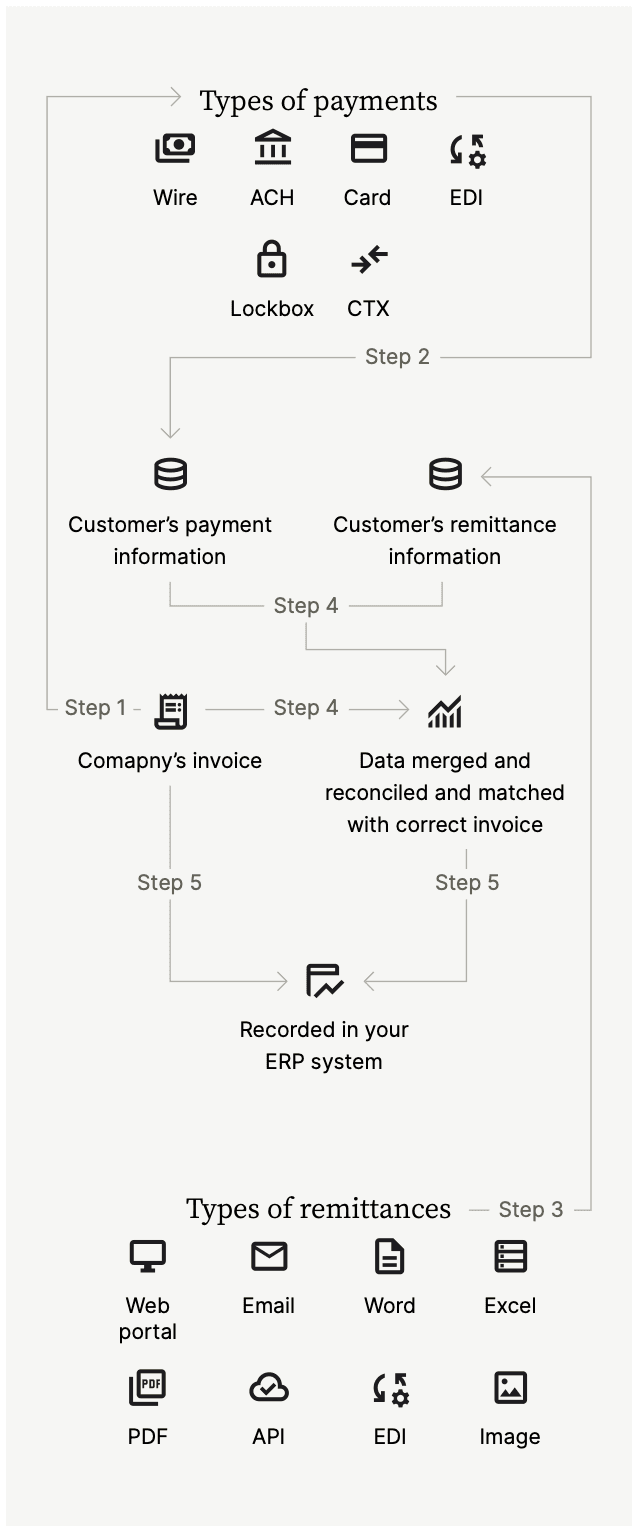

The cash application flowchart

While no two companies follow the same cash application process—because companies vary in nature, size, volume of customers, quantity of invoices, and delivery and payment methods—there are general steps common to most.

- Step 1: Your team prepares an invoice requesting payment for a goods or services and sends it to your customer—via email, mail or courier, fax, cloud-based portal or in person.

- Step 2: You receive payment via check, wire transfer, credit card payment, automated clearing house (ACH), electronic data interchange (EDI) or corporate trade exchange (CTX).

- Step 3: Your customer sends remittances (which specify why the payment was made or for what invoices) either with the payment in the case of checks or separately via emails, Excel files, PDFs, web portals or image scans.

- Step 4: All the data needs to be reconciled to ensure the information from the invoices and remittances matches with the payments made, either manually or through an automated process. Any discrepancies (for instance in the event a customer has made a partial payment) need to be investigated and resolved.

- Step 5: Once reconciled, the payment gets officially recorded in your company’s enterprise resource planning (ERP) system, where day-to- day business operations such as accounting are managed.

- Step 6: The finished work and process is

reviewed to look for any ways to optimize it.

Your AR team might also send receipt of payment to customers.

How changing payment trends are impacting the cash application process

The move to digital payments has been fuelled by such factors as the need for cost savings and improved efficiency (ACH payments are cheaper and take less time to process than checks), the need for improved cash management and reporting capabilities, regulations making electronic payment methods easier and more secure, large players like Walmart and Amazon mandating digital payments with suppliers and customers, and the general growth of ecommerce in the B2B space.

Customers, too, are driving this trend with increased demand to pay using digital methods that they are accustomed to using as consumers, which is more convenient and results in a better customer experience.

And with payment trends increasingly going digital, AR departments and their cash application processes are undergoing a massive shift, with executives looking for opportunities to optimize their accounts receivable practices.

Section 2: The risks of manual cash application and applying payments incorrectly

Many are involved in cash application—accountants, data entry clerks, bank personnel, postal and delivery workers, IT support workers, as well as software like payment processors and ERPs. When done manually, cash application is labor-intensive, with many specialists relying on Excel to perform data entry and analysis. The nature of these processes is time-consuming and prone to errors, leading to losses in productivity and increases in costs.

These are the challenges you’ll want to conquer in your cash application process.

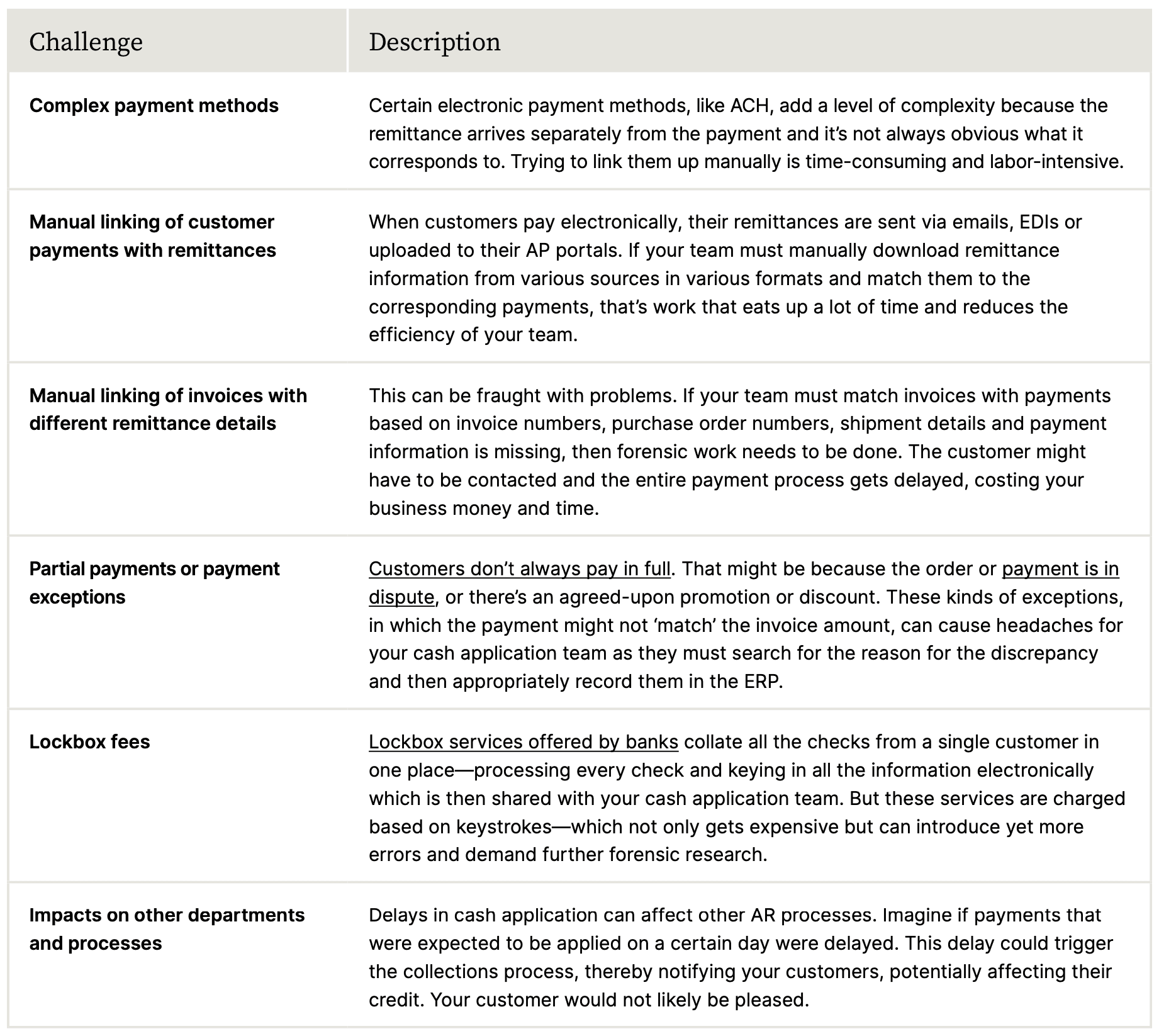

If your B2B operation is small—less than 1,000 invoices processed each month—the complexities of cash application might not be as onerous, even with a manual system. But what if you have thousands of customers operating in different jurisdictions and whose payment methods, such as ACH, have remittances that arrive separately from multiple sources?

Another somewhat recent challenge for AR departments has been extracting remittances from web portals, which started when many large operators such as Walmart and Amazon set up web portals as a cheaper way to deliver remittances, forcing suppliers to comply.

All these nuances and complexities can make it difficult to track what information corresponds with what. Also, errors and payment processing delays are more likely to occur, affecting how much capital your business has available to use in its operations. Even if there aren’t errors, the time and energy spent on manual cash application could be better utilized elsewhere in your business.

The challenges of matching payments with open receivables

What frequent misapplication of payments means for your business

Until you’ve formally recorded an incoming payment in your accounting system, you can consider that cash non-existent. That’s why being able to quickly—and correctly—apply incoming payments is so important.

Traditional cash application processes, however, compromise this, as they’re error-prone, time- consuming, and resource-intensive. And rather than isolate and remedy the root cause of these challenges, many businesses opt for employing multiple full-time accounting specialists to work exclusively on cash application due to the effort involved.

In fact, approximately 85% of finance leaders are still manually matching payments with remittance information. And nearly 20% claim this is their process for all their payments.

Applying a customer’s payment to the wrong invoice could mean their balance remains open when it shouldn’t. If the customer has surpassed their allowed credit limit, this error could prevent them from making any more purchases from you.

Frequent misapplication of payments also means your AR team will be forced to seek clarification from customers on what to do with their payment on a recurring basis. Much of this stems from having no clear way to manage short payments, payments lacking remittance information, or payments covering multiple invoices.

Plus, highly manual cash application processes involve unnecessary flipping between multiple Excel spreadsheets, payment systems, and your ERP—which introduces numerous opportunities for data entry errors.

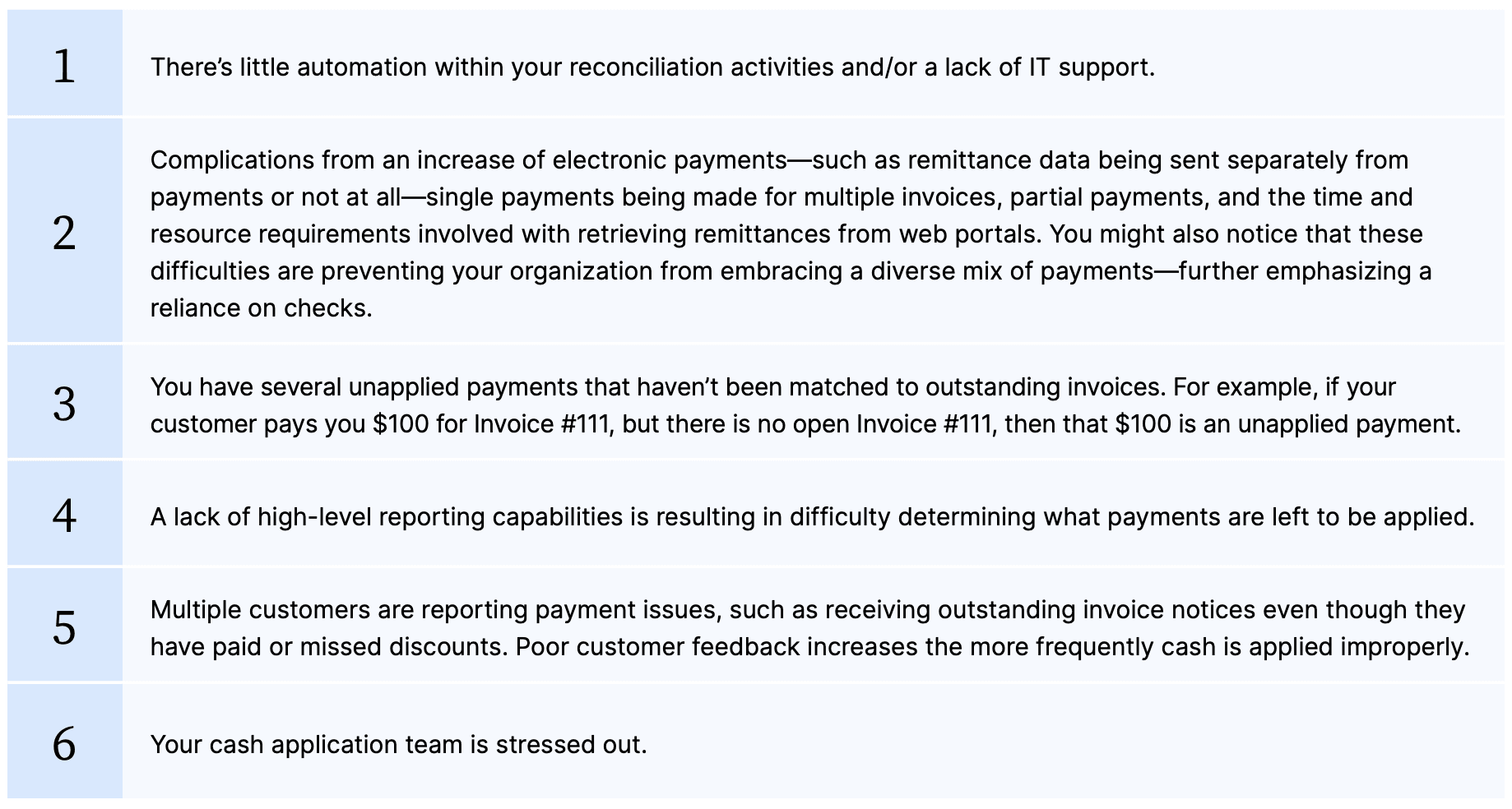

The signs your cash application efforts are inefficient

As you can see from some of the challenges we’ve discussed, or perhaps from your own painful experiences with cash application, highly manual and inefficient processes harm your business and create poor customer experiences.

What are the signs you need help?

If you’re noticing any of these symptoms in your organization, you should consider a better cash application solution:

How can you monitor if your cash application efforts are working well?

- The speed at which payments are being applied—Once remittance data has been received, how quickly are payments being applied? Is it the same day? The next day? The following week? Ideally cash is applied as quickly as possible. The longer cash goes unapplied, the less readily available cash you’ll have on hand.

- Whether or not cash application errors are present—The more payments you receive, the higher the likelihood of cash application errors occurring. While cash application specialists are exceedingly diligent, meticulous and thorough, any matching work that’s performed manually is still subject to errors. Automation can significantly decrease the likelihood of errors—striving for zero errors is recommended.

- The volume of remittances received—A lack of remittance data means further clarification is required on behalf of the cash application specialist before they’re able to match payments with the correct customer account and open receivable. To prevent slowing down the cash application process, you’ll want to monitor what percentage of payments are received without remittance data and work at reducing that volume.

AI-powered cash application versus manual cash application

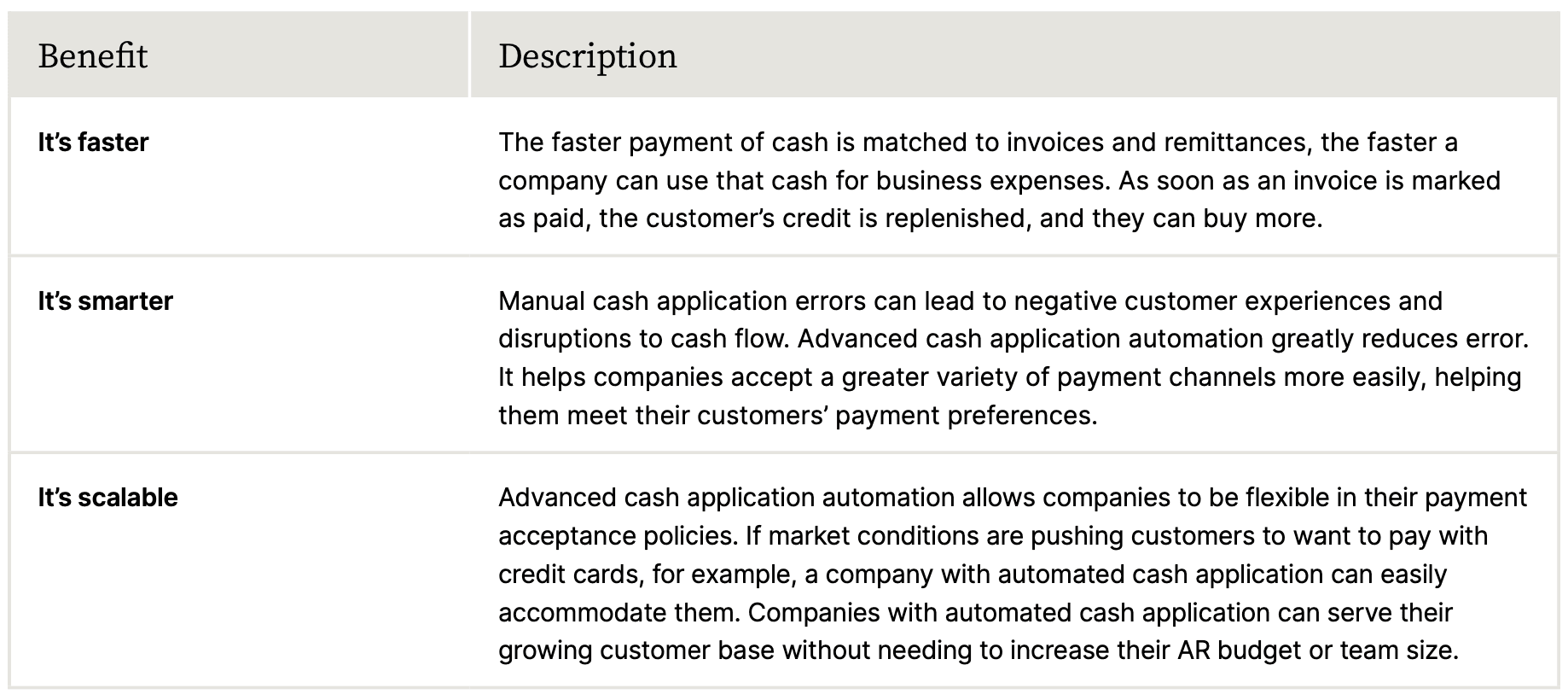

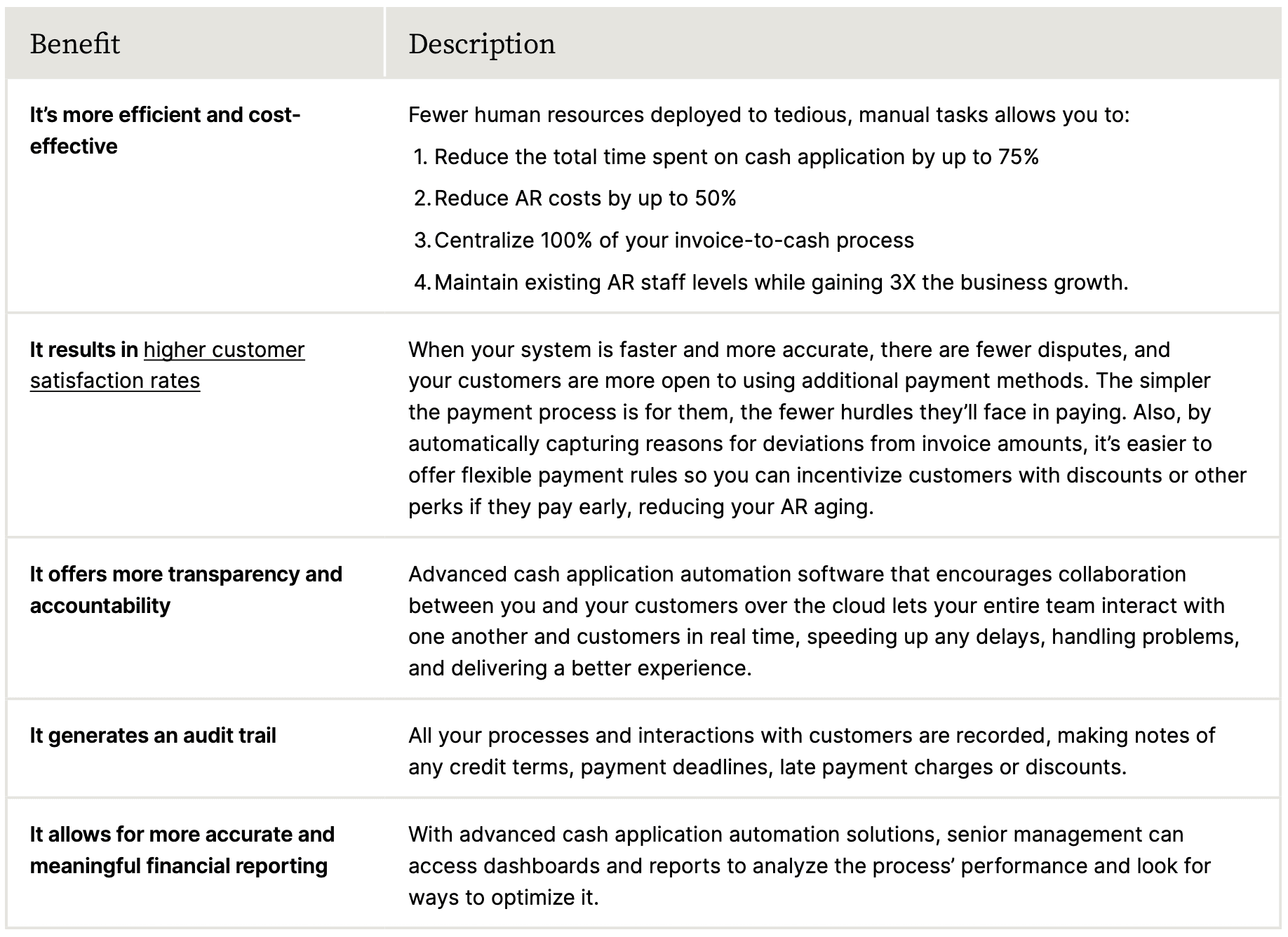

Here are eight benefits of advanced cash application automation over manual application:

Benefits 1 to 3:

Benefits 4 to 8:

🎥 Want to see artificial intelligence in action? The video above looks at how Madison Resources transformed cash application with Versapay:

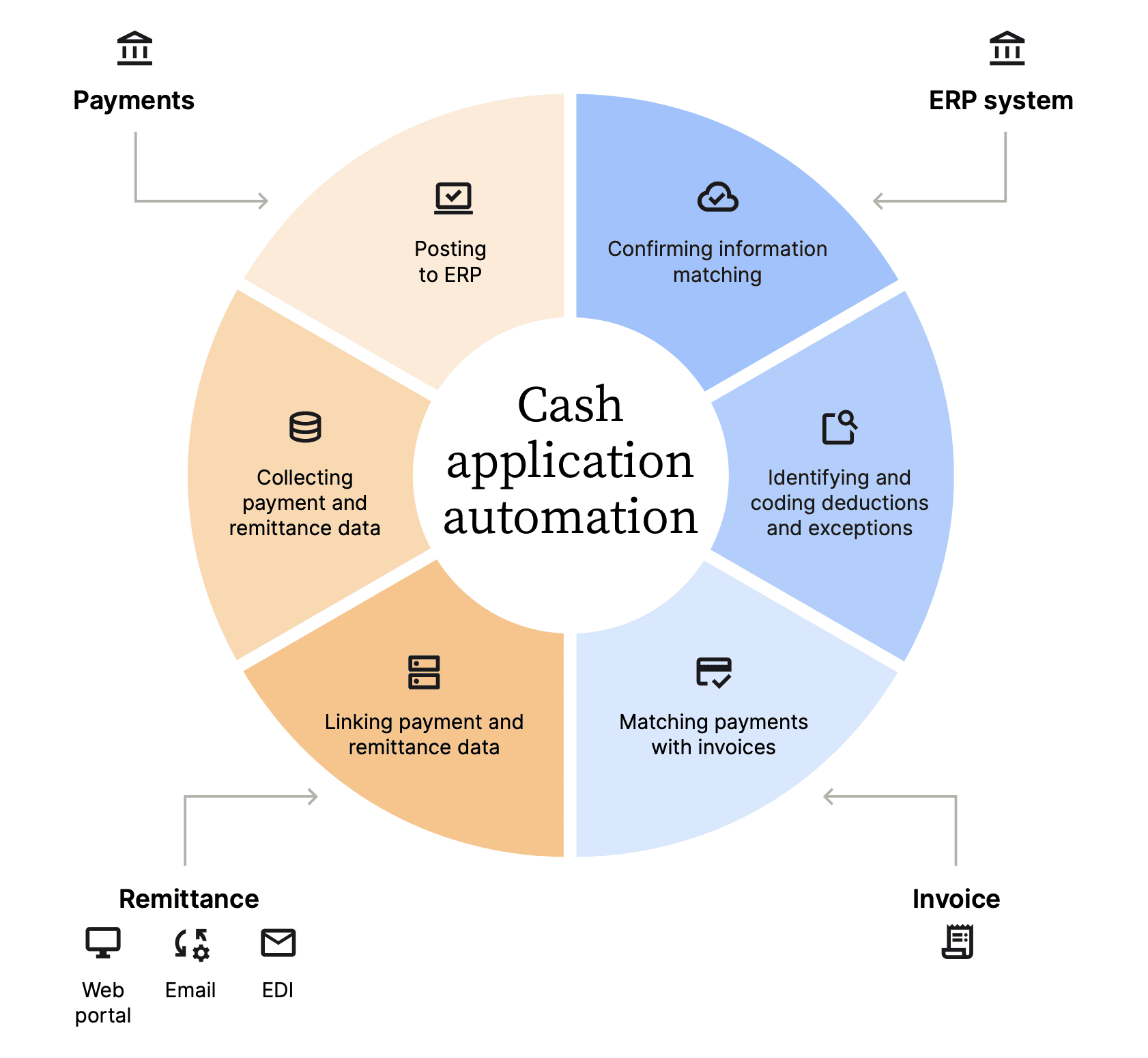

So, what can automation help you with?

A little bit of everything! Look at this graphic for an idea of where cash application automation can lend a helping hand:

How to evaluate cash application automation solutions

The best cash application solutions solve all the challenges discussed in this guide and drive major efficiency improvements by automating the majority of manual work. That way you can reap the benefits—resulting in a better operation for you and your customers.

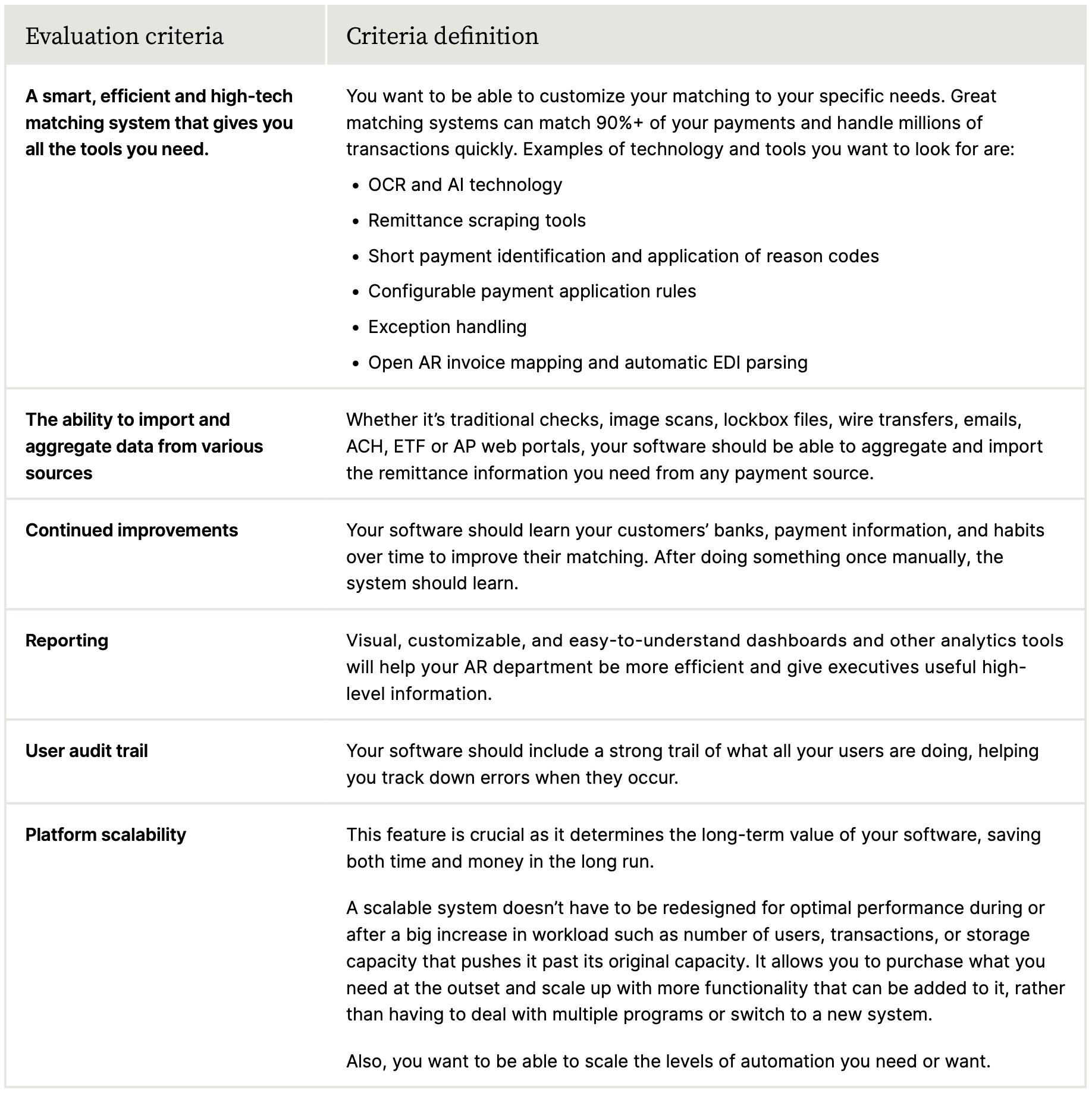

The cash application automation solution evaluation criteria (1 to 6):

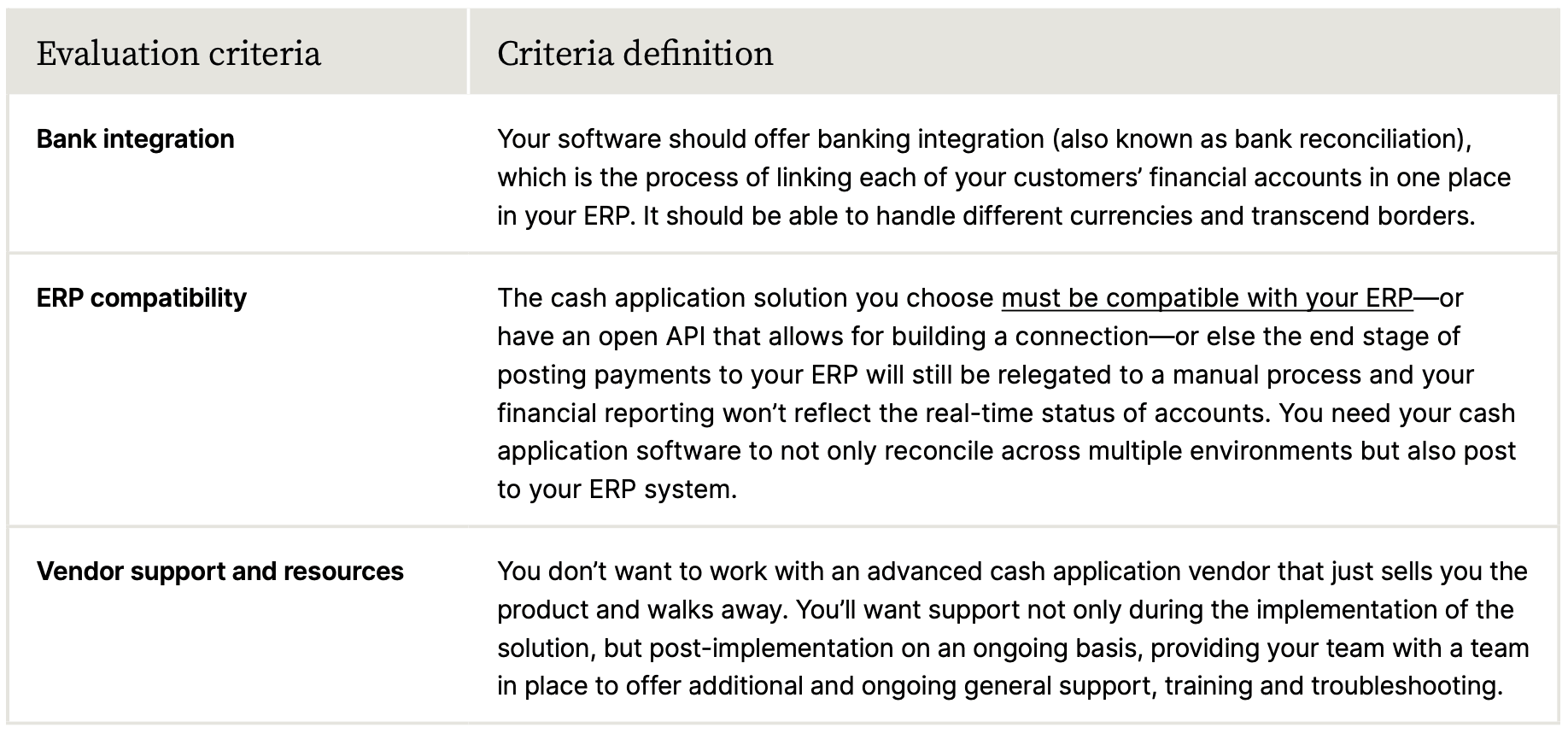

The cash application automation solution evaluation criteria (7 to 9):

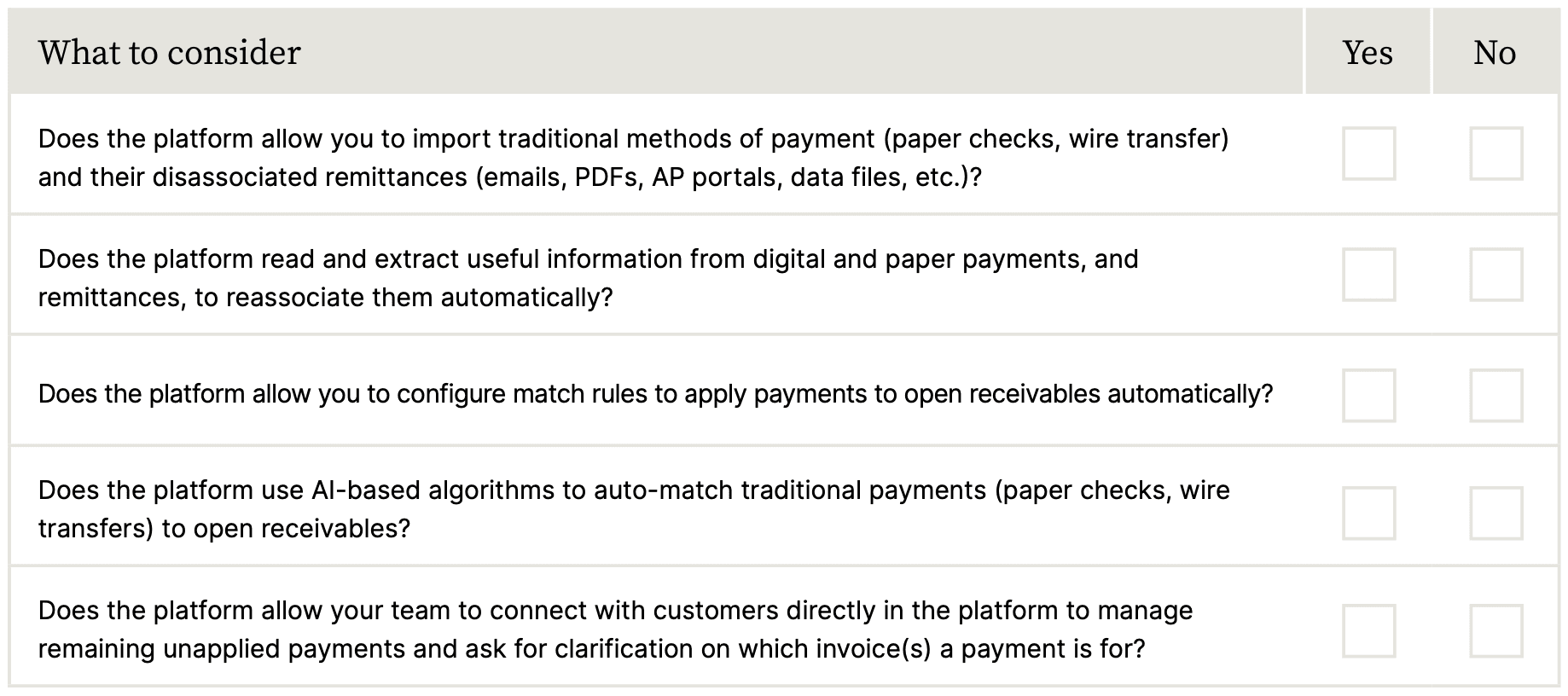

The cash application automation solution checklist:

Section 4: Real-world accounts receivable automation success stories

This healthcare service provider gives 4.5 hours back to cash application specialists daily with automation

Demand for services of this healthcare company skyrocketed; yet while explosive growth is tantamount to winning the jackpot for most, surprise growth often comes with a cost.

For a company relying on highly manual accounts receivable processes, facing unprecedented sales meant having to compensate by exhausting resources to perform daily, essential tasks like cash application. And unfortunately, daily often meant working until 10:00PM.

With cash application automation, this healthcare services provider streamlined their cash application process, and in turn made their customers happier. And, since implementing Versapay, they’ve redeployed numerous teammates to take on higher value, more strategic projects.

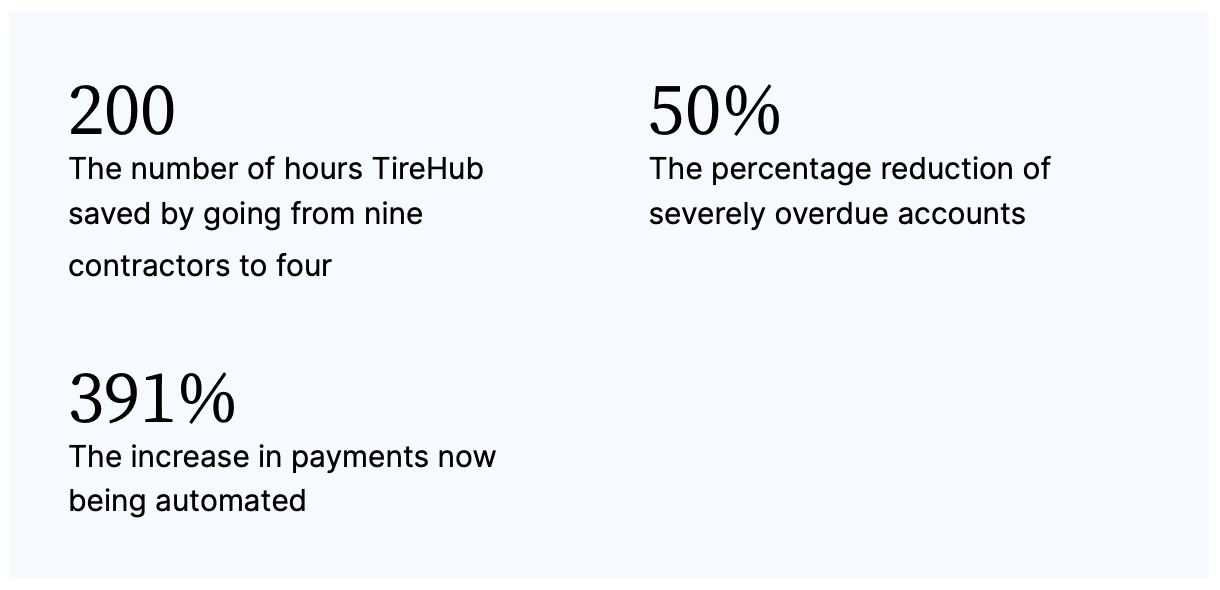

Automated cash application helps TireHub move resources to a higher class of problem solving

TireHub is a joint venture of tire manufacturing giants Goodyear and Bridgestone, serving as a last-mile service provider for both.

Taking on last-mile operations meant inheriting those companies’ existing client bases—and the varying billing and discounting practices those customers were used to.

With cash application automation, TireHub was able to reduce the application errors previously faced with their manual processes, allowing them to uncover considerable operational savings and strengthen their relationships with customers.

“With that much manual cash application, you’re bound to make mistakes,” says Matt Marin, TireHub’s Senior Manager of Financial Processes and Data Management. “And that was causing frustration for our customers. We also couldn’t hold customers accountable for what they owed when we were misapplying payments and credits. We were really struggling to manage our accounts and our customers were frustrated with the mistakes we were making.”