The Ultimate Guide to Credit Card Processing

Learn how credit card processing technology can speed up and automate payments, reduce manual processes, accelerate cash flow, and more!

Gotta run? Download the designed PDF (for free!) instead

The Ultimate Guide to Credit Card Processing

April 19th, 2023

This guide will help you understand how credit card processing technology can:

✓ Speed up and automate payments

✓ Reduce manual processes

✓ Accelerate cash flow

✓ Drive more revenue, and

✓ Empower crucial staff to perform more strategic activities

This guide explores:

- The rise of credit card use

- The entities involved in the credit card processing ecosystem

- The different processing fees and pricing models

- How you can save money through interchange optimization

- How to prevent security breaches and data theft

- How to ultimately choose the right credit card processor for your unique business

The state of credit card use

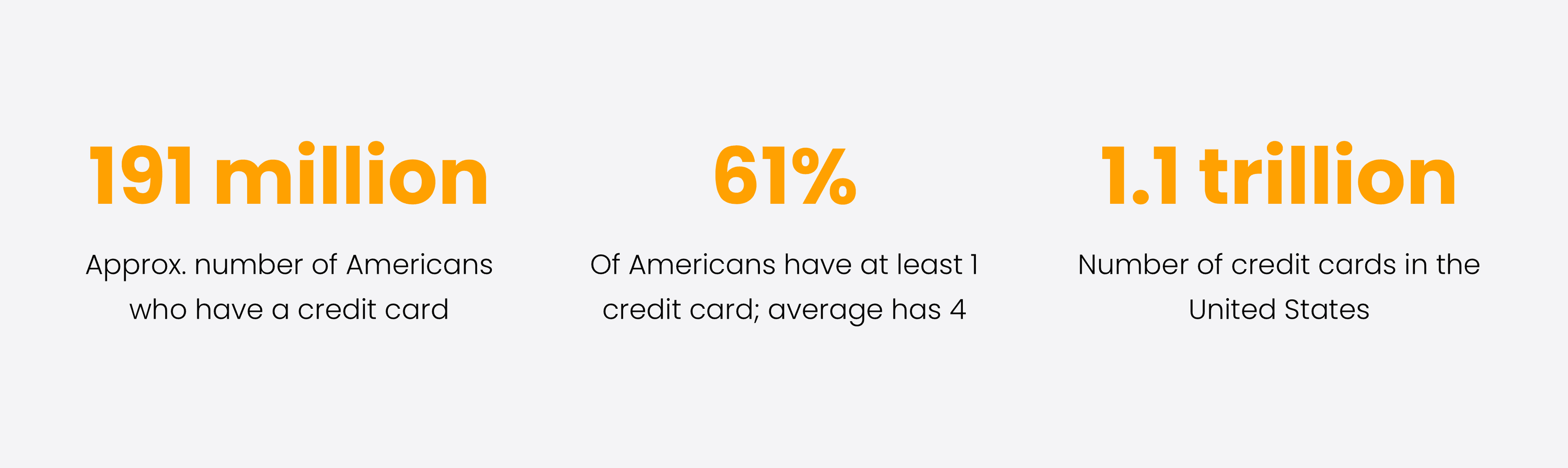

The credit card processing system we know today goes back decades. American Express issued the first plastic credit card in 1958, and revolving balances and finance charges were introduced a year later. Today, credit card use is ubiquitous, and it would be hard to imagine life without them. Hundreds of institutions around the world—including banks, credit unions, retailers, and finance companies—offer credit card products.

In the past five years, the use of cash among consumers has declined in the United States, while the use of credit has increased.

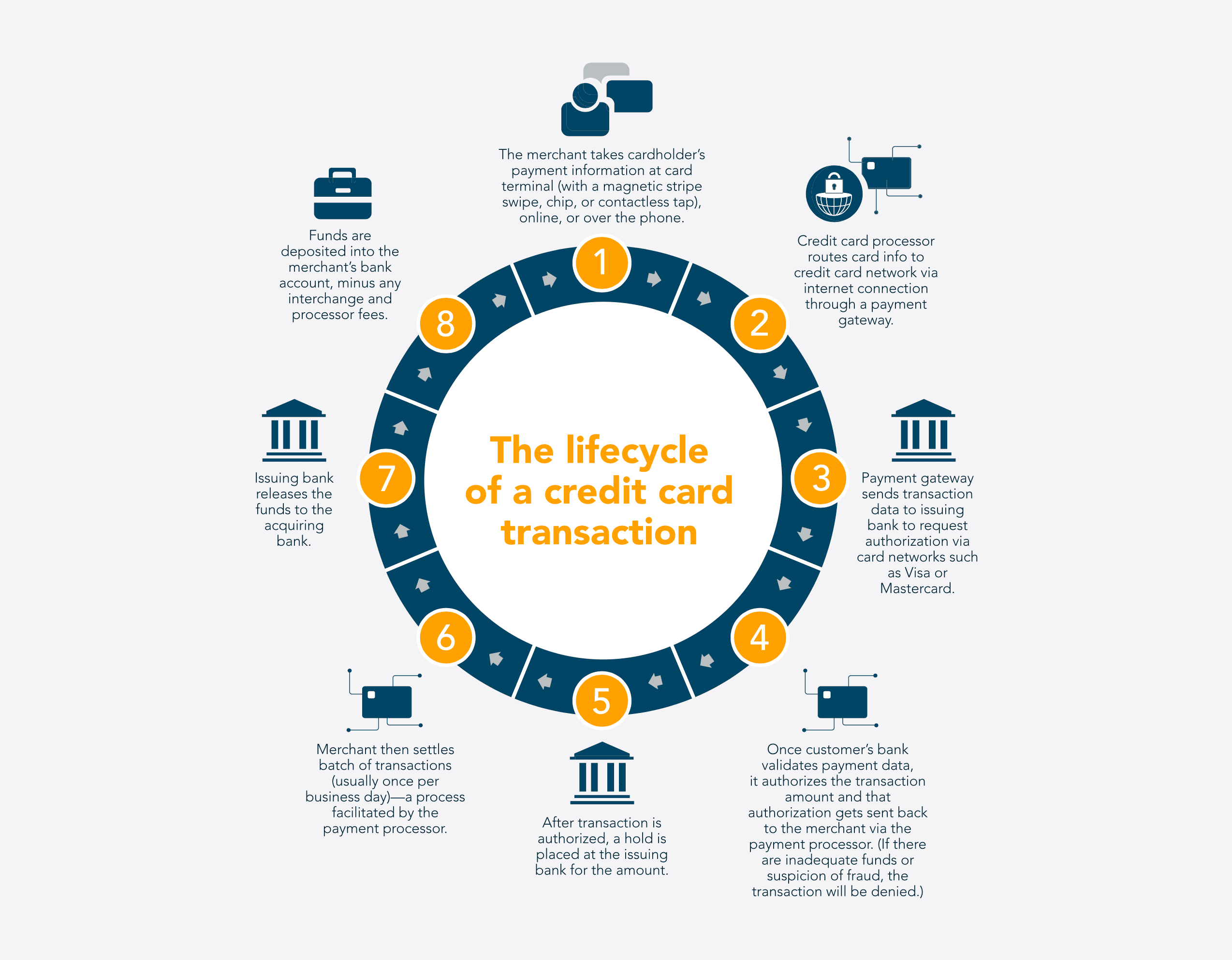

The lifecycle of a credit card transaction

- Step 1: The merchant takes cardholder’s payment information at card terminal (with a magnetic stripe swipe, chip, or contactless tap), online, or over the phone.

- Step 2: Credit card processor routes card info to credit card network via internet connection through a payment gateway.

- Step 3: Payment gateway sends transaction data to issuing bank to request authorization via card networks such as Visa or Mastercard.

- Step 4: Once customer’s bank validates payment data, it authorizes the transaction amount and that authorization gets sent back to the merchant via the payment processor. (If there are inadequate funds or suspicion of fraud, the transaction will be denied.)

- Step 5: After transaction is authorized, a hold is placed at the issuing bank for the amount.

- Step 6: Merchant then settles batch of transactions (usually once per business day)—a process facilitated by the payment processor.

- Step 7: Issuing bank releases the funds to the acquiring bank.

- Step 8: Funds are deposited into the merchant’s bank account, minus any interchange and processor fees.

How to save money on credit card processing

If you’re looking to save on costs for credit card processing—as B2B companies especially are— you’ll want to know about interchange optimization.

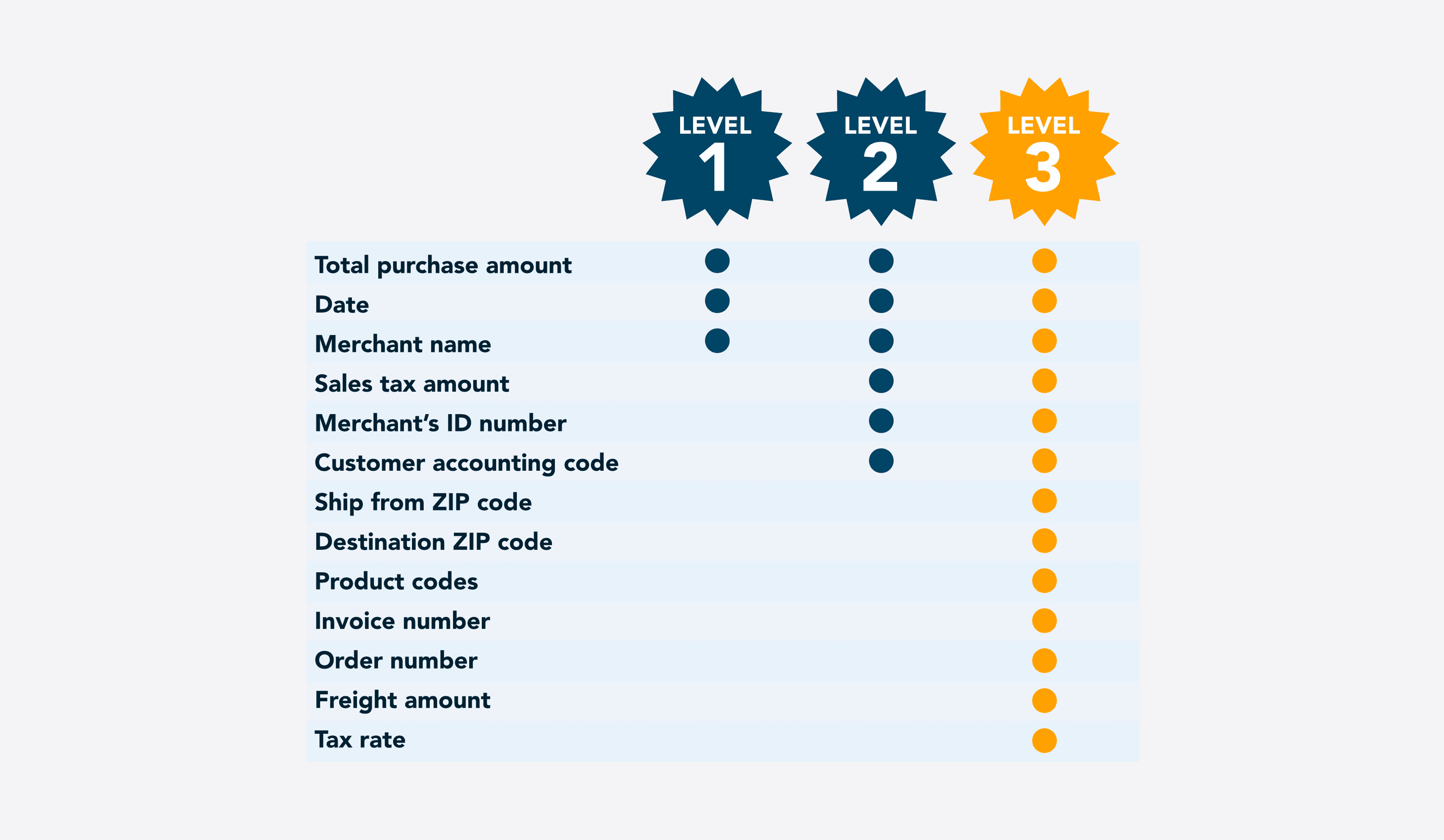

B2B businesses often rely on corporate and commercial cards, whose interchange rates can be higher than consumer cards. But that rate can be substantially reduced by passing more information to the credit card brands.

Most transactions pass along basic data—known as Level 1. But there are other levels of data—Level 2 and Level 3—and passing along high levels of data makes the transaction more secure. And the more secure your transactions are, the less risk there is to credit card companies, which leads them to reward you with lower interchange costs.

The most sophisticated payment processors offer interchange optimization as a service to help businesses save on processing fees—in some cases, up to 40%. Reducing interchange fees by as little as one percent can be invaluable when dealing with transactions of large value—as is usually the case in B2B—and can boost your bottom line or help you direct your money to other much-needed areas of the business.

Secure and protect sensitive credit card data

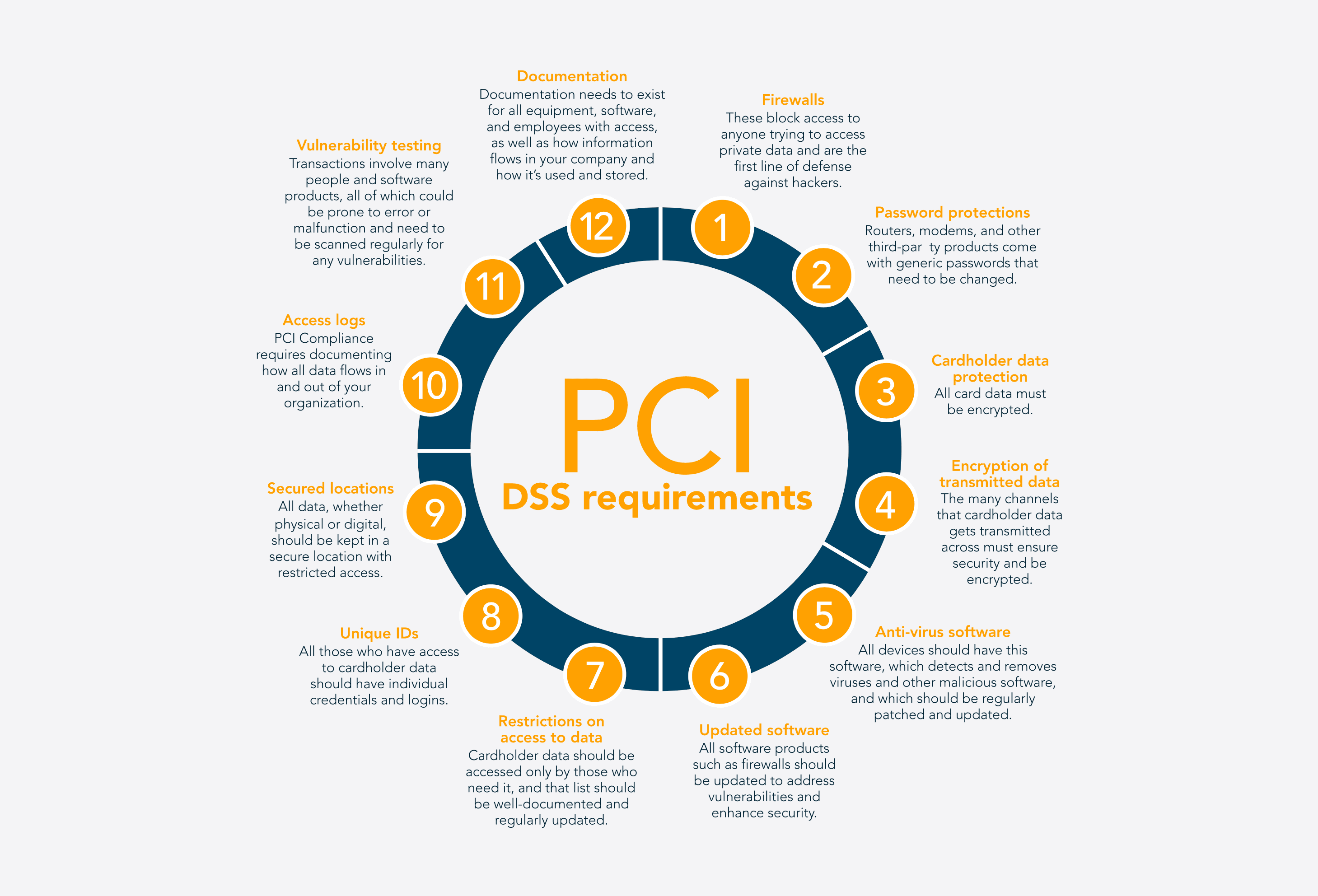

In the digital world, where very sensitive cardholder data is being transmitted, protecting that data is crucial. The Payment Card Industry Data Security Standard (PCI DSS) is the global set of requirements intended to ensure that all companies process, store and transmit credit card information in a secure environment. There are 12 main requirements for PCI DSS compliance that apply to merchants and credit card processors:

- Firewalls: These block access to anyone trying to access private data and are the first line of defense against hackers.

- Password protections: Routers, modems, and other third-party products come with generic passwords that need to be changed.

- Cardholder data protection: All card data must be encrypted.

- Encryption of transmitted data: The many channels that cardholder data gets transmitted across must ensure security and be encrypted.

- Anti-virus software: All devices should have this software, which should be regularly patched and updated.

- Updated software: All software products such as firewalls should be updated to address vulnerabilities and enhance security.

- Restrictions on access to data: Cardholder data should be accessed only by those who need it, and that list should be well-documented and regularly updated.

- Unique IDs: All those who have access to cardholder data should have individual credentials and logins.

- Secured locations: All data, whether physical or digital, should be kept in a secure location with restricted access.

- Access logs: PCI Compliance requires documenting how all data flows in and out of your organization.

- Vulnerability testing: Transactions involve many people and software products, all of which could be prone to error or malfunction and need to be scanned regularly for any vulnerabilities.

- Documentation: Documentation needs to exist for all equipment, software, and employees with access, as well as how information flows in your company and how it’s used and stored.

Your business should at minimum be PCI-compliant—this is the starting point for securing your systems and data. If your customers trust you with their sensitive data, that translates to increased confidence and repeat business. It also makes you a partner in the global effort to prevent security breaches and data theft.