What Are Integrated Payments? How They’ll Streamline Your Accounts Receivable

- 7 min read

In this blog, you’ll learn:

- What integrated payments are

- How integrated payments work

- 5 ways integrated payment processing benefits AR teams

- How to get started with integrated payment solutions

As any accounts receivable (AR) professional will tell you, one of the most tedious parts of their role is matching payments to invoices.

To alleviate this kind of manual AR work, it’s essential to integrate as much of your finance tech stack as possible. When systems talk to one another, this creates opportunities to automate processes that would otherwise take countless hours.

This is where integrated payments are especially valuable. In this article, we'll explain what integrated payments are, how integrated payment systems work, and how to get started with integrated payment processing.

What are integrated payments?

Integrated payments work by connecting the infrastructure your business needs for payment processing with your core software systems. These core systems could be Enterprise Resource Planning (ERP) solutions or accounting software.

That way, payment information travels to your main financial management software automatically. This saves AR teams significant effort by not having to post payments manually.

This capability is especially important as businesses grow. While manually posting payments might work for your team right now (though your cash application specialists might beg to differ), things will only get tougher as your sales increase and payment volume grows. Delaying the process of cash application can cause trouble if you employ credit limits, as customers may not be able to buy from you while they wait for their credit to be replenished.

With an integrated payment system, you’re able to scale your payment acceptance processes without the need for more headcount. If you plan on switching ERPs, this is an especially good time to implement integrated payments.

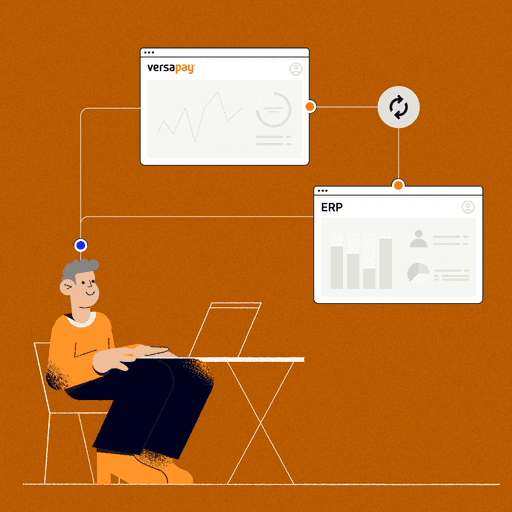

How do integrated payments work?

Here is an overview of how integrated payment systems work in tandem with your ERP or financial management system:

Step 1: Customer makes a payment through any sales channel

Many integrated payment solutions handle payments from a variety of sources. Versapay lets you accept payments across your point of sale, ecommerce, and accounts receivable channels—directly in your ERP. This includes all your customers’ favorite payment methods like credit and debit cards, ACH, virtual cards, and bank payments.

Step 2: Your ERP captures all the payment information thanks to integration

With payment information feeding automatically into your ERP, once a customer has made a payment, you’ll see it populate in your system automatically. The payment will be applied to the corresponding invoice automatically, minimizing errors and saving hours of manual matching.

Step 3: You can post the transaction to the right ledger

With your customer’s payment appearing in your cash receipts journal automatically, your work is basically done. You can then post the payment to the customer ledger with just a few clicks. With Versapay, you can also customize which business bank account payments should go to.

5 ways integrated payment processing benefits AR teams

There are multiple benefits to integrating your payment processing with your main accounting system:

1. Automates AR workflows

Without an integrated payment solution, your AR team might depend on multiple third-party systems to process a single transaction. This makes it hard to keep track of important records like bank reconciliation files as you have to pull these from many systems.

Before implementing Versapay’s integrated payment solutions, many of our customers were processing payments over the phone and keying the information into their systems themselves. This is both time-consuming and a security concern.

The AR team at Sharp Electronics’ Canadian headquarters knew this challenge well. Before implementing Versapay, they had over 200 customers making credit card payments over the phone every month.

“My team didn't have enough time to do it, so it took me an entire day every single month to process credit card payments,” says Ellen Chammas, Sharp Canada’s Manager of Credit and Accounts Receivable. “People were calling us for $1 and $2 invoices and we’d spend time on the phone taking their credit card information, leaving us little time for strategic projects.”

An integrated payment solution streamlines not only the cash application process (with payments posting to the appropriate records automatically), but also the invoicing process.

For instance, Versapay’s integrated payment solutions support click-to-pay invoicing. This allows you to automatically email a customer as soon as you create an invoice. Customers receive a secure link to where they can pay one or more invoices online.

2. Allows you to collect payments across any sales channel

Integrated payments are also well-suited to today’s complex and diversifying B2B payment ecosystem.

With customers each wanting to pay in different ways, it's important to be able to accept a variety of payment types across several channels. Integrated payment processing eliminates headaches associated with this by allowing your AR team to accept payments across point of sale, ecommerce, and on account—using just one system.

By supporting a greater variety of payment methods, you can drive more sales. Supporting more payment methods and sales channels also increases your chances of being able to do business with companies that have strict accounts payable (AP) requirements.

3. Helps you save on processing costs

An integrated payment system can also help businesses reduce credit card processing costs. Integrating your payment processing with your ERP allows you to take advantage of a process called interchange optimization.

Interchange fees (paid to the issuing bank by the acquiring bank) make up the biggest part of merchants' credit card processing costs. Merchants can, however, qualify for lower interchange rates by sending additional data about the payment with each transaction.

Your ERP contains rich data about each payment already, like where the product is going and the line-item details of the invoice. An integrated payment processor can send that data along with the payment automatically, thanks to its deep integrations.

The more transaction data you can provide, the more opportunity you have to qualify for lower interchange rates. In interchange optimization, level 1, 2, and 3 data processing refers to the breadth of data sent along with a transaction.

The resulting savings from interchange optimization can be huge. Enough for B2B merchants wary of high processing costs to justify accepting more credit card payments. Versapay, for example, can help you save up to 40% on your credit card processing fees.

4. Defends your business from fraud

Integrated payments are more fraud-resistant, too. And that’s important because 78% of consumers report they would stop engaging with a brand online following a breach.

Chargebacks are one such example of fraud that integrated payments help mitigate. This mechanism that’s intended for consumer protection is often manipulated for criminal purposes, and crops up through:

- Fraudulent activities

- Cardholder disputes

- Authorization issues, and

- Processing errors

Some integrated payment solutions can enable optional e-checkout features that limit fraudulent chargebacks.

Accepting and processing digital payments in sync with your ERP also reduces the need to hand off data to additional parties, helping you further minimize risk.

“There are all these different avenues for fraudsters to get into a business’ ecosystem,” says Chris Wassenaar, Chief Risk Officer at Versapay. “It only takes one organization with that supply chain to not update their security–for their devices or network–for fraudsters to be granted access.”

5. Improves customers’ billing and payment experience

Integrated payments are also a win-win for your customers. With greater support for digital invoicing and payments, integrated payments allow B2B buyers to carry out payments entirely online. Some integrated payment systems also allow buyers to securely store their payment information, which helps simplify recurring payments.

In a survey of 100 finance tech leaders, 87% said their buyers are ready to move away from check payments to digital payments. Integrated payment systems let you get around the challenges that might make accepting and reconciling digital payments challenging, so you can meet your customers where they are.

How to get started with integrated payment solutions

The best thing for getting started with an integrated payment system is to work with a payment processor that integrates seamlessly with your existing ERP system. This allows you to get up and running and start accepting payments quickly.

Some ERP software companies have online marketplaces showing the vendors that already work with their technology ecosystem. Alternatively, ask any potential integrated payment providers if they have API integrations that allow for connection with any system.

Versapay has native integrations with some of the most popular ERP solutions out there—Oracle Netsuite, Microsoft Dynamics 365 (Business Central and F&SCM), and Sage Intacct.

—

Learn how you can reduce manual AR work, speed up collections, and minimize processing fees with Verspay’s integrated payments.

P.S. Looking for advice on how to make your ERP your single source of truth for Finance? Check out our on-demand webinar.

ERP Optimization

Discover every advantage ERP systems offer and how to maximize their capabilities.

Always stay up-to-date

Subscribe

Join the 50,000 accounts receivable professionals already getting our insights, best practices, and stories every month.