Digital Payments: The Bedrock of Modern Business

Secure digital payment solutions are becoming an essential element of the invoice-to-cash cycle in modern commerce, especially in B2B.

Digital Payments Are Ready For The Spotlight

We surveyed 100 finance tech leaders to find out how check and digital payments use compare at their organizations and what their priorities are for the year.

What does the B2B payments landscape look like?

The size of a customer directly impacts the complexity of a payment process. So, B2B payments are naturally more cumbersome and time-consuming than those between businesses and consumers (B2C), largely due to the sheer amount of the transactions and what’s been a slow rate of innovation in B2B payment processes.

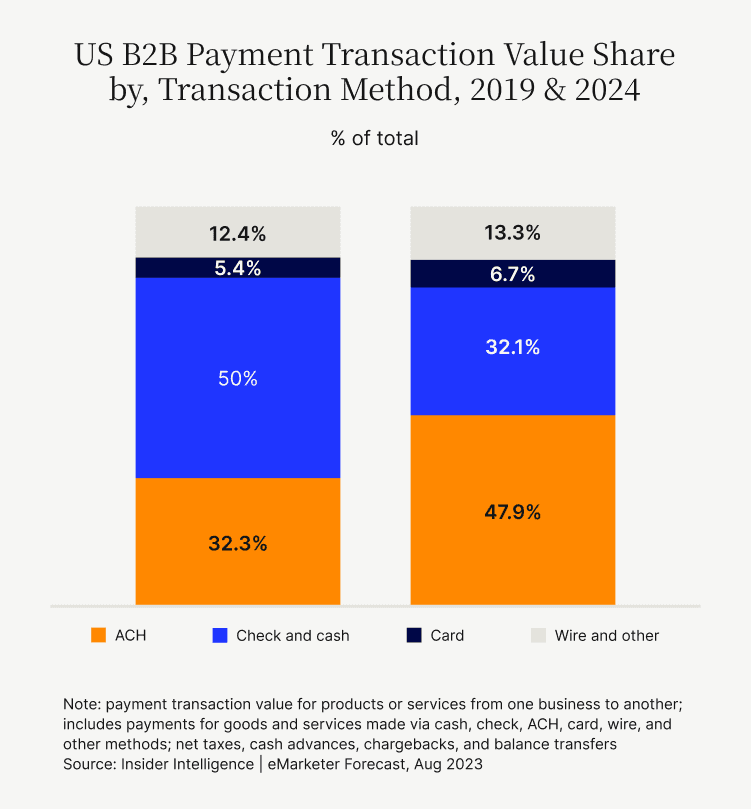

B2B transactions can reach substantial amounts, often in the millions of dollars. Moreover, a significant number of corporations continue to depend on traditional checks. According to eMarketer, recent research shows slightly over 32% of U.S. B2B transactions still involve cash and checks.

Check and cash transactions demand considerable manual processing by the seller. And this can delay the completion of B2B payments by weeks or even—as painful as it is to contemplate—months. To counter these challenges, digital payment solutions make transactions between businesses faster and more efficient.

The financial landscape is undergoing rapid change, with the shift from traditional payment methodologies like physical, check-based transactions to digital payment systems gathering incredible momentum. This is being propelled by the diverse array of benefits that secure digital payment software solutions offer to both B2B sellers and their customers, paving the way for a more efficient, secure, and user-friendly payment experience.

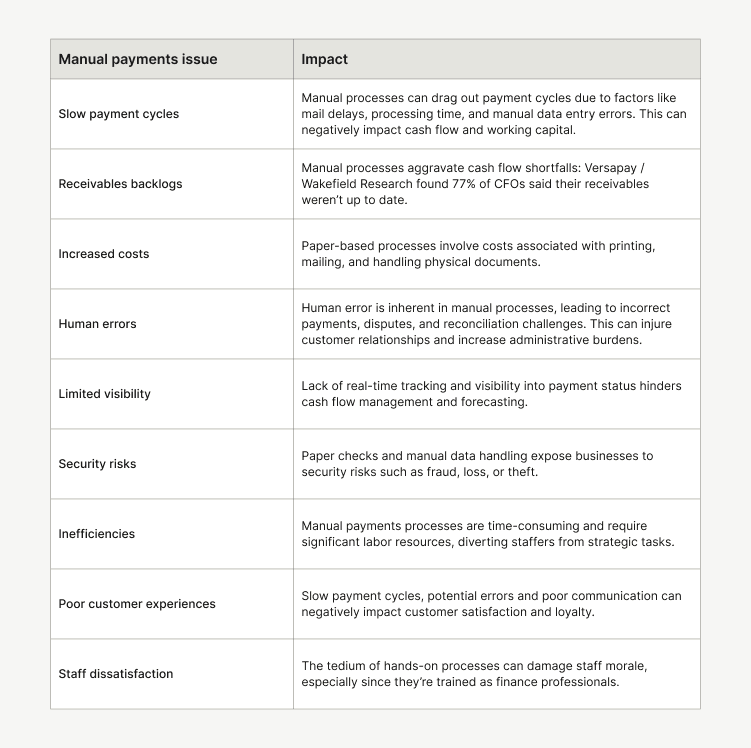

Digital payments vs. traditional payments: Manual process headaches

Traditional payments have dominated B2B commerce since, seemingly forever. These involve transactions based on cash, checks, and bank/wire transfers; the “bill of exchange” arrived as a predecessor to the check during the late Middle Ages, and wire transfers came along when the telegraph went into service.

But all of them come with drawbacks including slower processing times, higher fees for processing checks or wire transfers, increased risk of theft or fraud, and a generally cumbersome experience for both parties—sellers and buyers—involved. Here are just some of the many issues that arise from manual payments processes:

What’s driving adoption of secure digital payment software solutions?

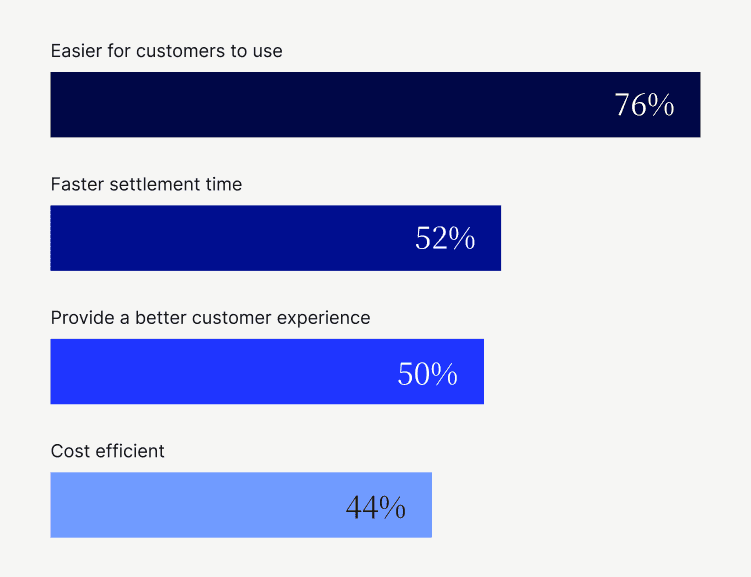

When they consider digital payments vs. traditional payments, companies are increasingly gravitating towards digital payment solutions for several reasons.

Ease of use: Customers can make digital payments that can be made anytime, anywhere, without the physical constraints associated with checks or cash.

Speed: Transactions are processed instantly or within a few hours with digital payment software, as opposed to days for checks to clear.

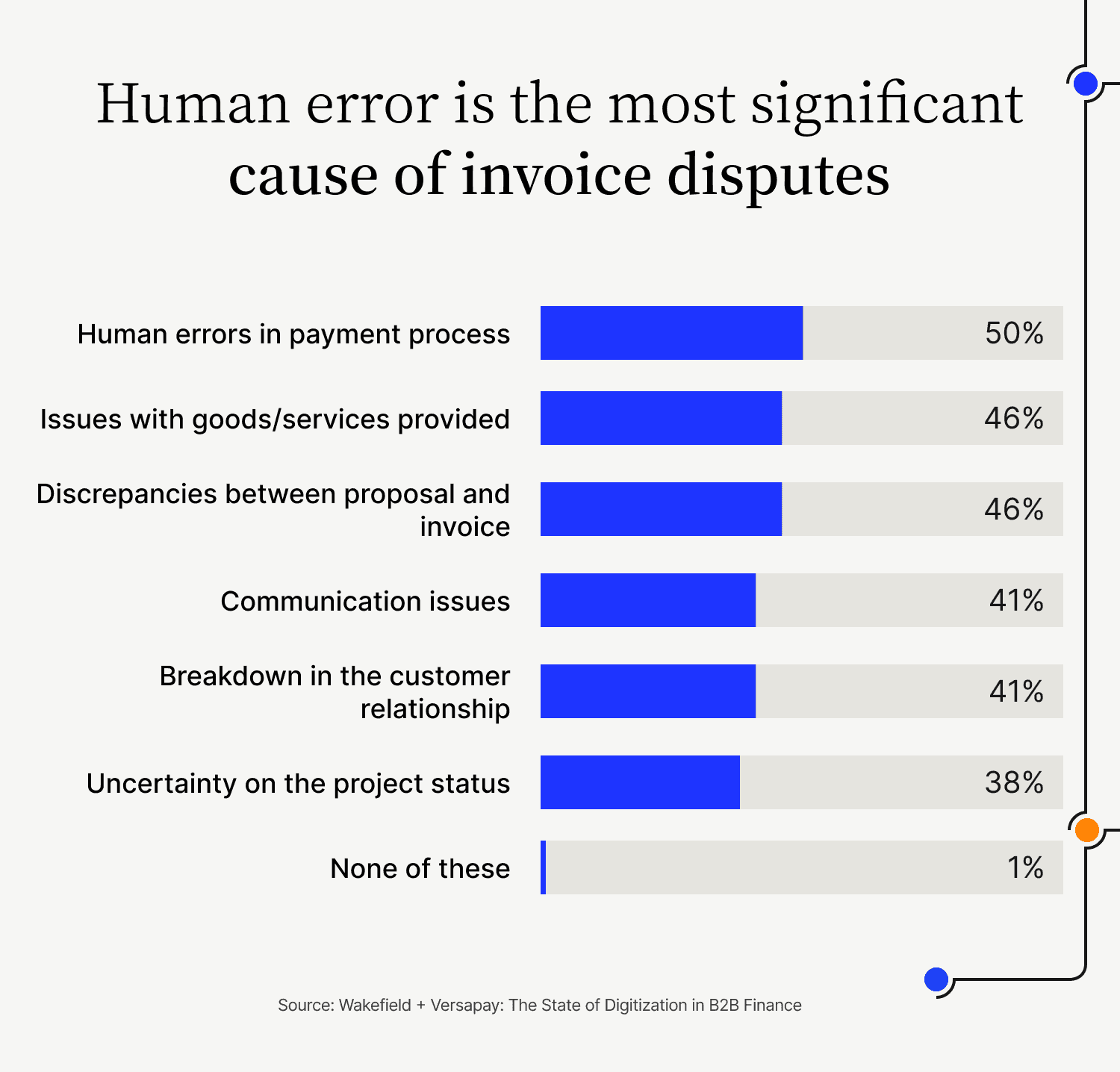

Improved customer experiences: This is thanks to the convenience and accuracy of digital processes, which remove human error and minimize disputes.

Lower costs: Digital transactions often incur lower fees than traditional banking or check processing services, and automating them means far less manual labor is needed.

Why is ease of use so high on the list? Because by offering versatility in payment methods using secure digital payment software solutions, B2B sellers can satisfy what’s increasingly becoming a basic customer expectation: That making a payment should be convenient and easy. Fail to honor their preferences at your own risk!

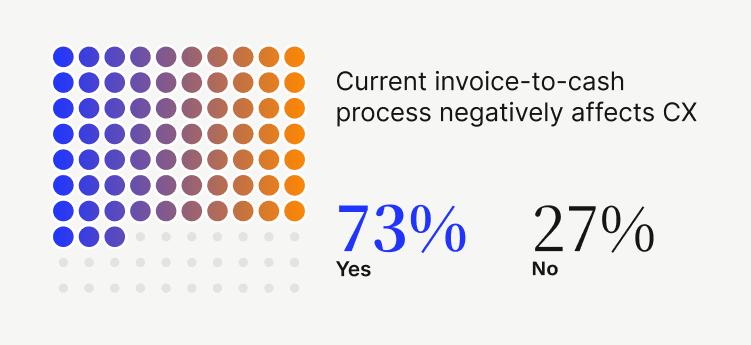

Corporations understand the urgency involved. According to research byJ.P. Morgan and Forbes, 85% of global executives feel optimizing payments is critical to giving their customers satisfactory outcomes.

The State of Digitization in B2B Finance

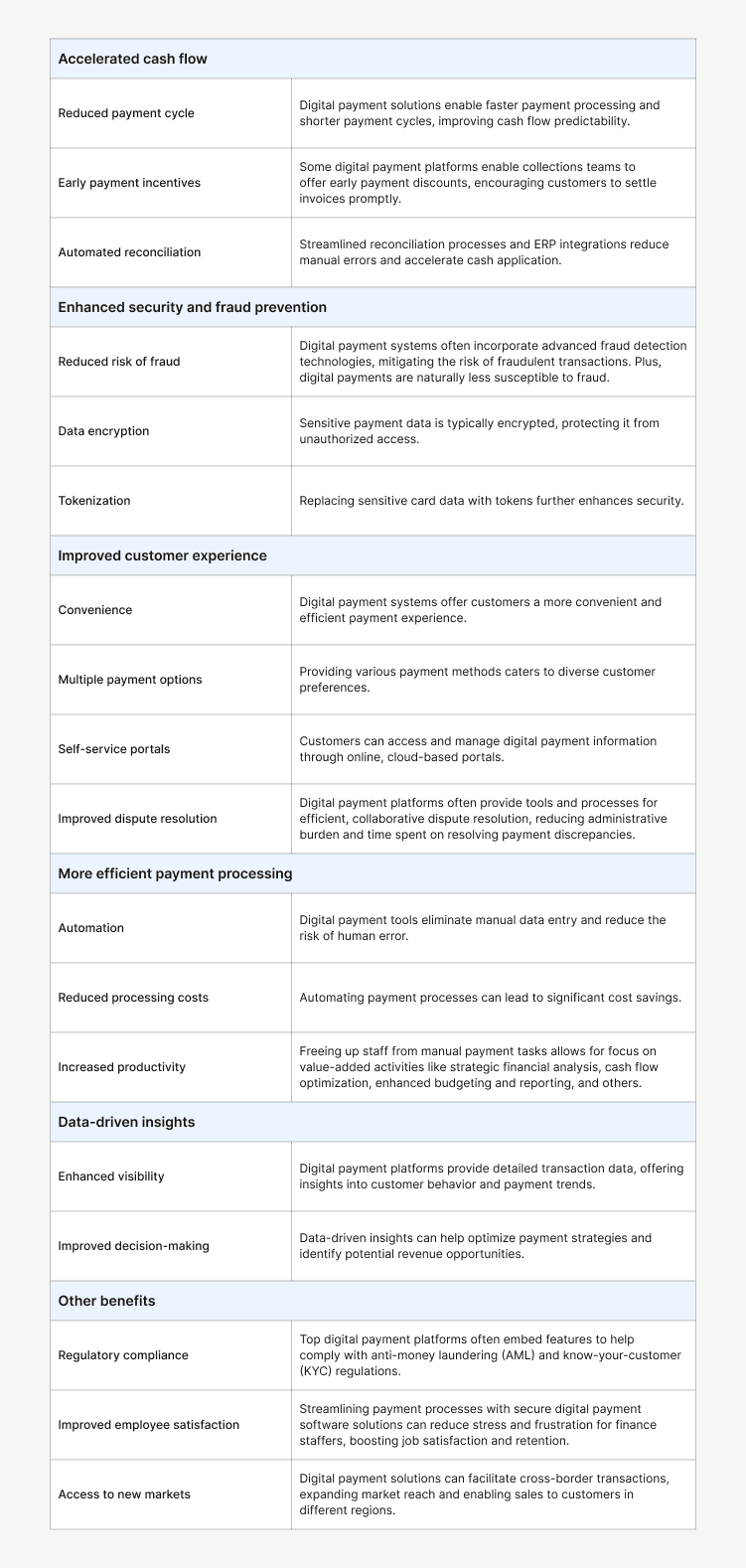

Why switch to digital payments? The benefits for B2B sellers

In comparing digital payments vs. traditional payments, it’s obvious that secure digital payment software solutions offer a myriad of advantages for B2B sellers when it comes to streamlining operations, enhancing cash flow, and improving customer satisfaction. Truth be told, it’s a roster of benefits that traditional payment processes would never be able to deliver.

What is an ACH Payment? The Benefits of ACH Payments and More

10 Ways Digital Payments Reduce Costs, Improve Efficiency, and Build Better Customer Relationships

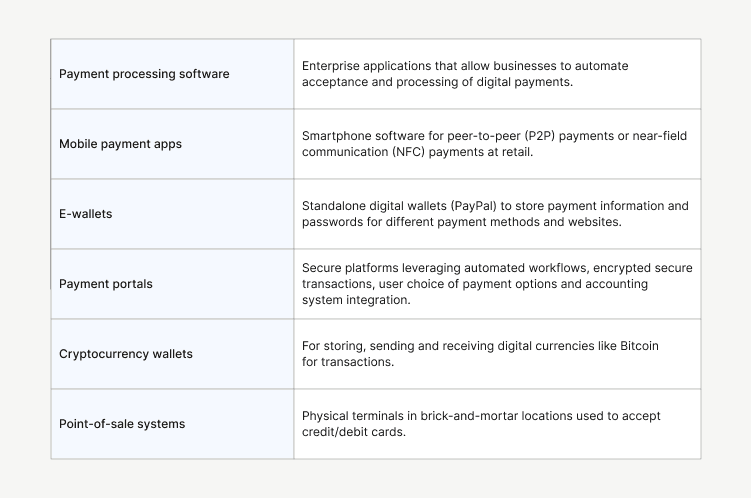

Types of digital payment solutions

Digital payment methods for businesses include a broad range of technologies that offer a stark contrast to traditional payment methods in how they optimize and accelerate the payment process.

Digital payment tools fall into several categories, including but not limited to:

The future of digital payment tools

The trajectory of digital payment systems is irrevocably headed toward even more innovative and secure technologies that will add an extra layer of security and convenience for both sellers and buyers. They’ll offer unprecedented levels of efficiency, security, and personalization in financial transactions.

Here are some of the near-future digital payment methods for businesses that are already impacting the B2B payments landscape:

Virtual credit cards: These enhance security for online purchases by generating temporary card numbers, which protect real account details from cyber threats. This feature has gained popularity among finance leaders, with 55% of CFOs reporting increased usage due to digitization trends.

Real-time payments: These are already gaining ground across the financial industry by allowing immediate fund transfers that reduce payment delays and improve financial fluidity. This has obvious benefits, as it permits quicker access to funds and improves cash flow management. According to PYMNTS.com, 81% of large retailers say real-time payments are very or extremely important for their B2B transactions, with 61% percent of manufacturers and 60% of insurers agreeing.

Blockchain and cryptocurrencies: While still in its early stages, blockchain technology promises unprecedented levels of security, transparency, and efficiency in financial transactions due to its potential to provide a secure, immutable online ledger. Cryptocurrencies, though volatile, could also have a part in enabling frictionless cross-border transactions.

Artificial intelligence (AI) and machine learning: AI-powered tools can enhance fraud prevention, optimize payment routing, and improve customer experiences by extracting insights from huge amounts of transactional data, not just to identify suspect anomalies but to find ways to improve processes. According to Doug Hathaway, Versapay’s VP of Engineering, AI can even make payments and accounts receivable more human, by “... removing much of the legwork needed to apply payments. When this happens it’s [accounts receivable] more engaging, and you can access more data, making it less mundane.”

Embedded finance: Integrating financial services within non-financial platforms (such as e-commerce platforms or ERP systems) enhances user experience and opens new growth opportunities and revenue streams by offering finserv tools directly within their existing platforms.

Request-to-pay: This innovative digital payment tool allows businesses to request payments from customers directly, improving the predictability of cash flow and invigorating business-client relationships by offering greater transparency and responsiveness in transactions.

Biometric, voice and touch payments: Voice-activated payments, facial recognition and touch-based authentication are emerging as secure digital payment tools, promising convenience and improved security by enabling transactions through simple voice commands or touch gestures that use biometric authentication. These cater to modern consumer tastes for quick, intuitive and efficient device and account interactions.

Digital payment systems and technologies that may lie farther into the future include:

Central bank digital currencies (CBDCs): Many governments are, dare we say, getting their geek on and considering roll-out of their very own digital currencies, officiated by the high and mighty central banks. CBDCs might have superheroic potential in B2B by zapping through the old-school barriers to cross-border transactions, giving global commerce a Red Bullish boost.

Quantum computing:It’s just offstage now but it’s getting ready for its turn in the spotlight, when it will probably transform how banking and payment systems work. Quantum systems are hundreds of millions of times faster than “conventional” computers. They could revolutionize fraud detection, accelerate and add intelligence to payment routing, and power cryptographic currencies and payment security tools that’ll create no end of frustration for hackers.

Paper Check Alternatives: How to Transition to Digital Payments

What are B2B Payments: A Guide to Streamlining Payment Acceptance

Learn how B2B payments work, examples of these transactions, the challenges with accepting traditional B2B payments, and the benefits of B2B payment solutions.

Versapay Collaborative AR Delivered 305% ROI

Demonstrating positive returns is key to successful digital transformations—especially as budgets tighten.

Digital Payment Fraud Prevention

Learn what digital payment fraud is, effective strategies to prevent online payment fraud, and how to provide customers a secure payment processing experience.

Why B2B Payment Automation is a Top Priority for CFOs

What is an eCheck? Your Guide to Understanding How Electronic Checks Work

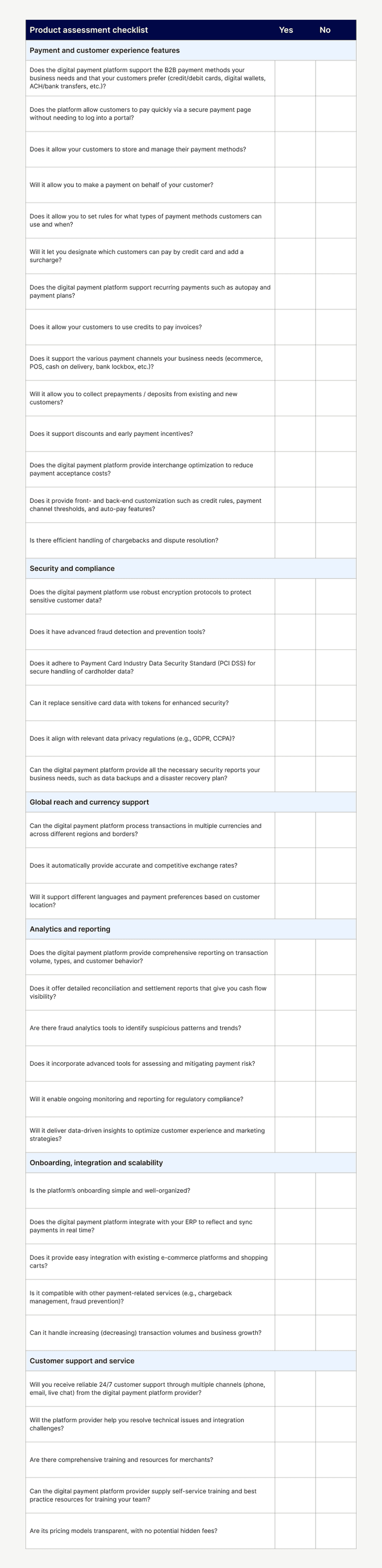

Choosing the right digital payment solution provider

Why switch to digital payments? Because the upside is outstanding. But choosing the product that’s best for your business from among competing secure digital payment software solutions is mission-critical if you’re aiming to provide seamless and secure B2B transactions.

Here are the key features you should look for in a digital payment system and its provider that can make that happen without headaches—or buyer’s remorse.

By getting answers to these questions, your organization can pick a digital payment platform that actually aligns with your specific needs, enhances customer experience, and mitigates risk.

How to Choose Accounts Receivable Automation Software

All digital payments resources

Getting paid online means you'll get paid faster. Find answers to questions on topics like virtual cards, what payment methods are used in B2B transactions, and much more.

How to Choose Accounts Receivable Automation Software

Learn what value there is in automating your accounts receivable and how to choose accounts receivable automation software

The State of Digitization in B2B Finance

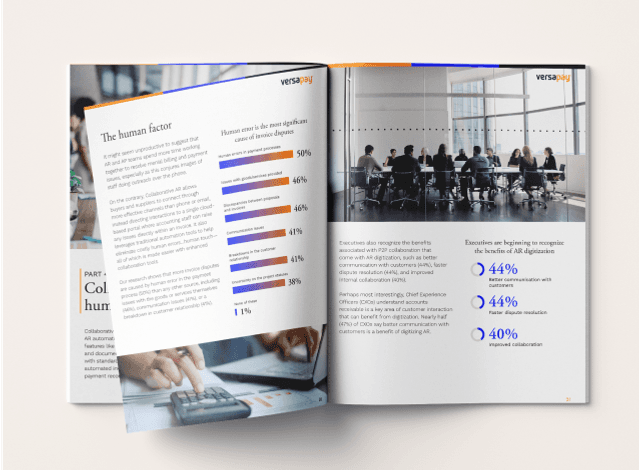

In collaboration with Wakefield Research, Versapay surveyed 1,000 C-level executives at companies with a minimum annual revenue of $100m USD on their AR digital transformation efforts.

Digital Payments Are Ready For The Spotlight

Versapay surveyed 100 finance tech leaders to find out how check and digital payments use compare at their organizations and what their priorities are for the year