Digital Payment Fraud Prevention

Learn what digital payment fraud is, effective strategies to prevent online payment fraud, and how to provide customers a secure payment processing experience.

How to Fight Fraud and Maximize CX

Payment fraud is ever evolving. Make sure you can process payments with peace of mind.

This guide explores:

→ The different types of payment fraud

→ How it can be detected and prevented

→ How to process payments while maximizing CX

→ And more

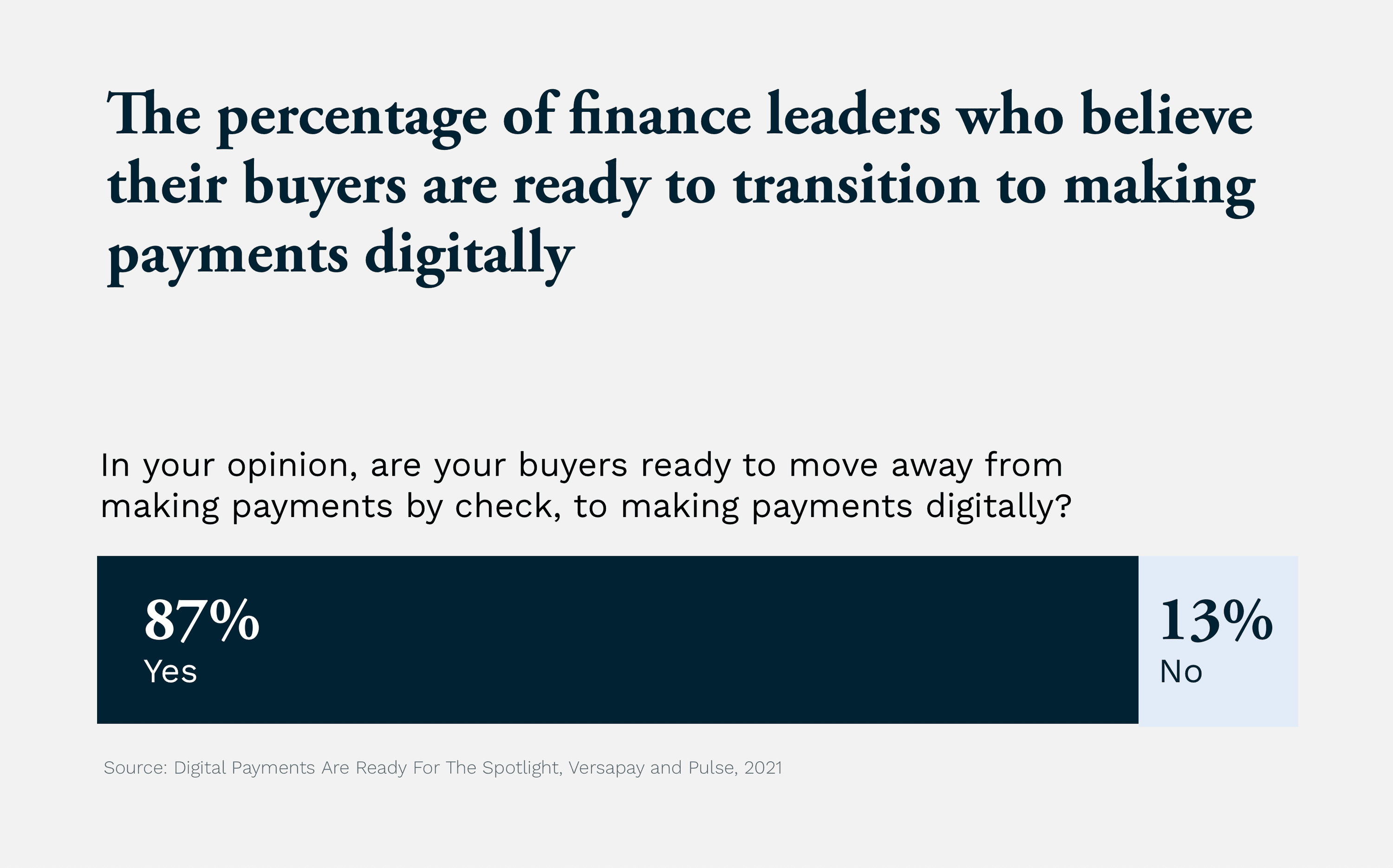

Eighty-seven percent of finance leaders believe their buyers are ready to transition to making payments digitally. With more business-to-business (B2B) customers embracing online payment channels, it’s important that finance leaders be aware of the risks of digital payment fraud and are well-equipped to combat them.

This is because payment fraud is ever evolving.

The threats that businesses and consumers now face are much different from the threats that prevailed at the turn of the 21st century—when check usage dominated and “online payment fraud” was still a foreign concept to many.

The different types of payment fraud

Payment fraud is multi-faceted.

New breeds of fraudsters are continually emerging, with new types of attacks surfacing whenever one is stamped out. The challenge for businesses is being aware of these emerging forms of fraud and how to spot them. With the right technology, businesses can more readily implement effective strategies to prevent online payment fraud, detect and lessen its impact on revenue and operations, and simultaneously enhance the customer experience.

We’ve elected to break down payment fraud into two groups: check fraud and digital payment fraud.

Digital payments have long been ready for the spotlight, but 91% of finance tech leaders say their organizations are still receiving check payments from their customers. Digital payments are the future of B2B commerce—there's no denying it—but for now, checks are still prevalent. Although, if the customer experience and back-office accounting benefits of accepting digital payments weren’t enough to turn you away from checks, maybe the payment fraud risks will.

“There are all these different, wonderful avenues for fraudsters to get into a business’ ecosystem. It only takes one organization with that supply chain to not update their security—for their devices or network—and that grants fraudsters access” — Chris Wassenaar, Chief Risk Officer, Versapay

Payment fraud group: Check fraud

What is the definition of check fraud?

We know that payment fraud occurs when an individual deliberately extracts money from another individual or business entity through deceptive and criminal means. Check fraud is simply the process of using checks to commit payment fraud.

What are the different types of check fraud?

Check fraud comes in many different shapes and sizes. What’s important to note, however, is that when dealing with physical checks, there are two critical vulnerabilities that aren’t present for their digital payment method counterparts.

Check payment fraud vulnerability 1—The first vulnerability is checks’ actual physical, paper-based nature. Because checks have to be physically transported from one party to another, there’s a higher likelihood that a fraudster can obtain checks while in transit or elsewhere.

Check payment fraud vulnerability 2—The second vulnerability is the confidential information contained within checks. In having information like your name, address, account number, and routing number directly on a check, you’re providing fraudsters upfront with all the information they need to commit check fraud.

The primary types of check fraud include:

Check forgery—This method is typically used when defrauding banks. The fraudster will intentionally sign a check without authorization or will endorse a check that’s not payable to the endorser. In very rare cases, a fraudster will try to pass a check that’s manufactured by themselves that represents an account that is not real.

Paper hanging—Paper hanging occurs when a fraudster knowingly writes a bad check. In this case the fraudster might purposely write a check that exceeds their balance to overdraw their account and take advantage of the float time. This is sometimes called check abandonment.

Check theft—This is the physical theft of checks with the intent to cash them fraudulently. The fraudster then typically forges a signature.

Check washing—This method often follows closely on the heels of check theft. Fraudsters will use highly volatile solvents to erase the ink off checks and then rewrite the checks as payable to themselves. They will likely increase the payable amount by hundreds or thousands of dollars.

Counterfeiting—A counterfeit check is printed on non-bank administered paper and made to look genuine. The information the fraudster includes on the check, however, will be tied to a real victim’s account.

Check kiting—Similar to paper hanging, check kiting is reliant on check float, whereby fraudsters aim to delay the notice of non-existent funds. In essence, fraudsters will gain access to funds deposited in one account prior to the bank collecting them from another.

Check conversion—In the context of check fraud, check conversion takes place when a non-payee endorses a check and then deposits it fraudulently. That same non-payee will take possession of cash that does not belong to them, and the true recipient will be unaware until much later.

The takeaway: relying on check payments isn’t great payment fraud management.

Payment fraud group: Digital payment fraud

What is the definition of digital payment fraud?

With the payment landscape evolving quickly, more digital payment channels are becoming available. Even payment methods traditionally popular within the B2C realm are becoming increasingly prevalent in B2B circles.

With this comes increased vulnerability to payment fraud, as each new payment method creates a new opportunity for fraudsters. According to the CEO of fraud detection company DataVisor, the advent of card-not-present (CNP) transactions replacing checks has seen fraudulent activity across digital channels ramp up significantly.

Compounding matters further is the fact that many businesses are unable to keep up with the rate of change or lack the in-house expertise to confidently fight fraud. This makes payment fraud management—and payment fraud prevention and detection—increasingly difficult.

At its core, digital payment fraud is no different than check fraud—fraud is fraud, after all. The difference lies in the tactics used by fraudsters and the need for businesses to remain highly vigilant as digital payment trends evolve.

What are the different types of digital payment fraud?

There are many more types of internet frauds—which are often intertwined with payment fraud—than these, but here are some of the most common types that merchants should be on the lookout for:

Identity theft—The scheme is as old as commerce itself, but, like commerce, has evolved over time to remain a threat. In this modern, digital age, fraudsters might impersonate e-commerce websites and attempt to obtain personal data via corrupted shopping carts.

Card theft—This method makes use of fraudsters’ theft of credit—or other card—details to then make purchases online. Businesses will often assume the purchase was legitimate and successfully process the transaction. The cardholder will likely dispute the transaction once they’re made aware, however, the business will be unable to recoup their losses (the cost of goods and services provided and the dispute fees).

Chargebacks—This process—whereby a cardholder disputes a charge with their bank—is an important consumer protection mechanism. It’s also a process that’s often abused by fraudsters in B2B commerce. Fraudsters deploy tactics such as account takeovers, phishing and smishing, domain squatting, and identity theft to make fraudulent purchases resulting in chargebacks.

Overpayments—In this case, a fraudster will make a purchase using illegally obtained credit card credentials and then approach the supplier for a full or partial refund. The fraudster, however, will request that the refund be granted to a different credit card than the one initially used or request payment through other means. If a chargeback is filed, the supplier will be left hanging for the chargeback amount and the amount sent to the fraudster.

Credit card testing—This is a malicious attack—facilitated by a fraudster—on a merchant’s website or shopping cart. It’s usually triggered by a bot or automated script that tests lists of illegally obtained credit card information to identify valid cards. The merchant may incur significant fees from credit card testing, whether the transactions are successful or not.

Account fraud—This kind of fraud occurs when fraudsters create customer accounts using falsified or stolen identities, or gain access to existing, legitimate accounts by masquerading as a colleague and subsequently changing email and mailing addresses. After acquiring access, fraudsters can steal funds directly using fraudulent wire transfers and purchases.

“A fraud prevention and detection strategy is important for all businesses because fraudsters will always focus on the weakest link or most vulnerable target to attack. For example, when EMV chip technology was introduced, fraud did not go away, it simply shifted from in-person fraud to card-not-present fraud and electronic payment systems became the new target. As more businesses adopt digital payments, the incentive for fraudsters to exploit vulnerable systems also increases. It's important that all businesses accepting digital payments deploy a fraud mitigation strategy that includes automated tools to verify the identity of a customer and provide real-time fraud scoring to properly evaluate the risk of a transaction” — Chris Adams, VP of Product, Payments, Versapay

The Ultimate Guide to Credit Card Processing

The most (and least) secure payment methods

While the potential for digital payment fraud might dissuade some businesses from making the jump to online payments, there are plenty of reasons not to let payment fraud be a deterrent. We’d argue that now, more so than ever, is the best time to embrace digital payments.

Here is a list of the most—and the least—secure payment methods to avoid online fraud. Notice anything? (Hint, hint. The most secure are all digital payment methods).

The most secure payment methods

1. ACH

An ACH is an electronic transfer of funds system run by the National Automated Clearing House Association (NACHA) in the United States. With an ACH payment, funds are moved electronically from one bank to another through the ACH network. This network connects every single US financial institution, which gives them the ability to transfer money from one bank to another safely, quickly, and securely.

2. Virtual cards

Virtual cards are single-use credit card numbers that are generated for each payment. As the name suggests, they are entirely virtual—no plastic, no chips, no PINs. Buyers typically enjoy using virtual cards as they offer improved security, better control, and complete transaction details.

Sellers are increasingly embracing this payment method, with help from solutions that allow for straight-through-processing of virtual cards, integrated with their enterprise resource planning systems (ERPs).

💡 Did you know that 63.5% of finance leaders report losing revenue because they’re unable to accept virtual credit cards? Learn more about the value of virtual credit cards in: The State of Virtual Credit Card Adoption Among Finance Leaders 💡

3. Credit cards

Despite how rampant payment fraud has become—and despite credit cards seemingly being the crux of all fraudulent attacks and types of payment frauds—credit cards are still one of the three most secure payment methods, especially for B2B buyers. Credit cards offer the benefit of not being linked to the buyer’s actual bank account and the ability to lock the card at the sign of fraudulent activity.

🚨 Our Ultimate Guide to Credit Card Processing covers what you need to know to secure and protect sensitive credit card data from credit card processing fraud 🚨

The least secure payment methods

1. Paper checks

Familiarity and a false sense of security are driving check payment fraud. It’s time to put those falsehoods to rest. Paper checks contain a wealth of sensitive information that can lead to severe consequences when in fraudsters’ hands.

Consider eChecks as an alternative to paper checks. This payment method is cheaper to process than paper checks—and credit cards—faster to process, less susceptible to transaction fraud, and creates less manual accounts receivable work,

2. Wire transfers

The term wire transfer is often used interchangeably with ACH. But while the two work very similarly, there are some notable differences that make wire transfers less secure and more open to payment processing fraud.

Note that wire transfers can be used to send several million dollars whereas ACH (Same Day) caps at $100,000 per payment. Once settled, wire transfers are also very difficult to reverse.

3. Phone-initiated payments (card-not-present)

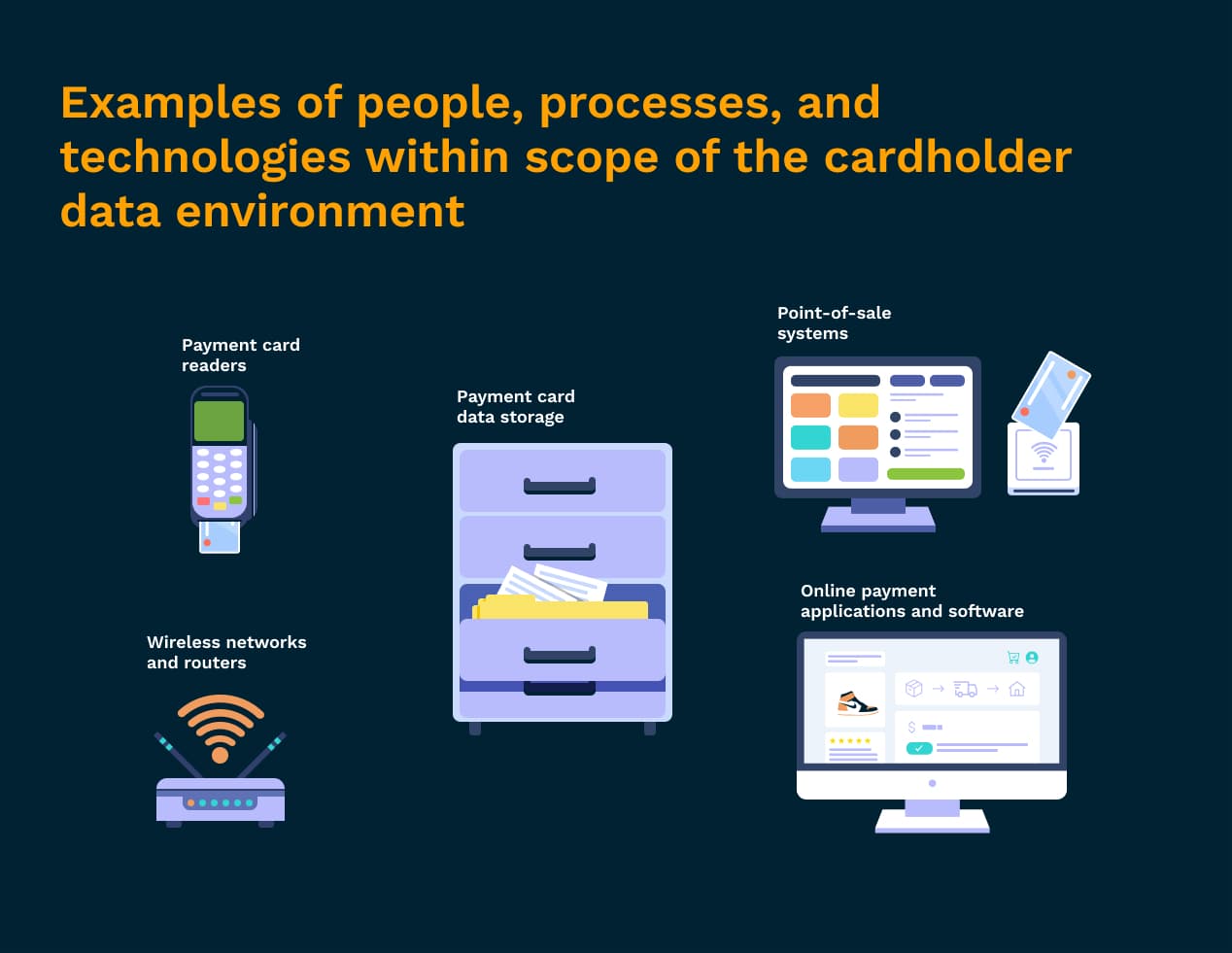

Phone-initiated payments put B2B sellers firmly in PCI DSS scope and the actual effort of processing payments over the phone is sluggish, inefficient, and error-prone.

Credit card information relayed over the phone must be handled by someone to process it, which opens your business up to risk. You’ll also need to ensure that information is destroyed—if it was recorded on a piece of paper for instance—after it’s been appropriately inputted into your accounting systems.

The Most (and Least) Secure B2B Payment Methods

How to Leverage Payment Fraud Detection Capabilities to Boost CX

Payment fraud protection: How to detect payment fraud

With how fast payment fraud evolves, it can be difficult for businesses to be as educated—and prepared—as possible to fight it.

That’s why having effective strategies to prevent online payment fraud in place is so vital for businesses. Rather than be reactive, it's important businesses take a proactive stance and identify suspicious behavior and patterns, in as close to real-time as possible.

Learn to spot what payment fraud looks like

It’s one thing to be familiar with the kinds of check and digital payment fraud we mentioned earlier. To actively detect whether a fraudulent scheme is at play, you’ll want to be on the lookout for a few telling indicators. Here are some of the most common signs of payment fraud:

1. Falsified or inconsistent information

Be on the lookout for buyers transacting using false information—such as phone numbers and email addresses. In many cases the information might appear to be accurate, but if there are inconsistencies—such as the same email address but different names used across multiple purchases—that’s a red flag.

2. Abnormal or canned communications

Fraudsters look to target as many businesses as they can in as little time as possible. To expedite the process, they often use canned or scripted responses. If communication with a prospective customer seems stiff or off or abnormal in any way, it might signal the start of a fraudulent attack.

3. Unusually large orders

You likely have a general sense of what products sell when, and in what quantities. Be aware if you suddenly begin receiving unusually large orders (comprised of multiple high-value goods) and are unable to pinpoint to a reasonable cause.

4. Atypical requests

Identifying fraud unfortunately requires a fair amount of qualitative analysis. Listening to your gut feeling is important. If you notice some unusual requests are being made, this could be a sign of fraudulent activity. For example, you might receive requests to:

Split a large order into multiple payments across different cards with different billing addresses

Process a payment manually to overcharge a card and pay the difference to a third-party, or

Provide a refund outside the card network from which the charge originated—such as via check or ACH

These might all be indicators of fraudulent behavior.

Recognize illegitimate traffic and behavioral changes easily

Once you know what you're looking for, you can create velocity logic rulesets—if you have an e-commerce or online shopping portal—to monitor data elements that occur within specific intervals. This means setting parameters that look for the above-mentioned indicators to help reduce incoming fraudulent activity.

It’s important you appoint a specific contact or team within your organization to receive notifications for these parameters. They should be someone who can be counted on to move into action when any of your controls are exceeded or triggered. This will allow you to quickly act and stop any incoming fraudulent activity as soon as It's identified.

“Awareness of customer payment frequencies and behavioral patterns is imperative at detecting where vulnerabilities exist” — Brandy Luczywo, Interchange Analyst, Versapay

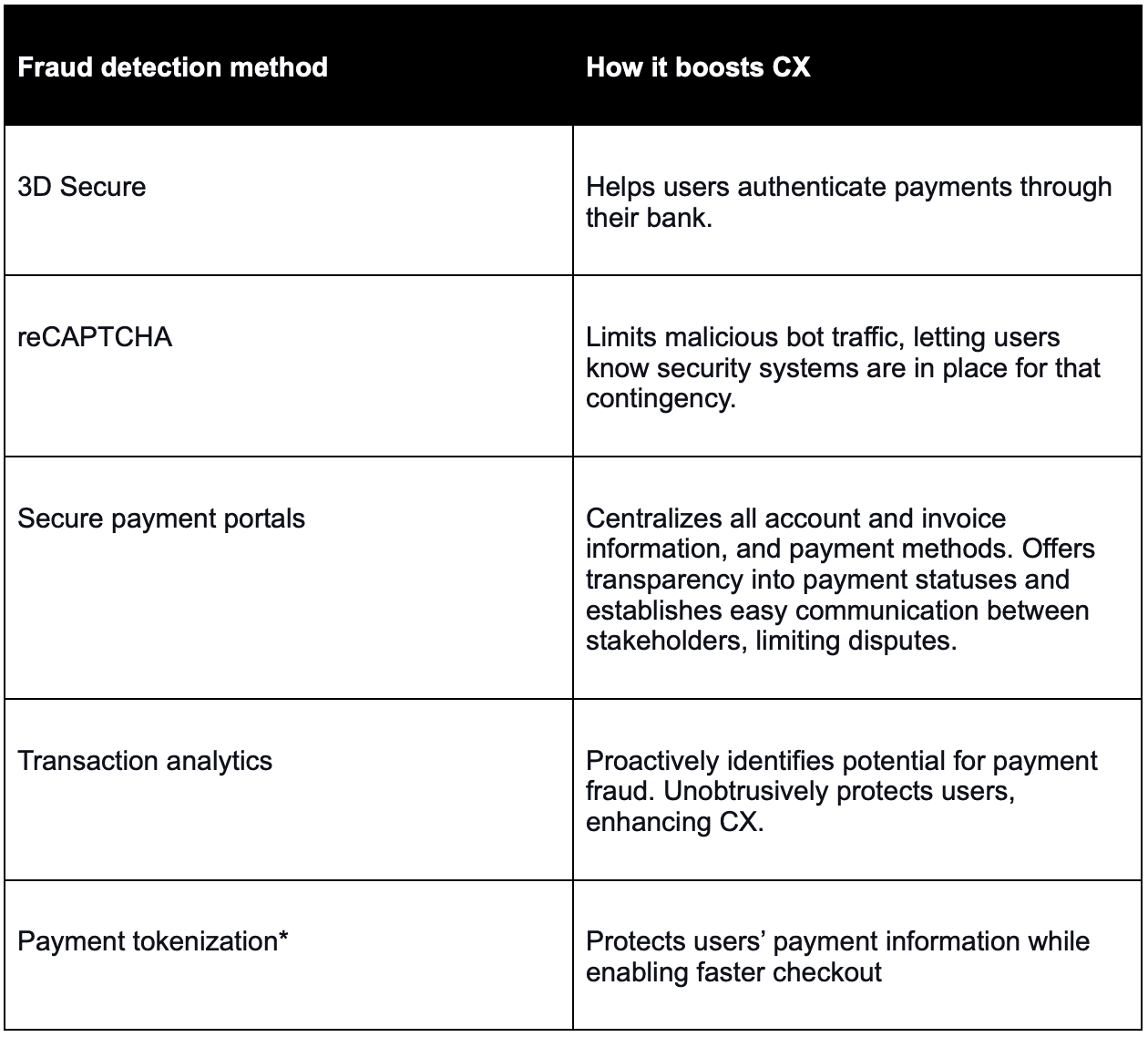

Implement payment fraud detection methods (that simultaneously improve CX)

Given the ramifications of payment fraud—or of being the recipient of fraudulent activity—businesses tend to treat payment fraud prevention as an exercise in risk management.

Unfortunately, this often impedes customer experience. It’s important you blend your payment fraud prevention tactics into your payment acceptance and processing workflows seamlessly, so that your customers’ payments are secure and their payment experience as a whole is enjoyable and memorable—for the right reasons; not for the unnecessary friction that’s often imposed on them.

Payment fraud prevention tactics can actually improve customer experience while minimizing payment fraud risk—here’s a sampling of how:

The Growing Need for CFO and CIO Collaboration

How to Accept Secure B2B Payments Online (While Limiting Fraud Risks)

Payment fraud protection: How to prevent payment fraud

A key realization for all B2B focused businesses is that it’s impossible to eliminate all fraud. But, that doesn’t mean it’s impossible to mitigate and prevent it from severely damaging your business’ financials and reputation. It just means you need to be highly vigilant and understand the inherent risks of accepting payment.

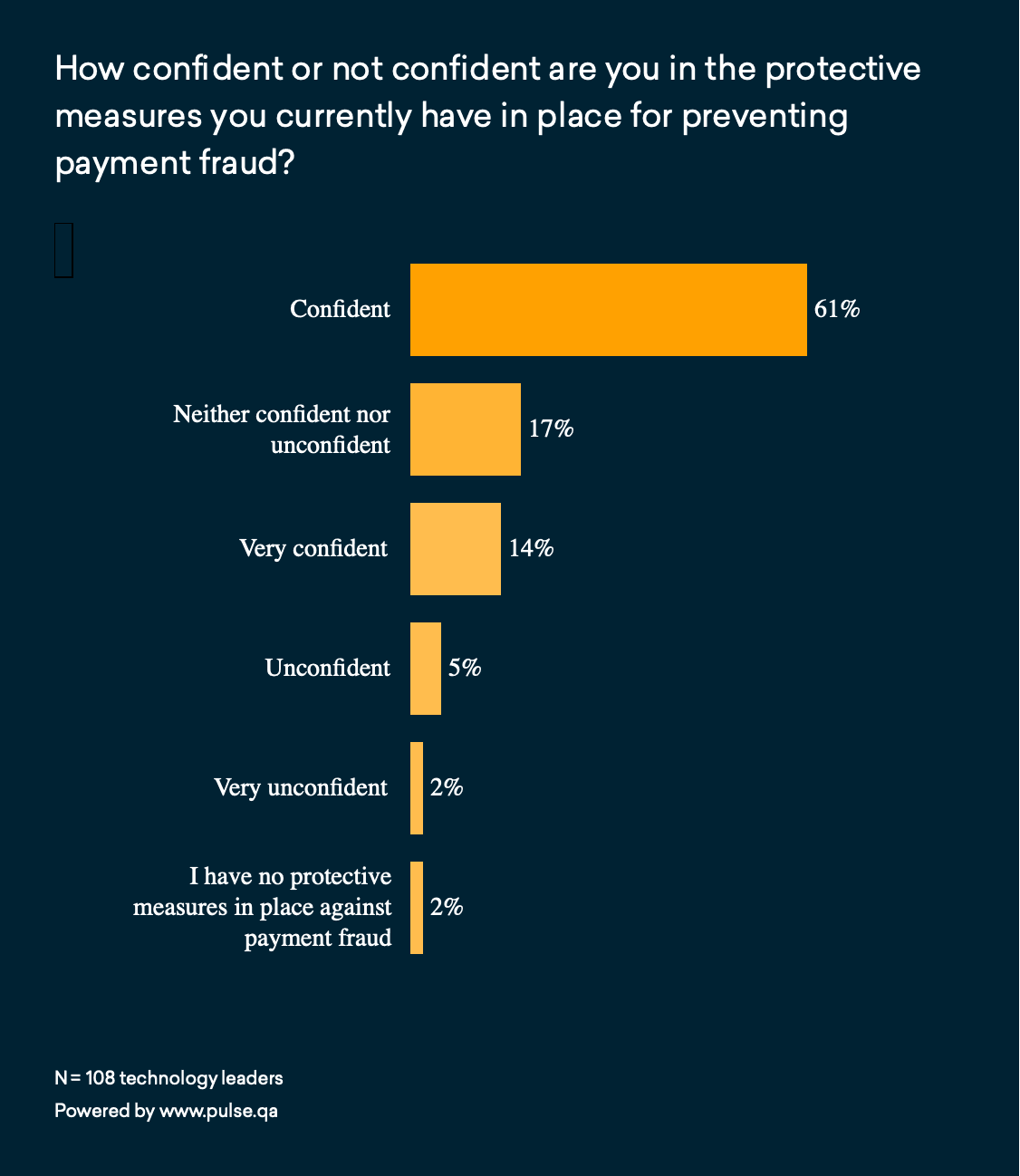

A recent survey by Versapay and Pulse revealed that 26% of technology leaders lack confidence in the protective measures they currently have in place for preventing payment fraud. Nearly three quarters of respondents, however, are confident or very confident in the measures they’ve implemented.

While these are promising surface-level findings, confidence does not equal security. Businesses are being impacted by payment fraud to the tune of nearly $30 billion a year. The most important thing you can do to maintain vigilance in the fight against fraud is to continually evaluate your position.

There are further payment fraud protection and best practices for online payment fraud prevention—and anti-fraud controls businesses can action—including:

Monitor, prevent, and block incoming fraudulent activity

Make compliance a year-round priority

Align your finance and IT divisions

1. Monitor, prevent, and block incoming fraudulent activity

One of the most important things you can do to prevent payment fraud is establish processes and tools that enable you to stop fraudulent activity early—not just merely detect it. With digital payments—specifically credit cards—the critical window to mitigate fraudulent activity is before authorization occurs—here, fees are still incurred even if a transaction is not approved.

One such tool that can help mitigate fraud is the use of CAPTCHAs. These are systems that help web hosts understand if humans or robots are accessing a website. They are unobtrusive safeguards that protect websites from spam and abuse. A common practice among fraudsters is card testing, which involves using automated scripts to run high volumes of authorization tests on illegally obtained credit cards. CAPTCHAs can block these mass tests.

“A little bit of friction—like having to engage a CAPTCHA—tells buyers that merchants actually care about the security of their credit card data” — Chris Wassenaar, Chief Risk Officer, Versapay

“Fraudsters are creatively identifying and capitalizing on vulnerabilities within shopping carts and API-related connections so having CAPTCHA-related functionality as well as monitoring and ensuring appropriate PCI compliance with all forms of payment-related processing connectors is strongly encouraged” — Brandy Luczywo, Interchange Analyst, Versapay

2. Make compliance a year-round priority

While adhering to PCI compliance guidelines is necessary for businesses that handle credit card information, being PCI-compliant does not guarantee your business will not fall victim to a data breach or payment fraud.

There is, however, a noticeable trend of businesses being non-compliant at the time of experiencing a data breach. According to Verizon’s 2020 Payment Security Report, of the companies that experienced a breach between 2014 and 2019, 53% were confirmed to be non-compliant. A remarkable 0% of PCI compliant companies surveyed experienced a breach. It’s important to view PCI compliance as a continuous effort that goes beyond the time of your annual certification.

3. Align your finance and IT divisions

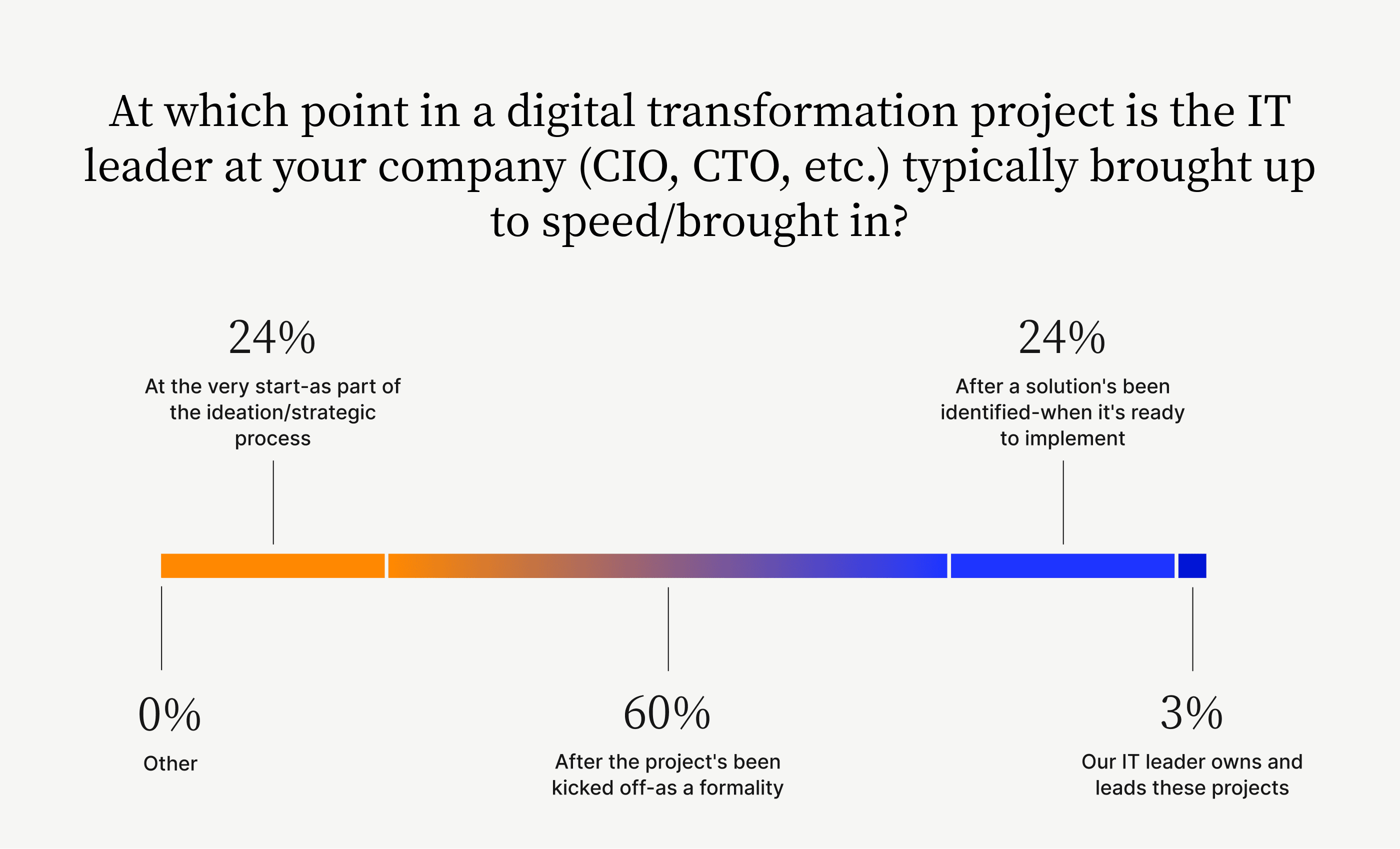

Efficient collaboration between your finance and IT teams is critical to preventing payment fraud—and boosting payment security. Unfortunately, there’s a tangible disconnect between the two parties, reducing how payment security is prioritized at most organizations.

We set out to examine the extent of this disconnect, and what we found is significant. In surveying 500 finance and IT leaders—to better understand their perception of how important collaboration between the CFO and CIO is—we learned that 60% of respondents only bring their IT leader up to speed on transformation projects after the project's been kicked off (and then, only as a formality).

This lack of collaboration has serious consequences for payment security. For example, the disconnect leads to IT being unaware of broader business goals and finance being unaware of the digital risks the company might face. As a result, payment applications go live with significant flaws, posing potential payment fraud—and customer experience—risks.

💡 Read our article—How to Boost Payment Security with Finance and IT Alignment: Why Collaboration is Critical—to learn best practices for aligning finance and IT to improve payment security and reduce the risk of payment fraud 💡

How to Boost Payment Security with Finance and IT Alignment: Why Collaboration is Critical

Prevent payment processing fraud: Process payments securely with Versapay

Beyond practicing constant vigilance, the most surefire strategy for mitigating digital payment fraud and processing payments securely is to streamline your payment acceptance. And the best digital payment processing and online payment fraud detection and prevention solutions are integrated payments solutions that allow you to process digital payments directly inside your ERP:

Partner with a secure, integrated payments provider

Many third-party providers—payment processors, payment gateways, merchant acquirers, issuing banks, and ERPs—are involved in processing digital payments. The more hands a payment passes through, the more vulnerabilities exist. And any vulnerability is an access point that fraudsters can exploit.

One of the best ways to increase the security of your digital payment acceptance is by using an integrated payments solution embedded seamlessly with your ERP. This eliminates many of the vulnerabilities arising from having multiple handoffs between third-party providers. These integrated payments solutions also allow buyers to securely store their payment information, simplifying repeat purchases.

Fraudsters will use what’s publicly accessible, such as an e-commerce site or a non-gated web-based payment page, to carry out their schemes. Instances of fraud on integrated payments solutions are exceptionally low as buyers typically pay through secure portals that require logins.

“The digital payment ecosystem is fragmented. Whether it's B2C or B2B, businesses are engaging with multiple third-party service providers and weaving their solutions into their own internal information technology infrastructure. Understanding the full landscape of that ecosystem is critical for businesses looking to prevent payment fraud” — Chris Wassenaar, Chief Risk Officer, Versapay

Secure payment solutions embedded directly in your ERP

Versapay offers native integrations with…

… to help you securely accept digital payments directly within your ERP. Using our secure payment gateway for fraud prevention, integrations with popular shopping cards, and first-rate merchant services, we safely transport sensitive card data from external systems directly to your ERP.

And where we don’t already have native integrations, we work with you to develop a solution tailored to your system.

Accepting and processing digital payments within a unified ecosystem that you control will significantly reduce the need to handoff data to additional parties, helping you minimize risk.

Versapay does more than help merchants process payments within a secure environment:

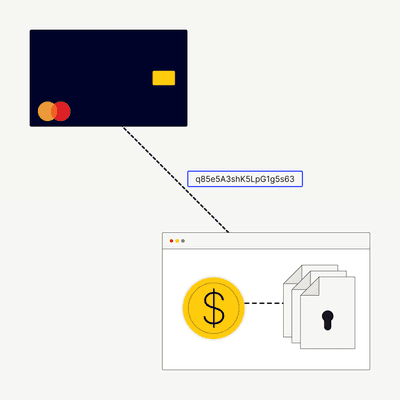

We remove you from PCI DSS scope by tokenizing and ensuring sensitive card information totally bypasses your e-commerce site. You can operate your e-commerce site with peace of mind, knowing sensitive data will never touch your servers.

We enable you to accept the most secure digital payment methods.

We provide you with greater visibility into your payments data, helping you learn expected payment behavior and understand when anomalies occur.

“This has been the most responsive payment processing partner I have ever worked with. Versapay took the time to understand our business and ensure we reduced our payment processing costs and improved funding timeframes. They have been a true advocate when it comes to fighting chargebacks” — Nicholas Cordaro, President, Las Vegas Expo

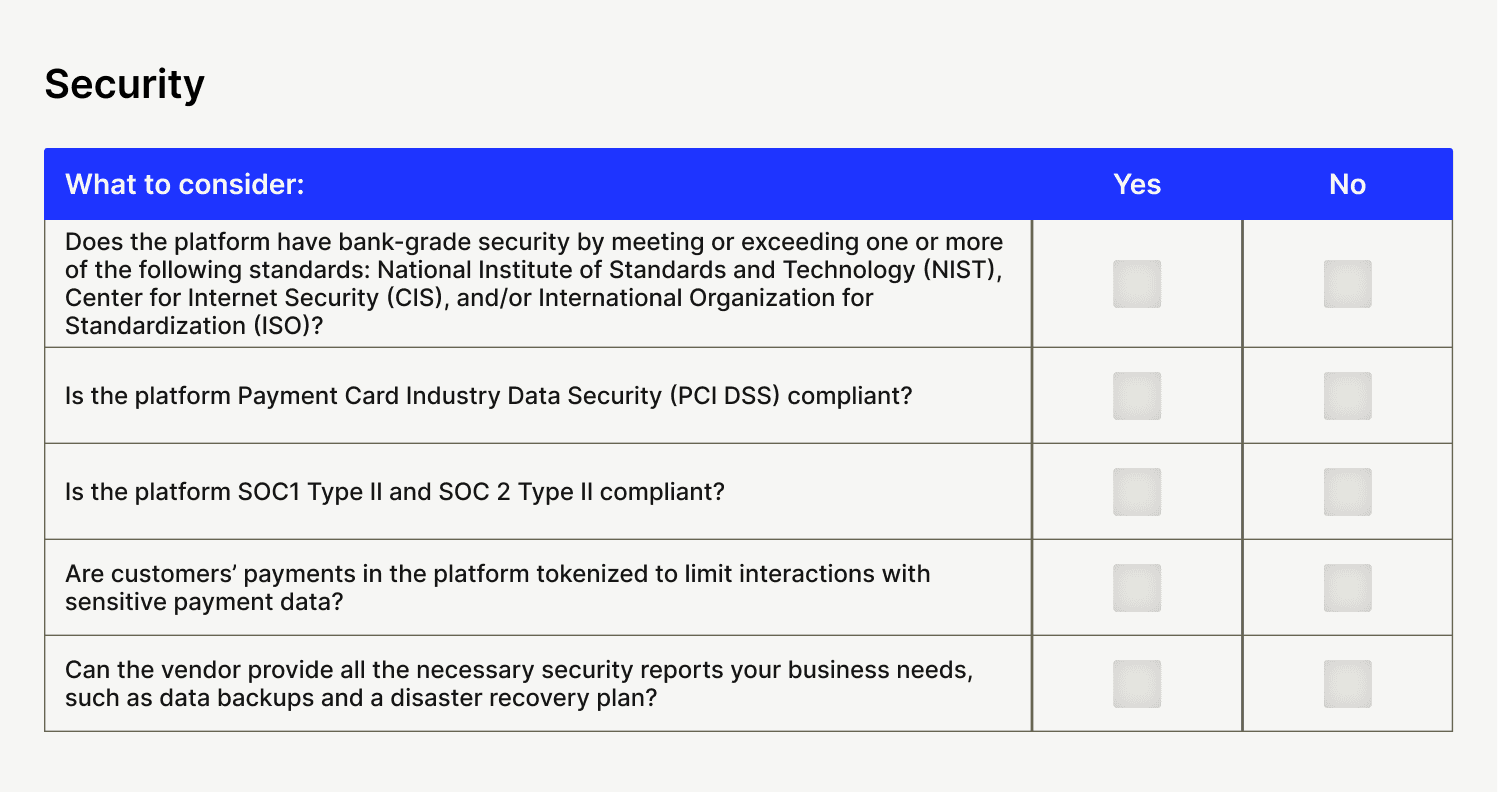

How to evaluate payment processing software

So, you want to find payment processing software with payment processing fraud prevention functionality baked into it—great idea! When choosing a processing and fraud detection system for e-commerce (or phone, POS / card-not-present) it’s important you’re able to capture any payment, from any channel, as securely as possible.

Here’s some criteria—from a payments and a security standpoint—we recommend evaluating potential payment processing solutions on, to ensure you can provide your customers a secure payment processing experience, and you don’t fall victim to digital payment fraud yourself.

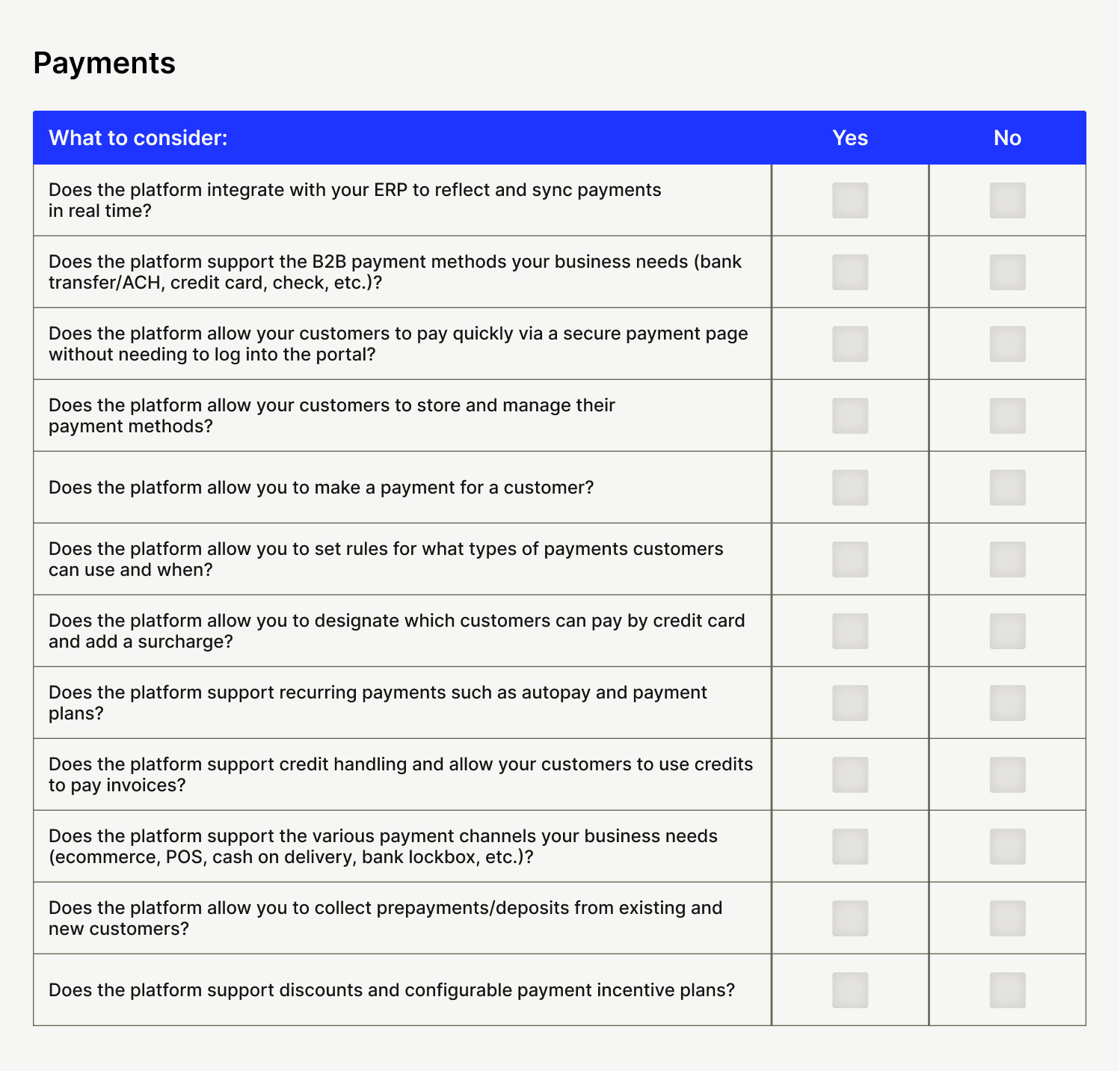

Evaluation criterion 1 — Payments

Easily facilitate business-grade online payments:

Evaluation criterion 2 — Security

Partner with a payment processing vendor who takes security as seriously as it takes payments:

How to Choose Accounts Receivable Automation Software

All payment fraud prevention resources

Staying vigilant against payment fraud is critical. Understand what to look for, and how you can keep your company secure from bad actors looking to cash in:

Payment Fraud Explained: How B2B Merchants Can Fight Fraud and Maximize Customer Experience

Payment fraud is ever evolving. This guide explores the different types of payment fraud, how it can be detected and prevented, how businesses can process payments while maximizing customer experience, and much more.