To add complexity (and confusion) I2C is a subset of the order-to-cash process that encompasses the entire sales cycle, from quote generation to payment receipt and closing of a sale.

Cash Application: The Ultimate Guide

Swift and accurate cash application leads to better straight-through processing rates, lower processing costs, reduced DSO, improved efficiencies, and better customer service.

How Versapay customers achieved 138% ROI

When automating cash application, ROI is critical.

In this TEI™ commissioned study conducted by Forrester Consulting for Versapay (May 2024), you'll learn how a composite organization of customers achieved significant ROI.

That includes:

- 69% improvement in cash posting efficiency

- Net savings present value of $306k over 3 years

- Payback of investment in under 6 months

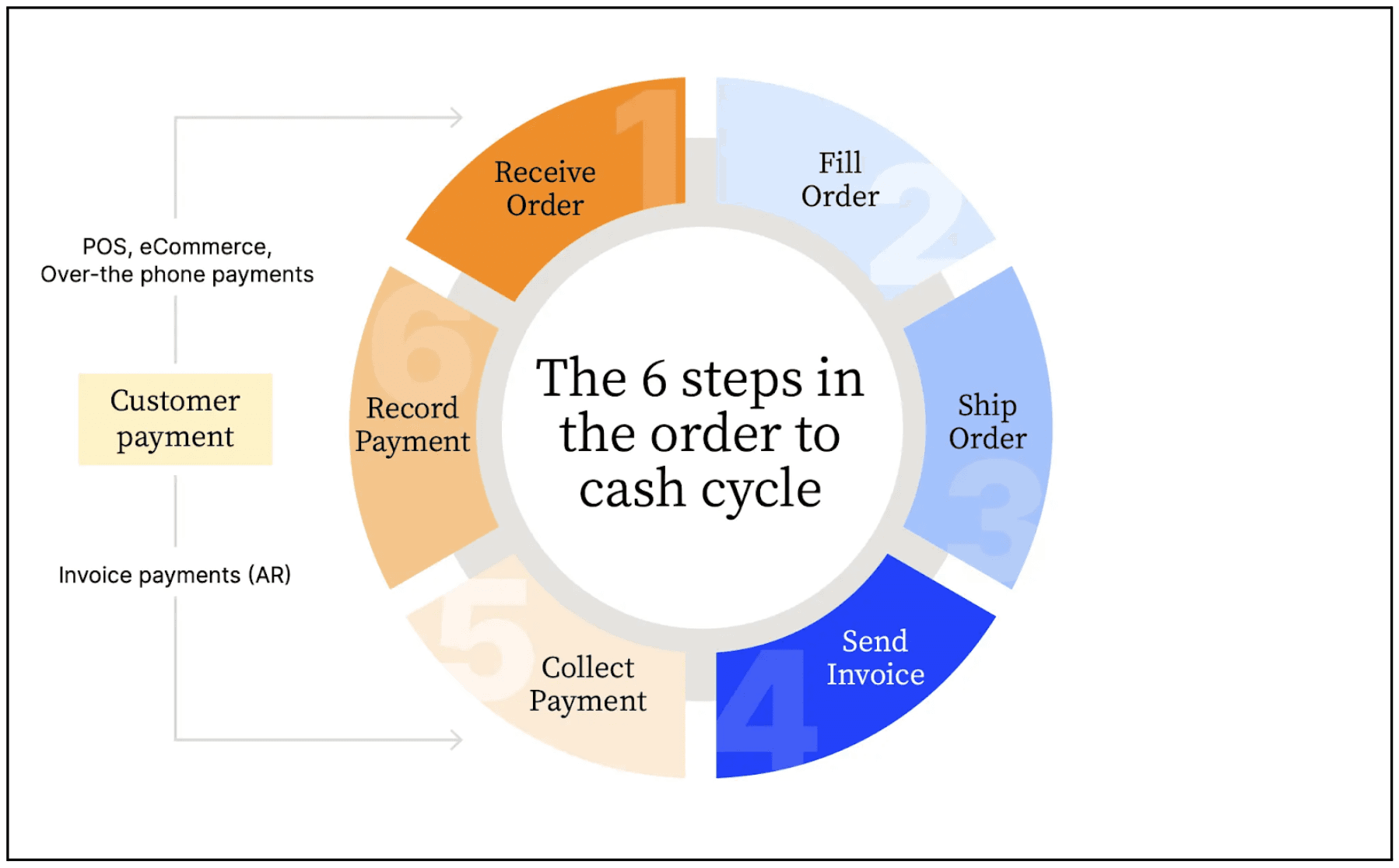

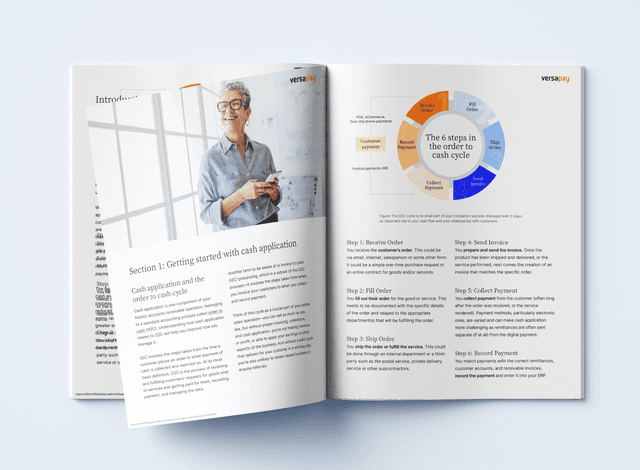

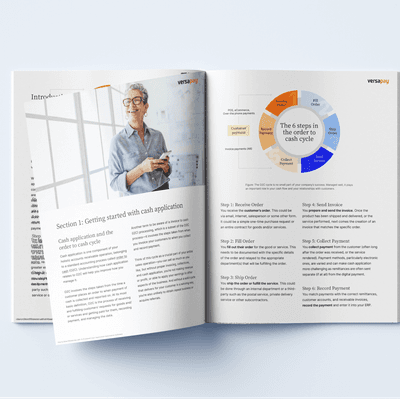

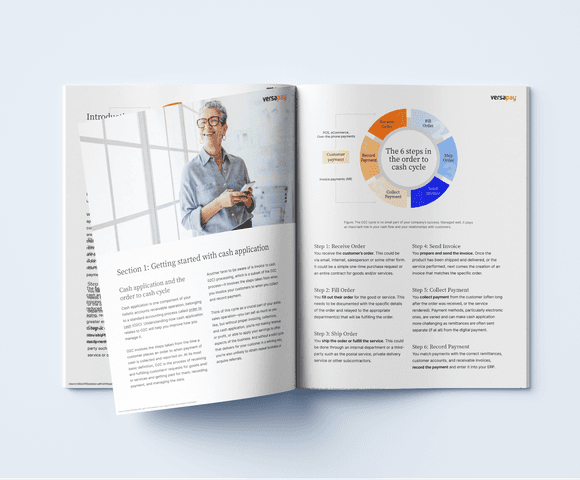

So, where does cash application fit into all this? At the nine o’clock spot in the illustration below — O2C Step 6: Record Payment.

Back to our first question: What is cash application? It’s a critical link in the O2C cycle, along with proper invoicing and collections. Without it, you won't generate or identify revenue or profit, nor will you be able to allocate your earnings towards other aspects of the business. Plus, building a more streamlined O2C cycle provides a winning experience to your customers that’s essential for repeat business or referrals.

The steps in the cash application process

Although companies vary in nature, size, volume of customers, quantity of invoices, and delivery and payment methods, most follow similar general steps in their cash application process:

- Step 1 — Your AR team creates an invoice and sends it to the customer.

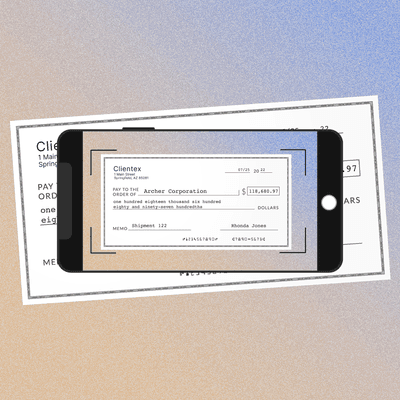

- Step 2 — Payment is received through various methods like check, wire transfer, credit card payment, automated clearing house (ACH), electronic data interchange (EDI), or corporate trade exchange (CTX).

- Step 3 — The customer sends a remittance to explain why the payment was made, either with the payment or separately.

- Step 4 — The data is then reconciled to ensure accuracy, and any discrepancies are investigated and resolved.

- Step 5 — The payment is recorded in your company’s enterprise resource planning (ERP) system.

- Step 6 — Finally, the process is reviewed to look for ways to improve it. A receipt for payment may also be sent to the customer.

A brief glossary of cash application terms

Here are the most common and useful terms to understand when discussing cash application and the various facets of the process.

Cash Application — The last step in the order-to-cash process, as a company applies a payment to a customer’s outstanding balance. It signifies the successful completion of a sale.

Remittance Data (Remittance Advice) — Information accompanying payments to help match them to specific invoices. Often missing in e-payments, requiring manual matching.

Manual Cash Application — Labor-intensive process where AR teams manually reconcile incoming payments from various channels with outstanding invoices.

Automated Cash Application — Leveraging automation to match payments to invoices, reducing errors and enhancing efficiency in the order-to-cash workflow.

General Ledger (GL) — The central repository for a company’s financial transactions, including recording revenue and expenses.

Invoice Matching — The process of associating payments with specific invoices based on relevant details.

Payment Channels — Various methods through which payments are received (e.g., checks, credit cards, ACH transfers).

Unapplied Cash — Payments received without clear assignment to specific invoices.

Overpayment — When a customer pays more than the outstanding balance, requiring proper handling.

Underpayment (Short Payments)— When a payment falls short of the invoice amount, necessitating resolution.

Aging Reports — Reports that summarize outstanding balances by age (e.g., 30 days, 60 days, 90 days).

Cash Flow Management — Ensuring efficient movement of funds within the organization.

Payment Reconciliation — Verifying that payments match expected amounts and identifying discrepancies.

Customer Experience — The experience the buyer/customer receives (or perceives) during the payment process, which can be positive or negative.

What are the risks of the cash application process?

Let’s be clear: There’s always an element of risk in any process. It’s just more aggravating—and damaging—when it involves money. What are the risks of the cash application process? How can they impact the organization?

The most apparent danger is that a poor cash application process can injure the efficiency and profitability of a business. The flip side of that is that a well-run cash application process can boost them.

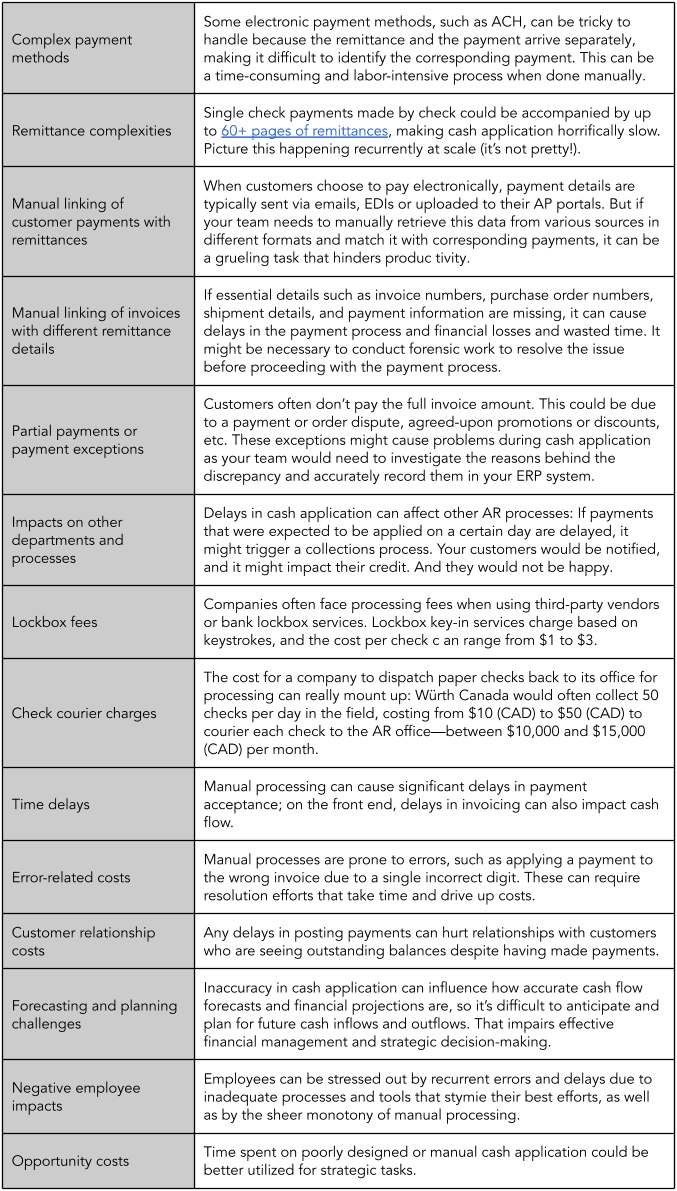

Let’s take a look at the various costs and delays that can drag on a cash application process and make it inefficient—particularly if it’s a manual process:

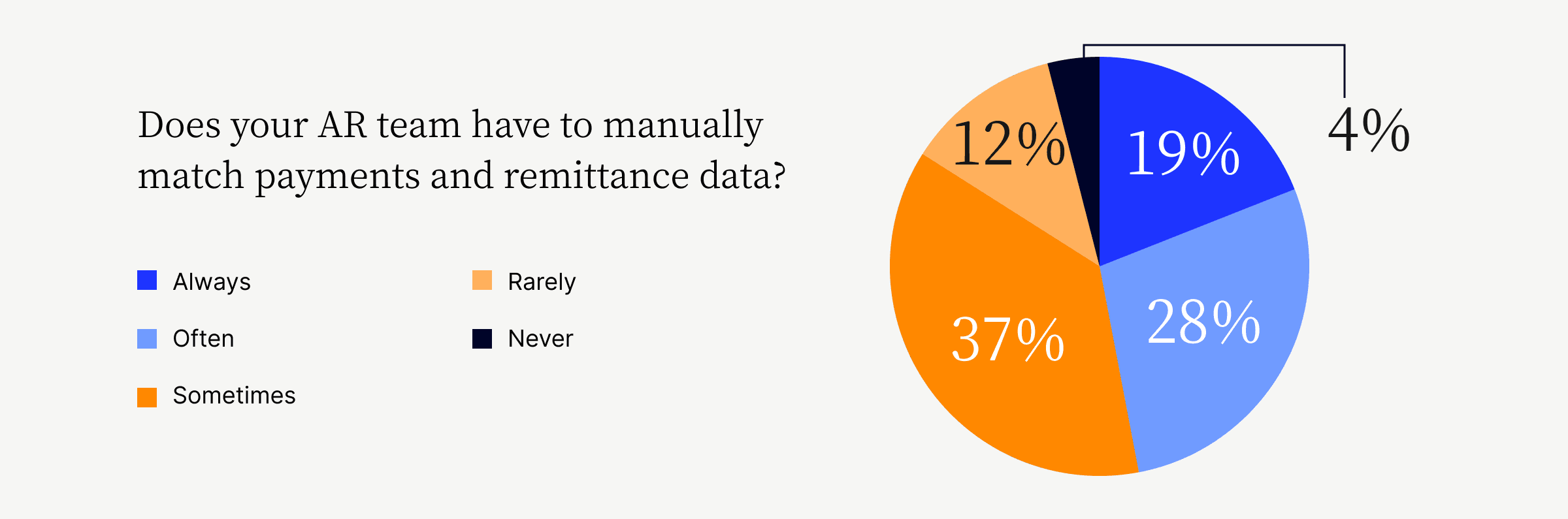

Many companies are still mired in manual cash application

Despite these risks, about 85% of finance leaders in recent Versapay research were still manually matching payments with remittance information, with nearly 20% claiming this as their process for all payments.

This may seem workable if you’re a B2B operation with less than 1,000 invoices processed each month. But what if you scale, or already have thousands of customers in multiple regions using different payment methods, and with remittances arriving separately from different sources?

Then conducting cash application manually is undoubtedly taking a prodigious bite out of your productivity, agility, and profitability.

What should your cash application process provide?

Whether they’re manual or automated, here are the attributes you should want in your cash application processes:

Accuracy — The cash application process shouldn’t cause errors that can lead to delays and poor customer experiences.

Speed — When cash is applied more rapidly, you’re able to reduce DSO, lower AR processing costs, and give your enterprise quicker access to its cash.

Standardization — By having standardized, consistent cash application processes, you eliminate inefficiencies and remove compliance issues.

How to know if your cash application system needs help?

These seven key indicators can help you determine if your current cash application tools or processes are falling short:

1. The speed of payment application

Once you’ve got remittance data in hand, how fast are payments being applied? The same day? The day after? The week after? Cash should be applied ASAP, because the longer it goes unapplied, the less readily available cash the company has on hand.

2. If cash application errors are happening

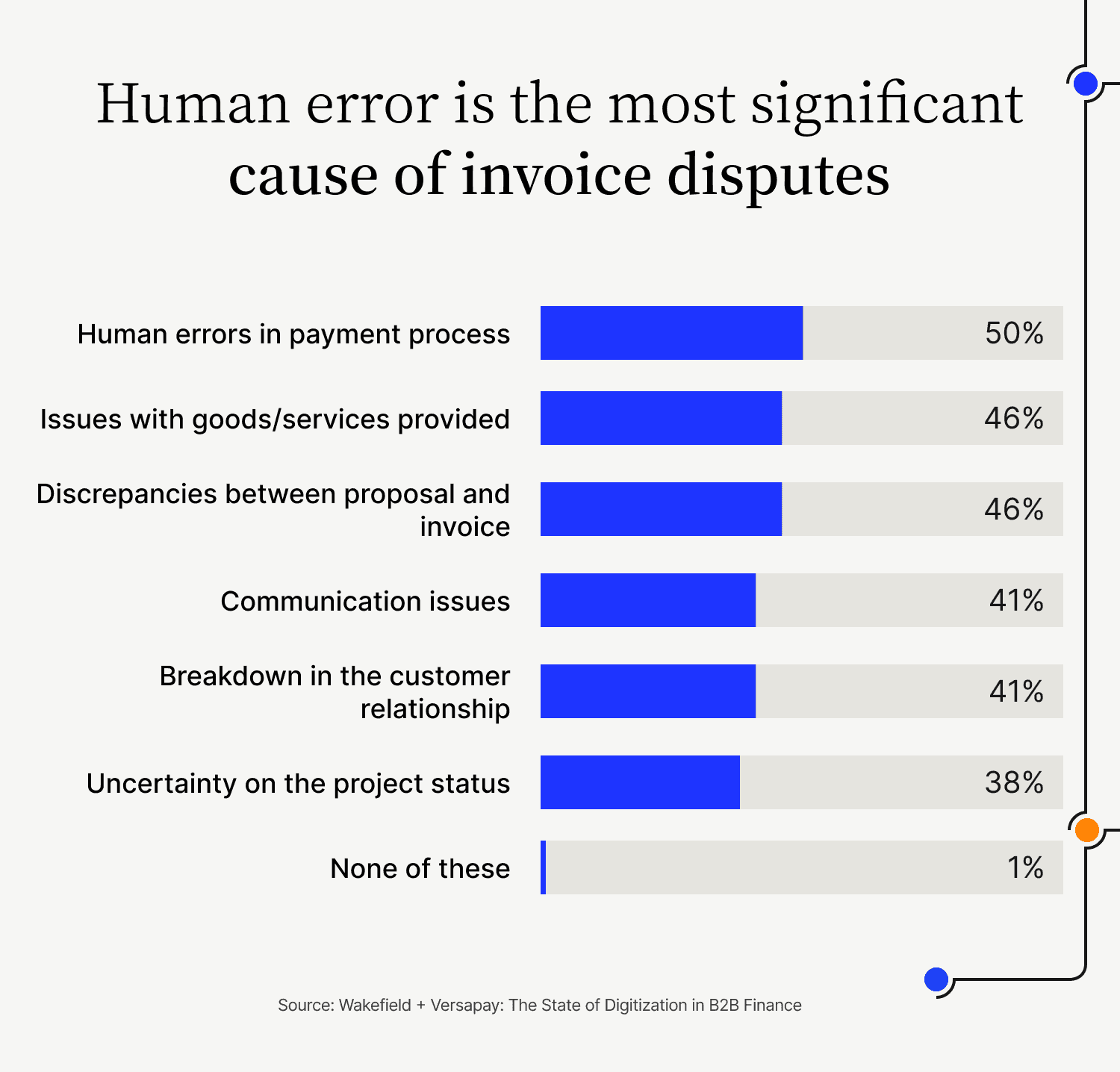

The more payments you take in, the more likely you’ll encounter cash application errors. While cash application specialists are diligent, meticulous and painstakingly thorough, any matching work that’s done manually will see errors. Zero errors is always the grail but getting even close to it is far from feasible with manual processes. Human error, by the way, is the most significant cause of invoice disputes; so even the smallest amount is detrimental to your cash flow.

3. The volume of remittances received

A lack of remittance data means more clarification is needed before the AR team can match payments with the right customer account and open receivable. To avoid slowdowns in the cash application process, monitor what percentage of payments are received without remittance data and work toward reducing that number.

4. The amount of team time spent on cash application

Here are useful benchmarks to apply in assessing this:

You’re in good shape — Cash application takes up less than 10% of your AR team’s time.

You’re working on it — It eats up about 15% of the team’s time.

You’ve got a problem — When over 25% of their time goes toward cash application.

If your AR specialists are manually downloading remittance information and matching it to payments, cross-checking invoices with remittance details, and searching for discrepancies caused by partial payments or payment exceptions, then you’re underutilizing skills that could go toward strategic projects.

5. Reporting is difficult because your data is unmanaged

If you don't have a tool to organize and analyze your cash application data, it can be difficult to identify which payments are still pending. This also means you can’t use data to evaluate the efficiency of your process or find ways to enhance it.

6. Customers are encountering payment issues

Are you getting customer feedback that finds fault with your cash application tools or processes? Have any of them contacted you to report a missed discount? Or asked about an outstanding invoice notice they received even though they’d already paid it?

7. Accepting paper checks is easier than managing digital payments

If this is the case, it may mean your AR team needs help managing digital payments. Moving from accepting only paper checks to also receiving digital payments involves adopting new cash application tools and revamping the workflows involved. This way, your team has everything it needs to reconcile remittances from a more complex range of payment methods.

Guide to AI-Powered Cash Application Automation Software

How To Solve Common Cash Application Challenges With Automation

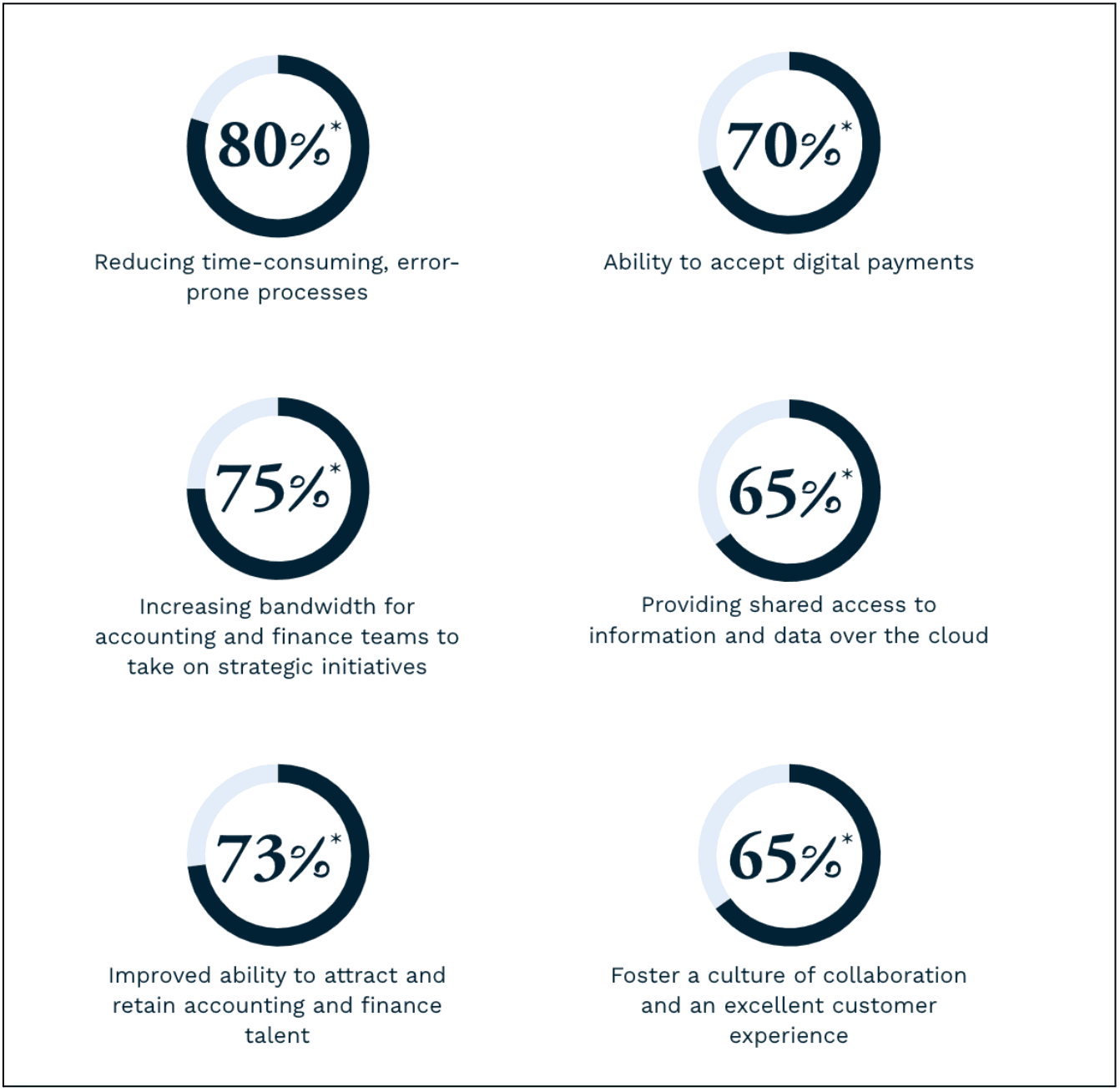

Inadequate AR processes, including cash application, can hamstring cash flow, drag down profitability, drive up costs and make it hard to do financial analysis and planning. A growing number of finance leaders are recognizing the need to automate AR processes in order to improve cash flow, as well as capture a whole spectrum of other benefits:

Research by PYMNTS and American Express found that 44.2% of executives at midsize firms had automated at least two AR processes, and 15.3% had automated 3-4 processes, while 26% of firms not currently innovating accounts receivable were planning to start doing so in the next six months, 27% in six to 12 months and 10% in one to three years.

The movement toward automation, including cash application automation, is no longer confined to early adopters: It’s a groundswell across almost every industry.

The 6 B2B payment trends impacting cash application

There are six notable trends impacting the traditional cash application process:

Digital transformation

Multiple payment channels

Real-time payments

Emergence of AI and machine learning

Demand for better customer experiences

Cash application automation as a key next step

1. Digital transformation

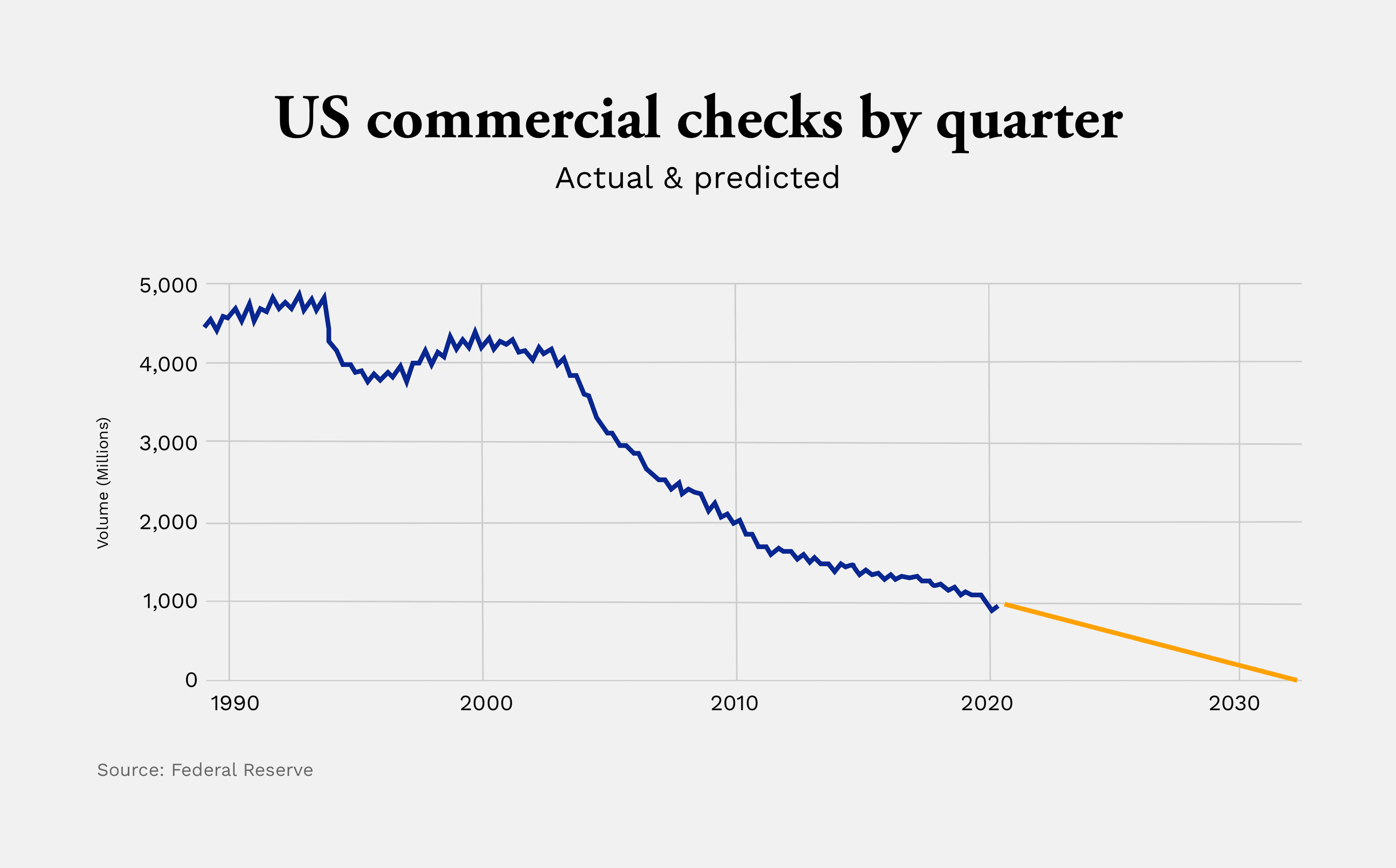

Businesses are flocking to digital payment solutions to streamline processes, improve efficiency, and cut costs. This includes employing electronic funds transfers (EFTs), virtual cards, and mobile payment apps.

Just 33% of B2B payments in the U.S. and Canada were made by check in 2022, a nine-point decline since 2019. Cash application processes need to adapt to this new landscape, where payment may arrive in different ways, yet the customer will expect to see that payment applied without any hiccups along the way—regardless of how they paid you.

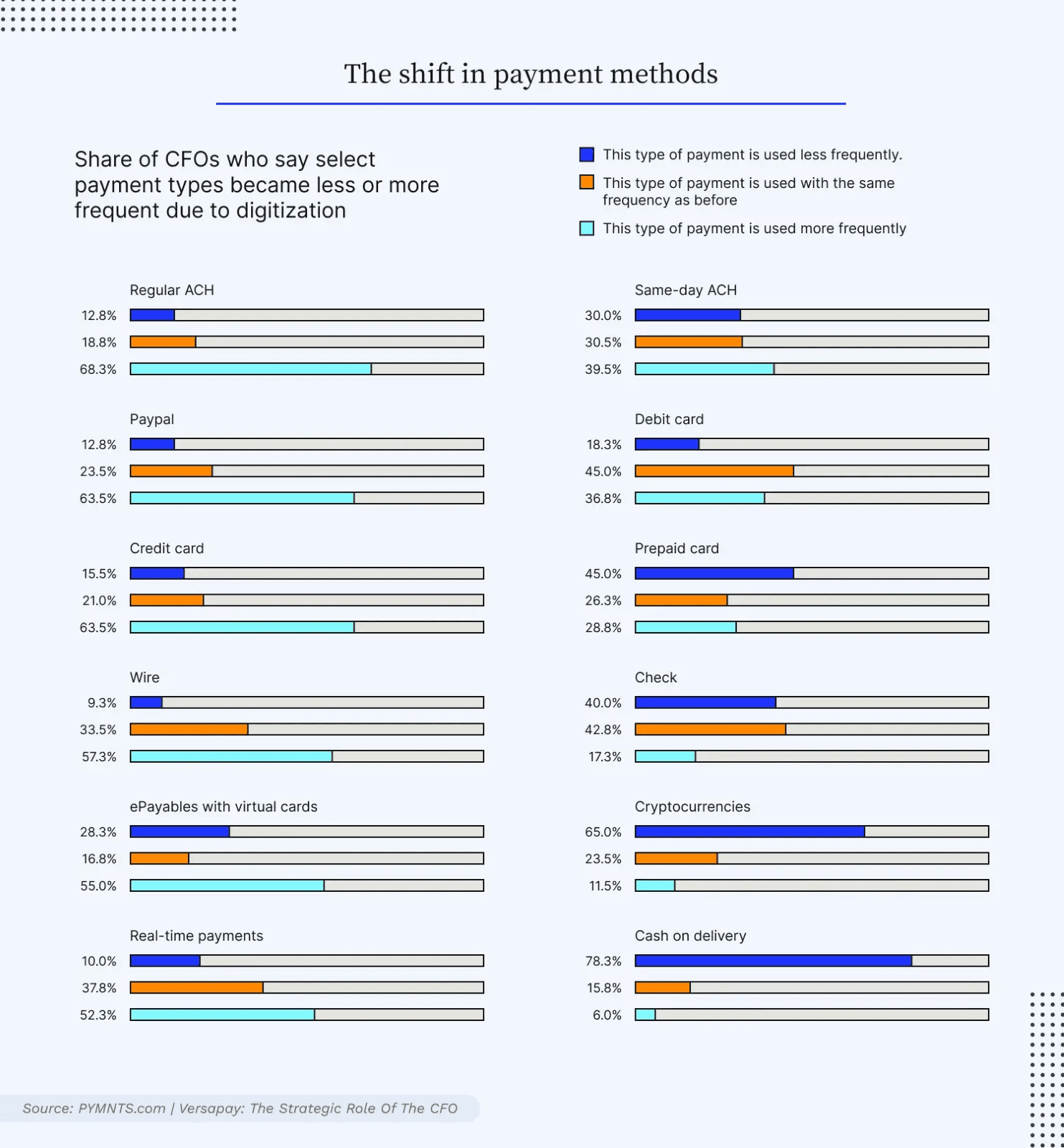

2. Multiple payment channels

Your customers may already be expecting to be able to make B2B payments the way they prefer, by using any of the multiple methods just described. They’re pursuing cost savings and efficiency, better cash management, convenience, and in some cases are being pressed to “go digital” by their own customers and key vendors.

It's vital that AR teams are able to intake a variety of payment options to sweeten customer satisfaction and expedite revenue collection, and cash application processes need to keep pace.

3. Real-time payments

Real-time payment systems are gaining traction. These systems allow for instant fund transfers between businesses, improving cash flow management and reducing reliance on traditional payment methods. As with the other trends, cash application tools have to be as integrated and automated as the other functions within AR in order to not be a bottleneck or process pain point.

4. Emergence of AI and machine learning

Solutions using AI and machine learning have revolutionized accounts receivable and cash application by analyzing large amounts of data and identifying patterns that humans may miss or take time detecting. AI can spot payment patterns and predict when customers are liable to pay, helping businesses manage cash flow and cutting the risk of late payments. They can also help identify potential fraud or suspicious activity.

By adopting AI-powered automation for AR and cash application, businesses can reduce costs, errors and risk, while optimizing cash management and their ability to make more concrete future financial projections.

5. Demand for better customer experiences

Improving customer experiences is imperative for the AP/AR ecosystem. A traditional B2B I2C process gives customers scant visibility into the status of outstanding payments or what they owe, while your AR team struggles to know if customers are going to send payments.

With few communication options except emails and phone calls, it’s hard (and slow!) to resolve disputes, address errors or run down remittance data, resulting in a “sub-optimal” customer experience.

B2B buyers now demand greater visibility and seamlessness from AR. This means cash application has to be accurate and timely, and integrated with collaborative systems that keep customers updated on payment status while providing two-way communication to speed up the resolution of cash application issues.

6. Cash application automation as a key next step

Cash application is a key AR process, as we’ve seen. So more of these leaders are waking up to just how pivotal a role the cash application process plays in AR success—and why cash application automation should be an urgent improvement.

In one finding, 37% of CFOs said slow processes are a big problem for AR teams and that cash management, specifically, is the most challenging part of AR.

What is cash application automation?

It’s a straightforward definition: Cash application automation is a digital solution that permits cash application tasks to be completed without any need for direct human involvement.

In advanced cash application software solutions, technologies like artificial intelligence and machine learning work jointly to match payment data to open receivables. Cash application automation is often included alongside other AR automation solutions for invoicing, collections, and payment processing.

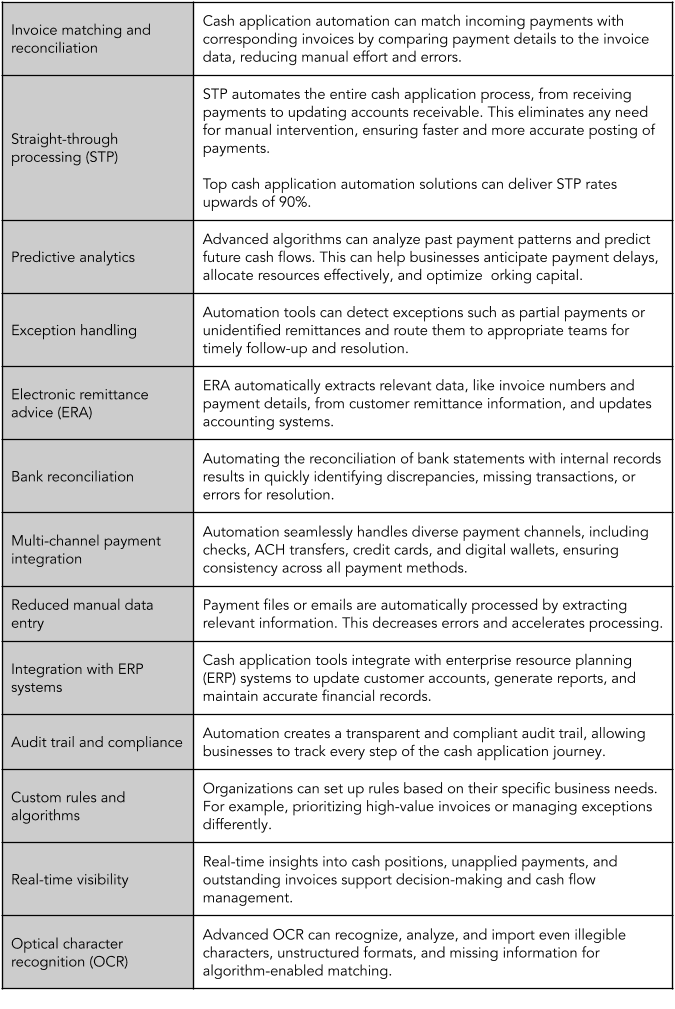

What capabilities does cash application automation deliver right now?

Some of these capabilities would have been undreamt-of not so long ago, but nowadays they’re commonplace cash application automation software functions:

Why do companies need to automate their cash application processes now?

The advent of digital payments has made the cash application process even more complex; we’ve touched on how electronic payments may have remittance data sent separately, forcing even more manual matching onto AR teams.

By automating the cash application process, organizations can streamline operations, reduce errors, save costs, and improve cash flow. For most, those benefits are enough to make it worthwhile. But improving the payment experience is another key reason to automate since your customers are used to fast and precise consumer payment processes—and may already be getting better experiences from your competitors that have automated.

Let’s examine how automating the cash application process works, and the benefits you can reap from the best cash application automation software solutions.

How Cole, Scott & Kissane Streamlined Cash Application Amid Growing Payment Complexity

7 Tips for Better Automated Cash Application

How does cash application automation work?

How does a truly advanced cash application automation solution work? Here’s a quick overview. If it wants to justify those all-to-common buzzwords “advanced” or “sophisticated,” it does so by incorporating the latest technologies.

It has advanced automation technologies

It will leverage advancements like robotic process automation (RPA), AI and machine learning in order to:

Retrieve and aggregate remittances from multiple and diverse sources like emails and web portals, collating them in a centralized archive and freeing AR teams from manually searching for remittance information.

Match invoices, automatically identify and validate deductions and discounts, and map customer reason codes back to ERPs.

It includes optical character recognition

OCR helps auto-extract check stub information with ease and accuracy by using templates to map out which regions of an image contain needed data or by using AI to search for specific items that indicate areas of interest.

There are two primary techniques used in OCR-equipped cash application software:

OCR Template technique

Ingests data from lockbox files.

Mines AP portals and emails for remittance data.

Configures payment application rules.

Matches buyer codes with supplier codes.

AI-Based OCR technique

Uses intelligent OCR and machine learning to quickly match payments to invoices without manual intervention.

Works with traditional checks, image scans, lockbox files, wire transfers, emails, ACH, ETF, and AP web portals.

Streamlines exception handling by identifying payments that need human intervention and offering collaboration tools.

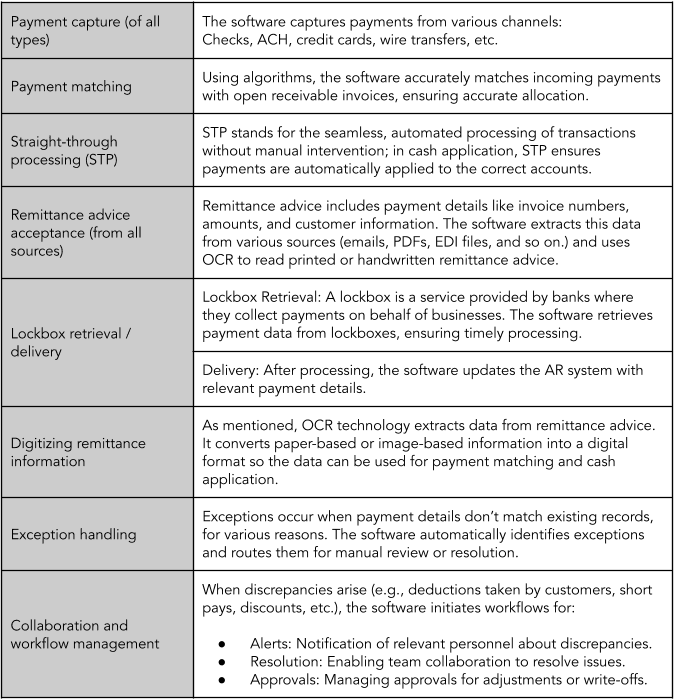

So, how does cash application automation actually do its job?

Here’s how artificial intelligence-powered automation comes into play in the cash application process:

How Versapay customers achieved 138% ROI

How This Healthcare Service Provider Gives 4.5 Hours Back to Cash Application Specialists Every Day with Automation

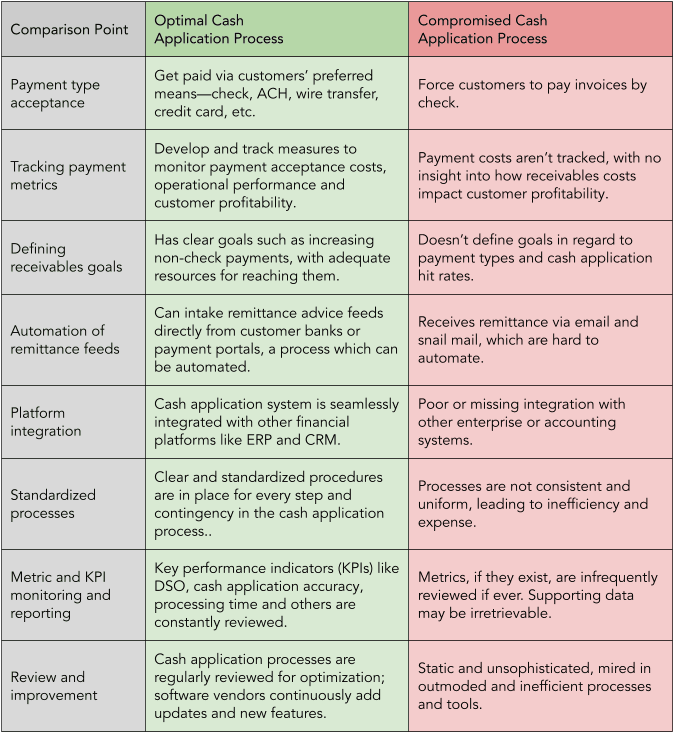

How can you improve the cash application process?

What does an optimal, top-performing cash application process look like versus an inadequate, poorly-performing one? Here’s a side-by-side comparison of how the two stack up:

Tips for improving your cash application process

If you’re looking to begin automating cash application, or even if you’ve already started down that path at some level, here are proven best practices for using automation to maximize process performance:

Accept digital payments — Digital payments, especially made via a payment portal with an electronically-issued invoice, are easier to match than paper checks. Cash application automation speeds up the process and eliminates errors common to manual reconciliation.

Digitize remittance advice data — With OCR and automation, you’ll capture remittance data in real-time and match it to invoices, saving countless human hours while reducing lockbox key-in fees and the sheer tedium of manual reconciliation.

Employ mobile check deposit — Productivity gains from mobile check deposits can be considerable, as businesses still collect 25% to 75% of payments by check payments that are manually matched with remittance advice.

Ensure straight-through processing on e-payments — For electronic payments against electronic invoices, automated cash application can automatically link remittance with payment and help you see straight-through processing rates of over 90%, and a solution that uses AI and machine learning can lift efficiency by up to 75%.

Automate team workflows around short pays, deductions, and discounts — A customer may have a good reason for short payment but it means headaches and back-and-forth emails and phone calls if you manually reconcile payments. Cash application automation platforms with AI can alleviate them: For instance, AI might automatically recognize how a lump sum payment actually covers multiple outstanding invoices and apply the payment accordingly.

What Used to Take Haas Door All Day, Now Takes Minutes with Advanced Cash Application

How to Improve the Cash Application Process

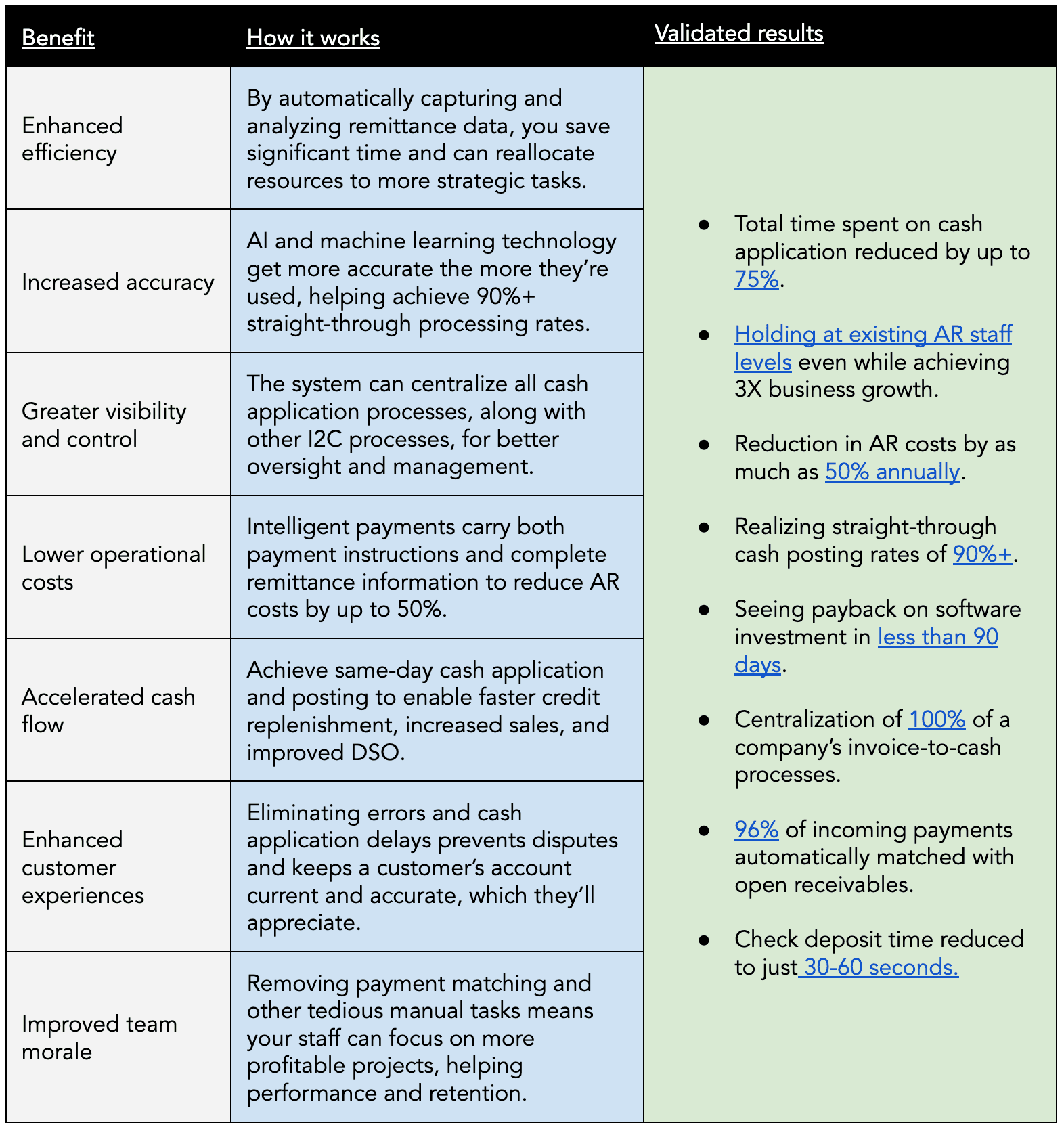

The benefits of cash application automation

Cash application automation using a full-featured solution that leverages AI can deliver a long list of improvements and tangible returns. And it bears repeating: The longer an AI is in use, the smarter it becomes, with corresponding effects on the benefits it brings.

6 Signs Your Cash Application Process Could Be Better—And How To Improve It

Choosing the best cash application automation tool

There’s a growing number of automated cash application tools out there, so choosing the best system for automatic cash application—the one that fits your needs today and that can scale with you tomorrow—will take a little homework.

Two suggestions?

Focus on solutions that integrate AI and machine learning, as this will contribute to both product performance and its longevity as non-AI solutions become outmoded.

Evaluate both the platform and the provider; a software solution is only as reliable as the organization that supports it.

That’s why we’ve provided this evaluation criteria checklist you can use in assessing competing software solutions. Take a free, interactive copy with you for the road:

Cash application automation is critical to helping accounts receivable teams keep up with the speed of the modern business world. It can easily be the difference between slow cash flow and a healthy stream of income.

It’s also important to remember that automated cash application software doesn’t just affect your day-to-day life—it has a major impact on customer experience. And in times like these, holding on to every customer you can is critical. Plus, who doesn’t want their customers to have great payment experiences?

As for parting words, how about a free demonstration of Versapay's cash application automation software?

All cash application resources

Keep your books in top shape. Learn about the practices and technologies that help you ensure every payment matches an open receivable.

A Finance Leader's Guide to AI-Powered Cash Application

With advanced cash application automation technology, you can harness powerful, high-tech tools to make your cash application process smarter, faster, and stronger.

Determine the potential financial impact of Versapay Cash Application on your organization.